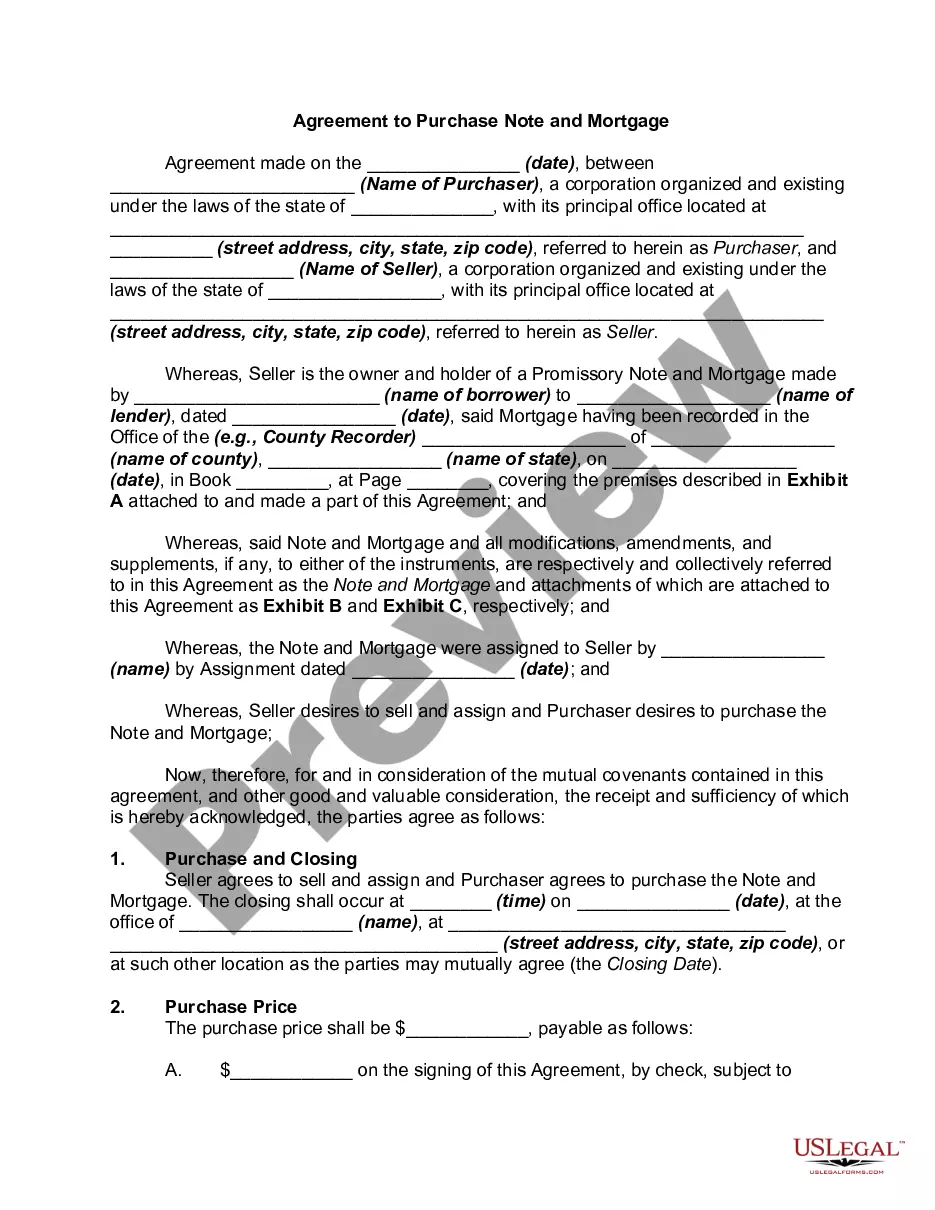

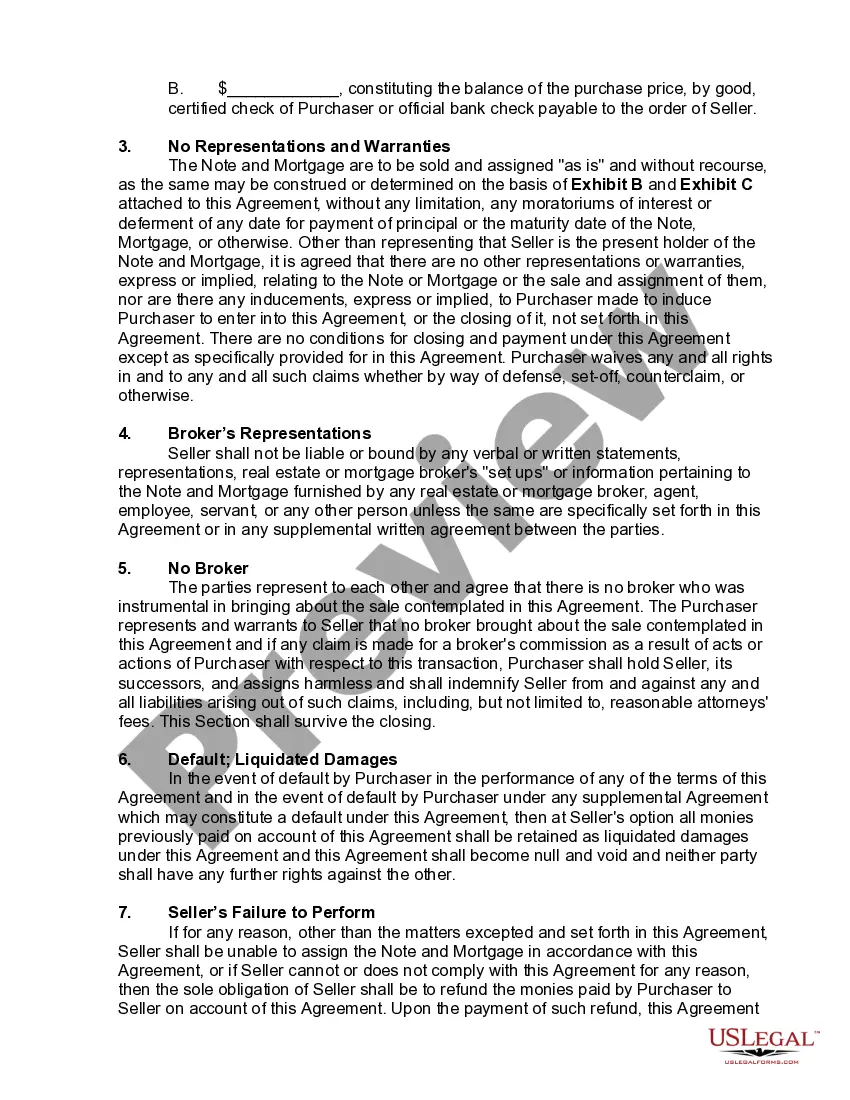

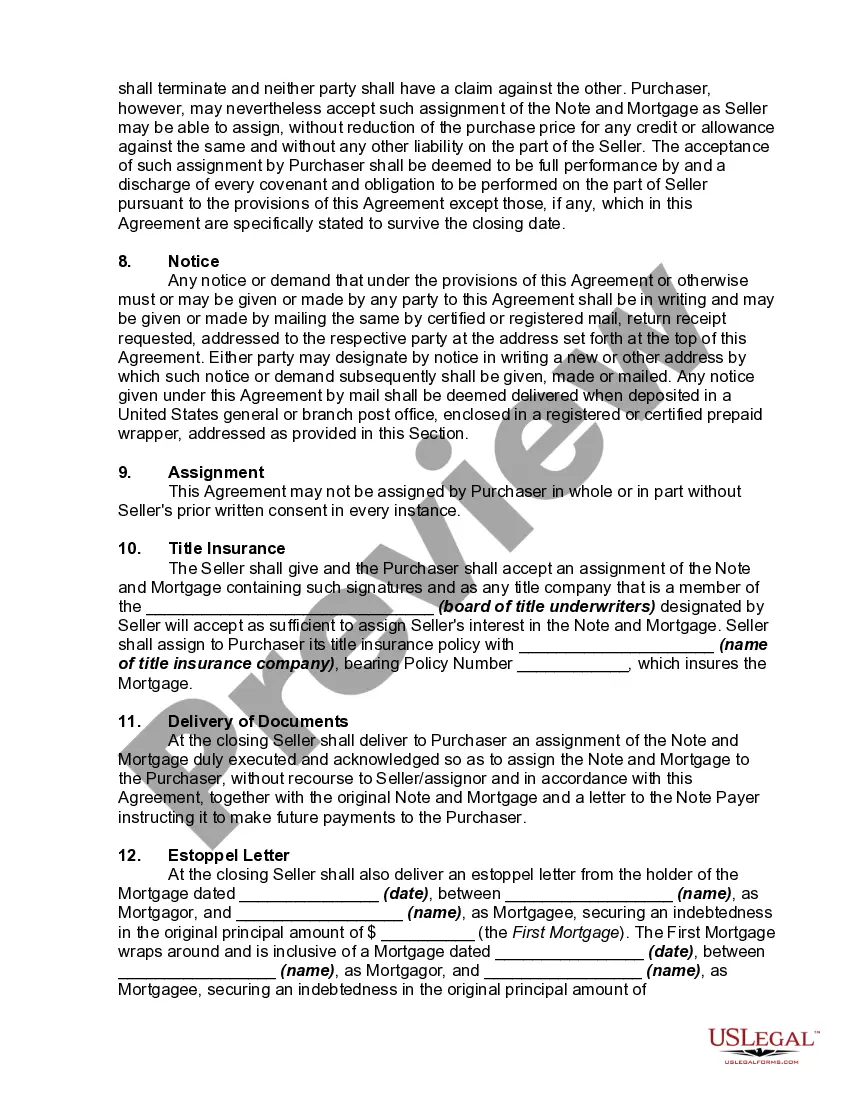

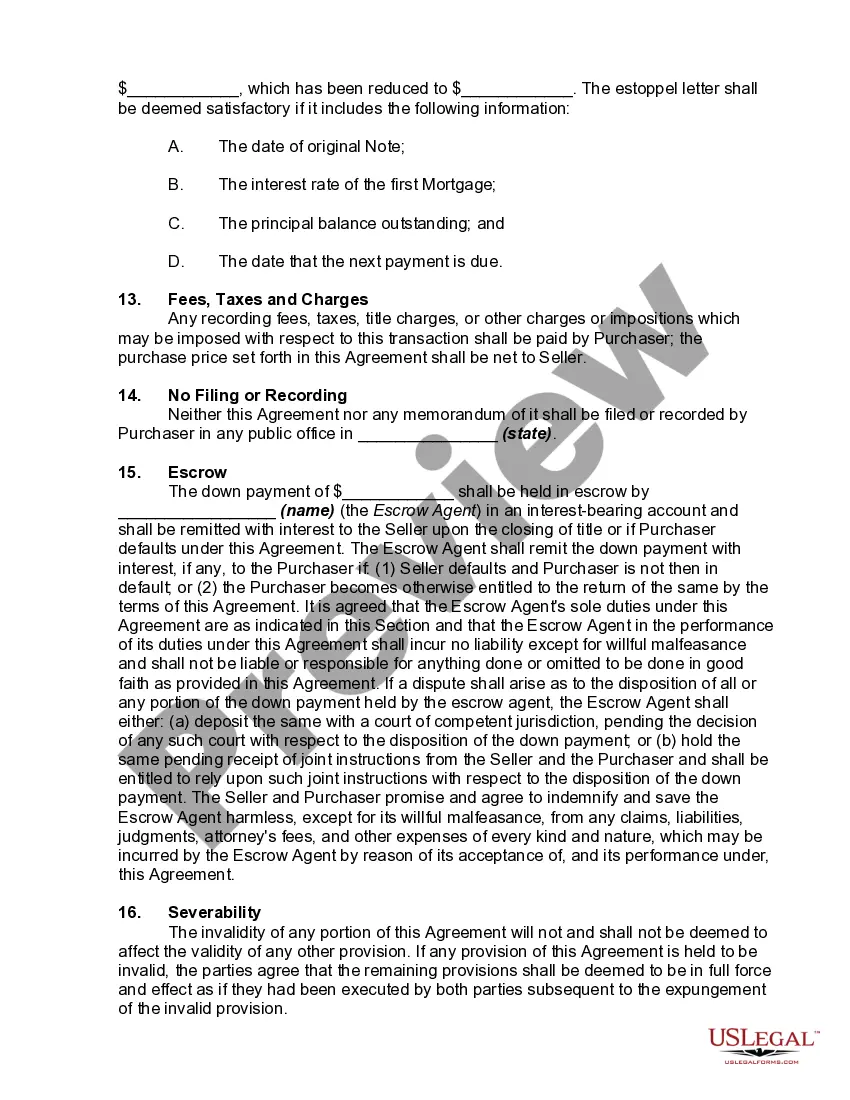

The Virgin Islands Agreement to Purchase Note and Mortgage is a legal document that outlines the terms and conditions of a real estate transaction in the Virgin Islands. It is used when a buyer agrees to purchase a property and enters into a financing arrangement with the seller. This agreement ensures that both parties are protected and have a clear understanding of their rights and obligations. The Agreement to Purchase Note and Mortgage typically consists of several key components. First, it includes details about the buyer and seller, such as their names, addresses, and contact information. It also specifies the property being sold, including its address, legal description, and any applicable zoning restrictions or covenants. The agreement outlines the purchase price of the property, including the payment terms and any applicable interest rates. It also states the amount of the down payment and whether the buyer will assume an existing mortgage or obtain financing from a third party. Furthermore, the document includes clauses regarding the closing procedure, such as the date when the transaction will be completed, the location of the closing, and the allocation of closing costs between the buyer and seller. It is important to note that there may be different types of Virgin Islands Agreement to Purchase Note and Mortgage depending on the specific circumstances of the transaction. Some common variations include: 1. Traditional Agreement to Purchase Note and Mortgage: This is the most basic and commonly used form, in which the buyer agrees to purchase the property and finances the purchase through a mortgage. 