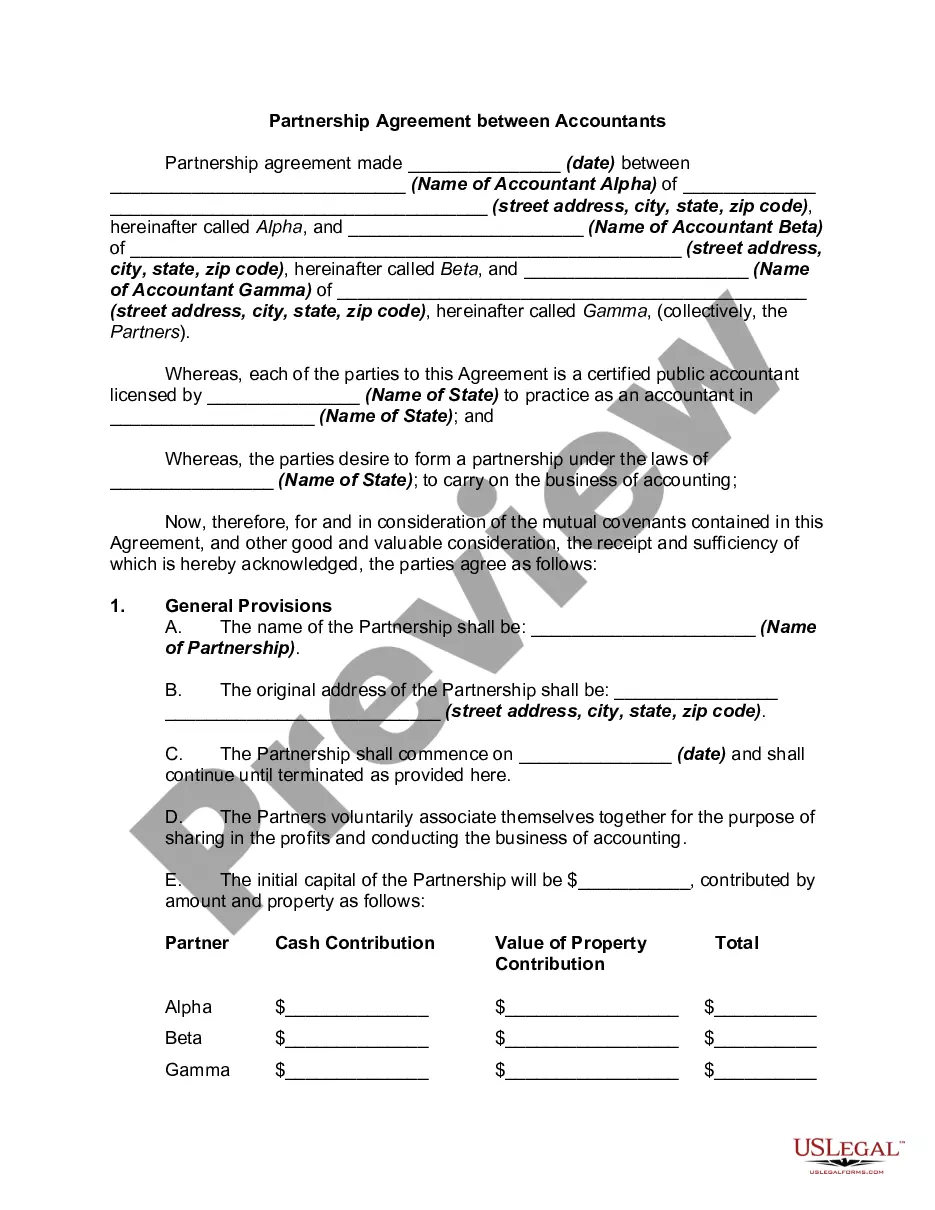

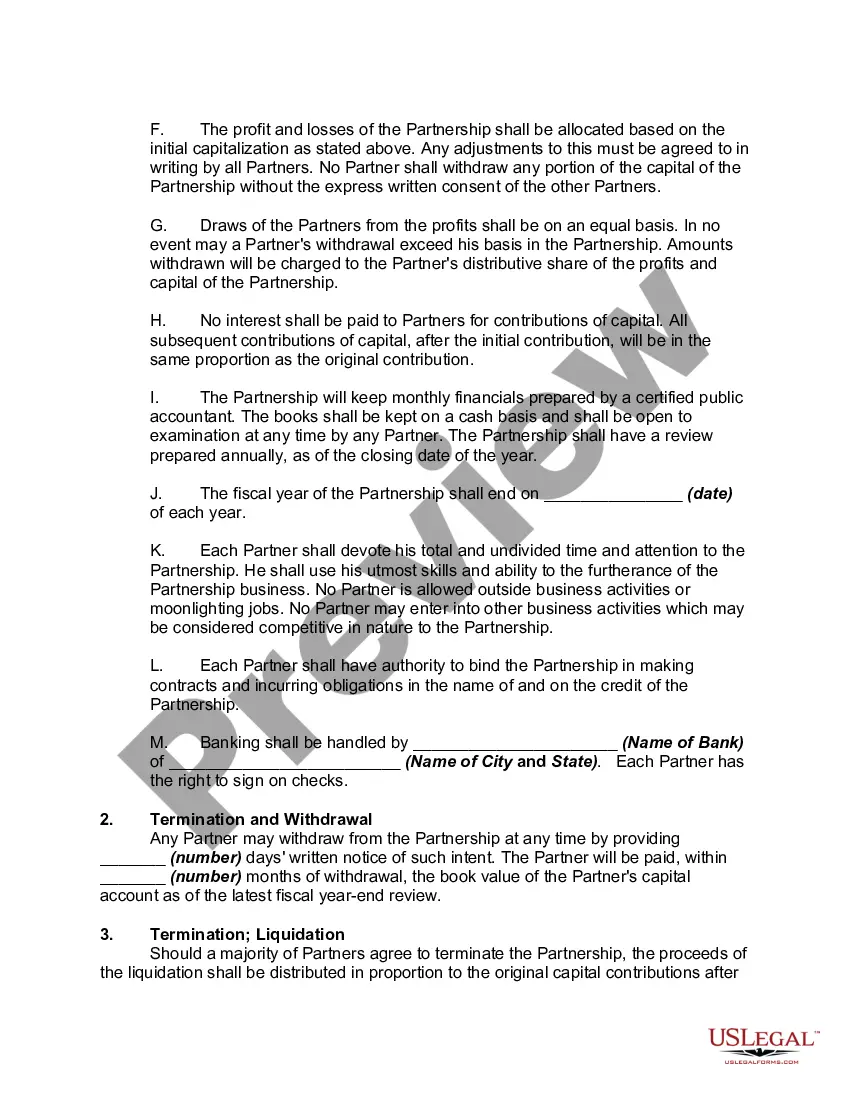

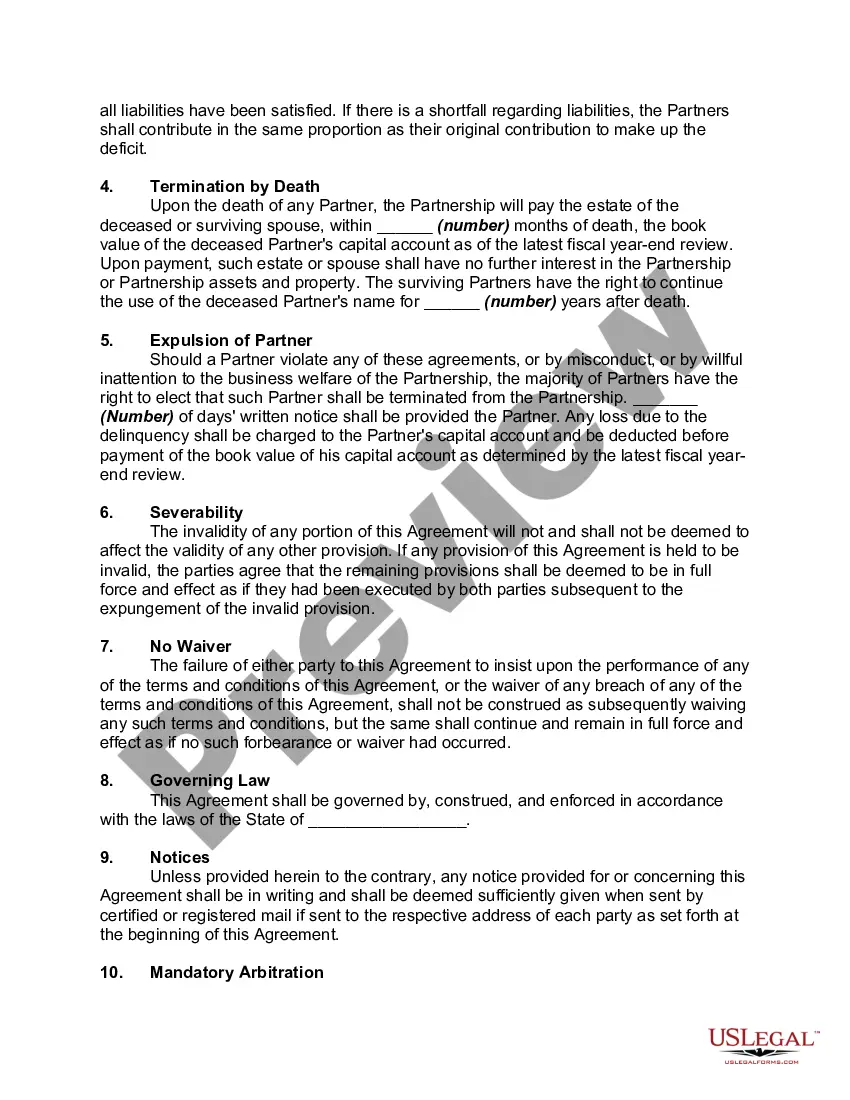

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

A Virgin Islands Partnership Agreement Between Accountants is a legal document that outlines the terms and conditions governing a professional partnership between accountants in the Virgin Islands. This agreement serves as a crucial framework for establishing a formal business relationship between two or more accounting professionals, ensuring clarity, transparency, and legal protection for all parties involved. Here are some relevant keywords related to this topic: 1. Virgin Islands: This refers to the group of islands located in the Caribbean, constituting the United States Virgin Islands (SVI) and the British Virgin Islands (BVI). The partnership agreement is specific to the Virgin Islands jurisdiction. 2. Partnership Agreement: This legal contract defines the rights, obligations, and responsibilities of partners within a business arrangement. In the case of accountants, it outlines the terms related to sharing profits, decision-making, and management of the partnership. 3. Accountants: These are professionals who specialize in financial record-keeping, tax preparation, auditing, and related services. In the context of the partnership agreement, it refers to individuals or firms practicing accounting in the Virgin Islands. 4. Business Structure: The partnership agreement may specify the type of partnership. For example, it could be a general partnership where all partners share equal authority and liability, or a limited partnership where some partners have limited liability. 5. Purpose and Scope: The agreement must define the purpose and scope of the partnership, such as providing accounting services to clients in the Virgin Islands. It may outline the specific industries or sectors the partnership will serve. 6. Capital Contributions: Partnerships typically require partners to contribute capital to fund the business. The agreement will detail the initial and ongoing capital contributions required from each partner. 7. Profit Sharing: The agreement will establish how profits and losses will be allocated among partners. This may be based on the partners' capital contributions or other agreed-upon terms. 