Virgin Islands Agreement to Continue Business Between Surviving Partners and Legal Representative of Deceased Partner

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement To Continue Business Between Surviving Partners And Legal Representative Of Deceased Partner?

You are capable of dedicating time online searching for the proper legal document template that meets the federal and state standards you require.

US Legal Forms provides a vast collection of legal forms that have been reviewed by experts.

You can obtain or create the Virgin Islands Agreement to Continue Business Between Remaining Partners and Legal Representative of Deceased Partner through their service.

If available, use the Preview button to take a look at the document template simultaneously.

- If you already have a US Legal Forms account, you can Log In and click the Obtain button.

- After that, you can complete, edit, create, or sign the Virgin Islands Agreement to Continue Business Between Remaining Partners and Legal Representative of Deceased Partner.

- Every legal document template you purchase is yours permanently.

- To get another copy of any purchased form, go to the My documents tab and click the relevant button.

- If you are visiting the US Legal Forms site for the first time, follow the simple instructions below.

- First, make sure you have selected the right document template for the county/town of your choice.

- Check the form description to ensure you've chosen the appropriate form.

Form popularity

FAQ

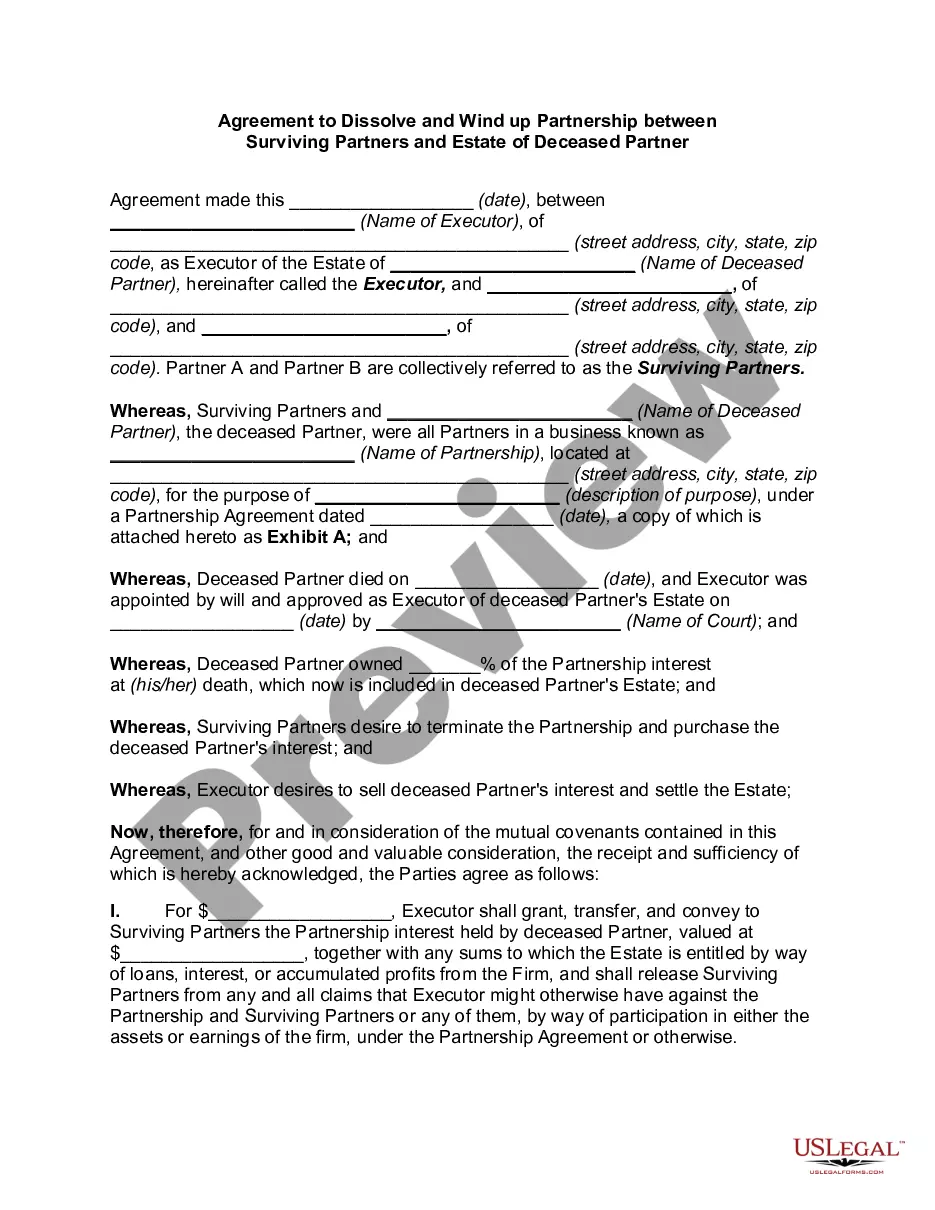

The Supreme Court held as under: Section 42(c) of the Partnership Act can appropriately be applied to a' partnership where there are more than two partners. If one of them dies, the firm is dissolved; but if there is a contract to the contrary, the surviving partners will continue the firm.

In case of death of a partner, his or her legal representative receives the amount payable to him or her by the firm. The legal representative of the deceased partner is eligible for the following amounts: The amount standing in the deceased partner's Capital A/c.

On the death of a partner, subject to any contract to the contrary, the partnership ceases to exist. Here, the contract on the contrary means the partnership need not be dissolved if it is expressly mentioned in the partnership deed that the remaining partners (not a partner) can continue the firm's business.

For the aforesaid proposition, the Court relied upon Section 42(c) of Indian Partnership Act, 1932 which provided for dissolution of a partnership upon the death of a partner and noting that in this case, once the partnership comes to an end, by virtue of death of one of the partners, there would not be any partnership

On the death of a partner, subject to any contract to the contrary, the partnership ceases to exist. Here, the contract on the contrary means the partnership need not be dissolved if it is expressly mentioned in the partnership deed that the remaining partners (not a partner) can continue the firm's business.

Keeping it successful is even harder, and coping with the death of a partner may be the hardest situation of all. When that happens, your deceased partner's share in the business usually passes to a surviving spouse, either by terms of a will or simply by default as the primary heir.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

Business of a partnership firm may not come to an end due to the death of a partner. Other partners shall continue to run the business of the firm.

Keeping it successful is even harder, and coping with the death of a partner may be the hardest situation of all. When that happens, your deceased partner's share in the business usually passes to a surviving spouse, either by terms of a will or simply by default as the primary heir.

Business partnership agreement. A properly arranged and funded agreement is a legally binding contract that spells out exactly what is to happen if one of the business's owners dies. It generally calls for the survivors to buy the deceased owner's share in the business from his or her heirs.