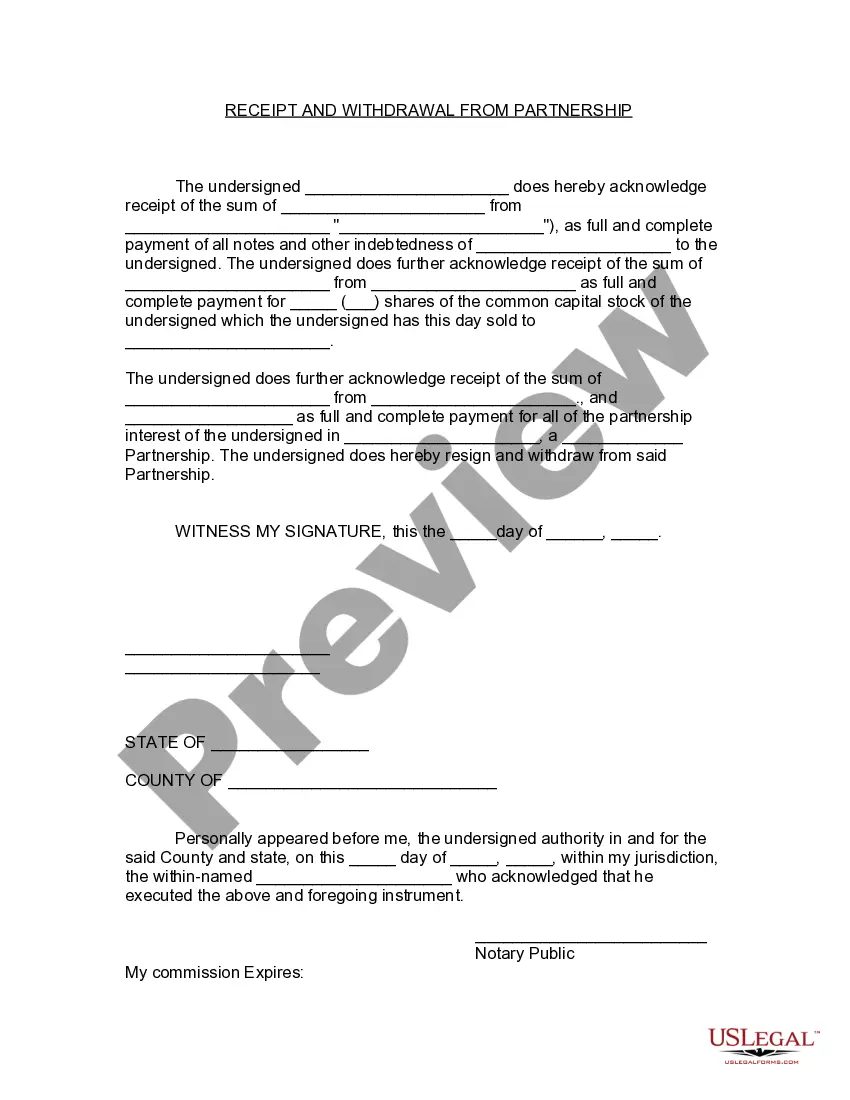

Title: Virgin Islands Receipt and Withdrawal from Partnership: Explained in Detail Introduction: Virgin Islands Receipt and Withdrawal from Partnership refers to the legal procedures involved when a partner joins a partnership or leaves an existing partnership in the Virgin Islands jurisdiction. This article will provide a comprehensive understanding of the process, its significance, and potential variations. 1. Definition and Key Considerations: Receipt and withdrawal from partnership in the Virgin Islands involve the addition or departure of a partner from an existing business entity. Partnerships can be formed as limited partnerships (LP) or general partnerships (GP), with each having variations in their receipt and withdrawal procedures. 2. Virgin Islands Receipt from Partnership: When a partner is added, often referred to as a receipt or admission, it signifies their consent to join an existing partnership. The following key points must be considered: — Partnership Agreement: The partnership agreement must be reviewed carefully, ensuring it covers the admission of new partners, profit-sharing formulas, and management responsibilities. — Legal Documentation: The incoming partner must complete the necessary legal documentation, such as a partnership agreement addendum or an amended agreement. — Financial Contribution: The new partner is expected to contribute an agreed-upon amount in terms of capital, assets, or services to the partnership. — Evaluation of Partnership Value: The partnership's existing value must be assessed to determine the incoming partner's ownership percentage and distribution of profits and losses. — Public Notice: Appropriate public notice of the new partnership may be required, fulfilling legal obligations and providing transparency to external stakeholders. — Tax Implications: Receipt from partnership may have tax implications that should be considered by both the incoming partner and the existing partnership. 3. Virgin Islands Withdrawal from Partnership: Withdrawing from a partnership in the Virgin Islands implies the departure of a partner from an existing partnership. The relevant aspects are: — Dissolution or Partnership Continuation: Depending on the terms stated in the partnership agreement, the withdrawal of a partner may lead to the dissolution of the partnership or continuation with the remaining partners. — Legal Notification: The partner wishing to withdraw should provide written notice to the other partners, incorporating the reasons and the intended date of departure. — Documentation and Financial Settlements: A comprehensive exit agreement should be prepared, addressing the partner's share in the partnership assets, liabilities, and any pending legal or financial obligations. — Distribution of Assets and Revaluation: Upon withdrawal, the departing partner's interests are distributed among the remaining partners, and the partnership assets may need to be revalued. — Tax Implications: The withdrawal may have tax implications for both the departing partner and the partnership, which need to be ascertained and addressed. Types of Virgin Islands Receipt and Withdrawal from Partnership: — Limited Partnership Receipt and Withdrawal: Specific regulations and