8. Decision-making: The agreement outlines how decisions will be made within the partnership, whether through unanimous consent or with a designated managing partner. It may also address methods for resolving disputes. 9. Dissolution and Exit Strategy: In the event that a partner wishes to withdraw from the partnership or if the partnership needs to be dissolved, the agreement will specify the process and any associated terms, such as the division of assets or clients. Different types of Virgin Islands Partnership Agreements Between Accountants may include variations based on the specific needs and goals of the partners involved. For instance, there could be agreements between accounting firms or agreements between individual accountants forming a partnership. Each agreement will be tailored to the circumstances and requirements of the partnering parties involved. In conclusion, a Virgin Islands Partnership Agreement Between Accountants is a vital legal document that establishes the foundation for a professional partnership in accounting services. It addresses various aspects such as business structure, capital contributions, profit-sharing, decision-making, and dissolution. The agreements can be structured based on the unique preferences and circumstances of the partners involved, contributing to a successful and harmonious partnership.A Virgin Islands Partnership Agreement Between Accountants is a legal document that outlines the terms and conditions governing a professional partnership between accountants in the Virgin Islands. This agreement serves as a crucial framework for establishing a formal business relationship between two or more accounting professionals, ensuring clarity, transparency, and legal protection for all parties involved. Here are some relevant keywords related to this topic: 1. Virgin Islands: This refers to the group of islands located in the Caribbean, constituting the United States Virgin Islands (SVI) and the British Virgin Islands (BVI). The partnership agreement is specific to the Virgin Islands jurisdiction. 2. Partnership Agreement: This legal contract defines the rights, obligations, and responsibilities of partners within a business arrangement. In the case of accountants, it outlines the terms related to sharing profits, decision-making, and management of the partnership. 