2. Seller Financing Agreement to Purchase Note and Mortgage: In some cases, the seller may agree to act as the lender and finance the purchase directly. This type of agreement may include specific terms related to interest rates, repayment schedules, and default procedures. 3. Assumption Agreement to Purchase Note and Mortgage: If the property being sold has an existing mortgage, the buyer may choose to assume the mortgage rather than obtaining financing from a different lender. This agreement outlines the terms of the assumption, including any additional payments or conditions. Regardless of the specific type, the Virgin Islands Agreement to Purchase Note and Mortgage is a crucial legal document that safeguards the interests of both the buyer and seller in a real estate transaction. It provides a clear framework for the purchase and financing of the property, ensuring a smooth and legally binding transaction.

Virgin Islands Agreement to Purchase Note and Mortgage

Description

How to fill out Virgin Islands Agreement To Purchase Note And Mortgage?

Finding the right legal document design can be a have a problem. Of course, there are plenty of web templates available on the net, but how do you discover the legal form you will need? Utilize the US Legal Forms web site. The service offers a huge number of web templates, like the Virgin Islands Agreement to Purchase Note and Mortgage, which you can use for organization and personal requirements. All the varieties are checked by pros and fulfill federal and state demands.

If you are presently authorized, log in to the account and click on the Down load option to obtain the Virgin Islands Agreement to Purchase Note and Mortgage. Make use of your account to appear through the legal varieties you might have bought formerly. Go to the My Forms tab of your own account and obtain an additional copy in the document you will need.

If you are a whole new customer of US Legal Forms, allow me to share basic recommendations so that you can adhere to:

- Very first, make sure you have selected the correct form to your area/state. You can examine the shape while using Preview option and look at the shape description to make sure this is basically the best for you.

- In case the form fails to fulfill your expectations, make use of the Seach field to find the proper form.

- When you are sure that the shape would work, go through the Acquire now option to obtain the form.

- Opt for the costs strategy you want and enter in the essential information. Create your account and buy your order using your PayPal account or credit card.

- Pick the submit format and acquire the legal document design to the product.

- Total, change and print and indication the acquired Virgin Islands Agreement to Purchase Note and Mortgage.

US Legal Forms may be the biggest collection of legal varieties in which you can discover different document web templates. Utilize the company to acquire professionally-produced paperwork that adhere to condition demands.

Form popularity

FAQ