considerations pertain to the admission and withdrawal of partners in a limited partnership setup. — General Partnership Receipt and Withdrawal: The receipt and withdrawal procedures in a general partnership may differ from those of a limited partnership. It is essential to identify and adhere to the appropriate guidelines. — Amalgamation of Partnerships: In certain cases, a partnership entity may merge with another partnership or undergo a reconstitution, leading to a different set of procedures for receipt and withdrawal. Conclusion: Virgin Islands Receipt and Withdrawal from Partnership entails the admission and departure of partners from a partnership in the Virgin Islands jurisdiction. These processes necessitate careful consideration of legal obligations, financial arrangements, partnership valuation, tax implications, and documentation. Understanding the specific type of partnership, whether limited or general, is vital for accurately navigating the receipt and withdrawal procedures.

Virgin Islands Receipt and Withdrawal from Partnership

Description

How to fill out Virgin Islands Receipt And Withdrawal From Partnership?

US Legal Forms - one of the largest libraries of legal forms in the United States - gives an array of legal file layouts you are able to obtain or print. Using the web site, you can get a large number of forms for business and person uses, categorized by types, claims, or search phrases.You can find the most recent variations of forms like the Virgin Islands Receipt and Withdrawal from Partnership in seconds.

If you already have a subscription, log in and obtain Virgin Islands Receipt and Withdrawal from Partnership in the US Legal Forms collection. The Acquire switch can look on every kind you view. You have access to all previously downloaded forms from the My Forms tab of your own accounts.

In order to use US Legal Forms the first time, listed here are basic instructions to help you started off:

- Be sure you have selected the proper kind for your area/county. Click on the Preview switch to review the form`s content. Look at the kind information to actually have chosen the proper kind.

- In case the kind does not suit your needs, make use of the Lookup industry towards the top of the display screen to get the one which does.

- In case you are pleased with the shape, validate your selection by visiting the Get now switch. Then, opt for the prices strategy you prefer and provide your references to sign up for an accounts.

- Process the deal. Utilize your bank card or PayPal accounts to perform the deal.

- Pick the format and obtain the shape on the device.

- Make alterations. Complete, edit and print and indication the downloaded Virgin Islands Receipt and Withdrawal from Partnership.

Each template you included with your money lacks an expiration date and is yours forever. So, if you would like obtain or print one more copy, just proceed to the My Forms portion and then click about the kind you require.

Obtain access to the Virgin Islands Receipt and Withdrawal from Partnership with US Legal Forms, probably the most considerable collection of legal file layouts. Use a large number of professional and condition-particular layouts that meet up with your small business or person demands and needs.