3. Accountants: These are professionals who specialize in financial record-keeping, tax preparation, auditing, and related services. In the context of the partnership agreement, it refers to individuals or firms practicing accounting in the Virgin Islands. 4. Business Structure: The partnership agreement may specify the type of partnership. For example, it could be a general partnership where all partners share equal authority and liability, or a limited partnership where some partners have limited liability. 5. Purpose and Scope: The agreement must define the purpose and scope of the partnership, such as providing accounting services to clients in the Virgin Islands. It may outline the specific industries or sectors the partnership will serve. 6. Capital Contributions: Partnerships typically require partners to contribute capital to fund the business. The agreement will detail the initial and ongoing capital contributions required from each partner. 7. Profit Sharing: The agreement will establish how profits and losses will be allocated among partners. This may be based on the partners' capital contributions or other agreed-upon terms. 8. Decision-making: The agreement outlines how decisions will be made within the partnership, whether through unanimous consent or with a designated managing partner. It may also address methods for resolving disputes. 9. Dissolution and Exit Strategy: In the event that a partner wishes to withdraw from the partnership or if the partnership needs to be dissolved, the agreement will specify the process and any associated terms, such as the division of assets or clients. Different types of Virgin Islands Partnership Agreements Between Accountants may include variations based on the specific needs and goals of the partners involved. For instance, there could be agreements between accounting firms or agreements between individual accountants forming a partnership. Each agreement will be tailored to the circumstances and requirements of the partnering parties involved. In conclusion, a Virgin Islands Partnership Agreement Between Accountants is a vital legal document that establishes the foundation for a professional partnership in accounting services. It addresses various aspects such as business structure, capital contributions, profit-sharing, decision-making, and dissolution. The agreements can be structured based on the unique preferences and circumstances of the partners involved, contributing to a successful and harmonious partnership.