Qualifying for a Mortgage in the BVI There are some common factors regardless of the lender we use in the BVI; you will be required to have 50% equity in the home and they must be in the tourist or expat areas of the island. For our private loan, the minimum property value is $1,500,000.

Buying Process, Fees & Taxes Can foreigners buy property in the BVI? Yes, foreigners can buy property in the BVI and the Government of the BVI welcomes investment from overseas buyers. However, foreign nationals are required to apply for a Non-Belonger Land Holding Licence (NBLHL) for which there is a small fee.

What Is A Purchase Agreement? A real estate purchase agreement spells out the terms under which a buyer and seller agree to engage in a real estate transaction. Signing a purchase agreement effectively places both the buyer and seller (as well as the property in question) ?under contract.?

The BVI Financial Services Commission is an autonomous regulatory authority responsible for the regulation, supervision and inspection of all the British Virgin Islands financial services including insurance, banking, trustee business, company management, mutual funds business, the registration of companies, limited ...

Although there are higher rates and fees for our private mortgages in the USVI, they can be a much quicker and easier process than trying to finance through the local banks. The banks in the USVI can be a little slower and the qualification is a bit more difficult than you would see on the mainland.

Caribbean mortgages will require full disclosure of income, outgoings and savings. The maximum loan to value available is 70% to 75% of the purchase price, or valuation, whichever is the lower.