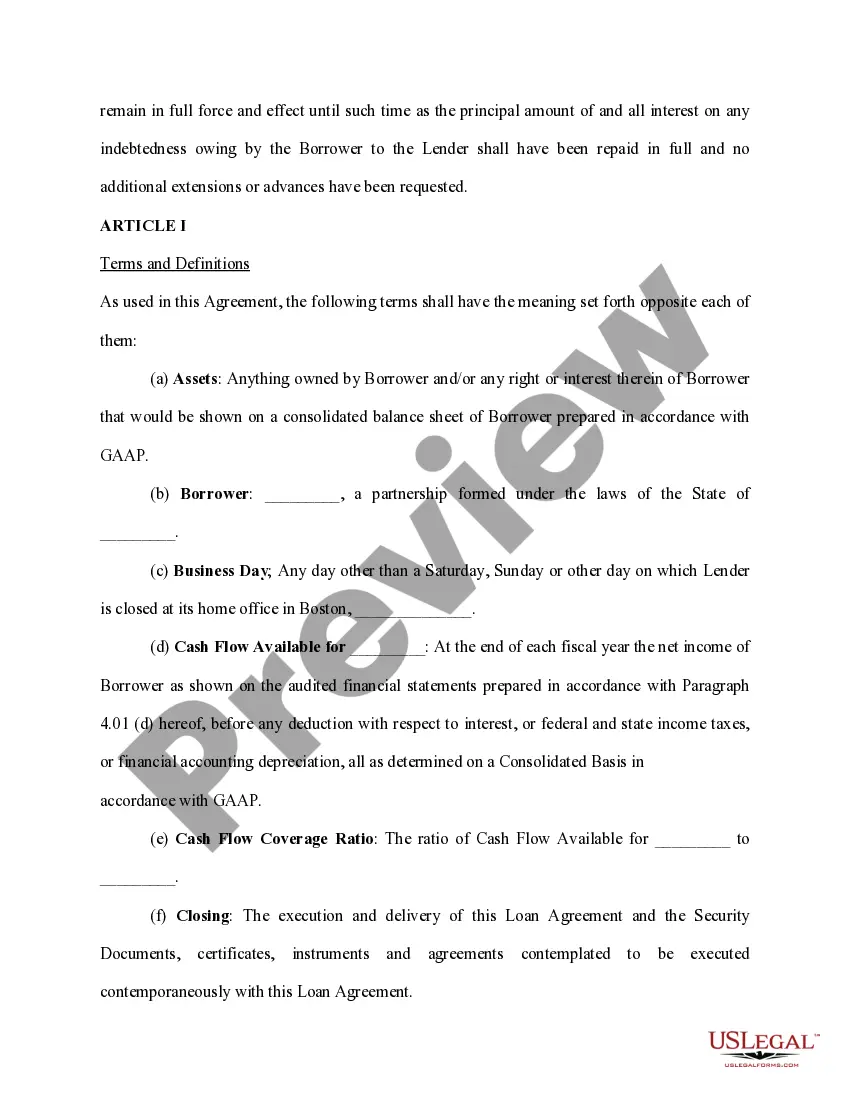

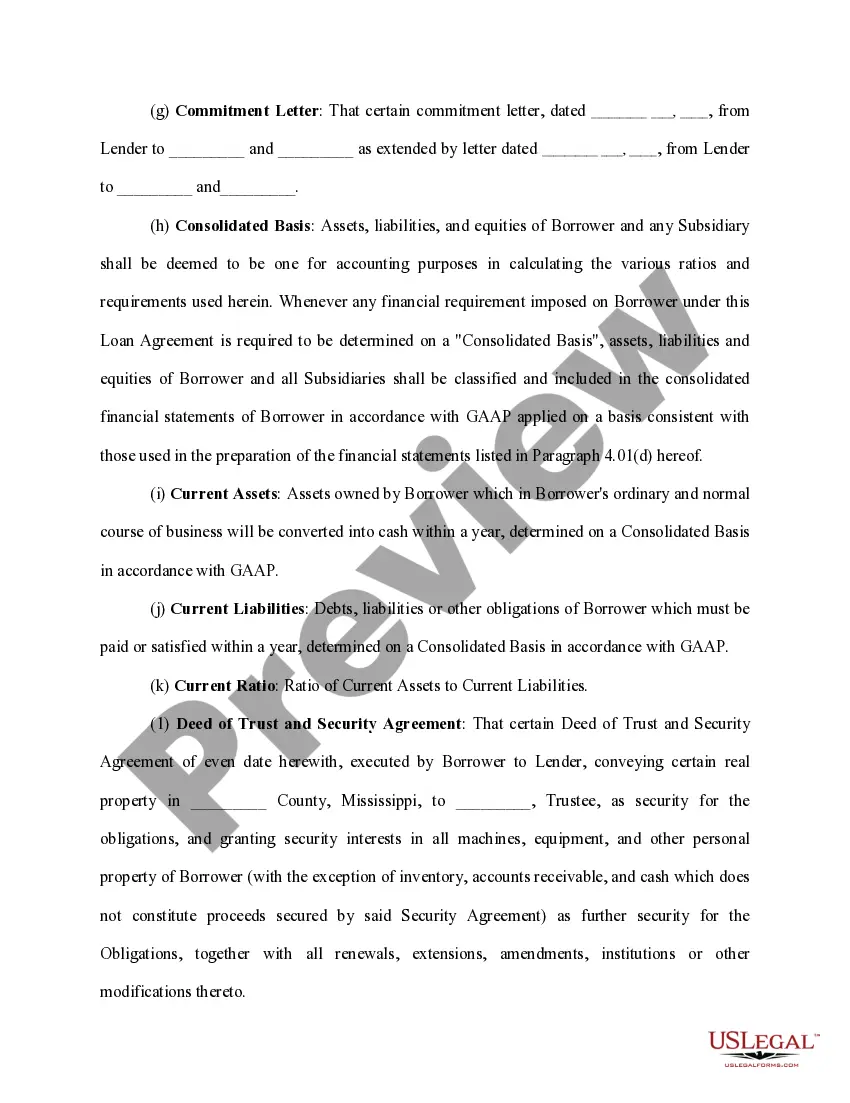

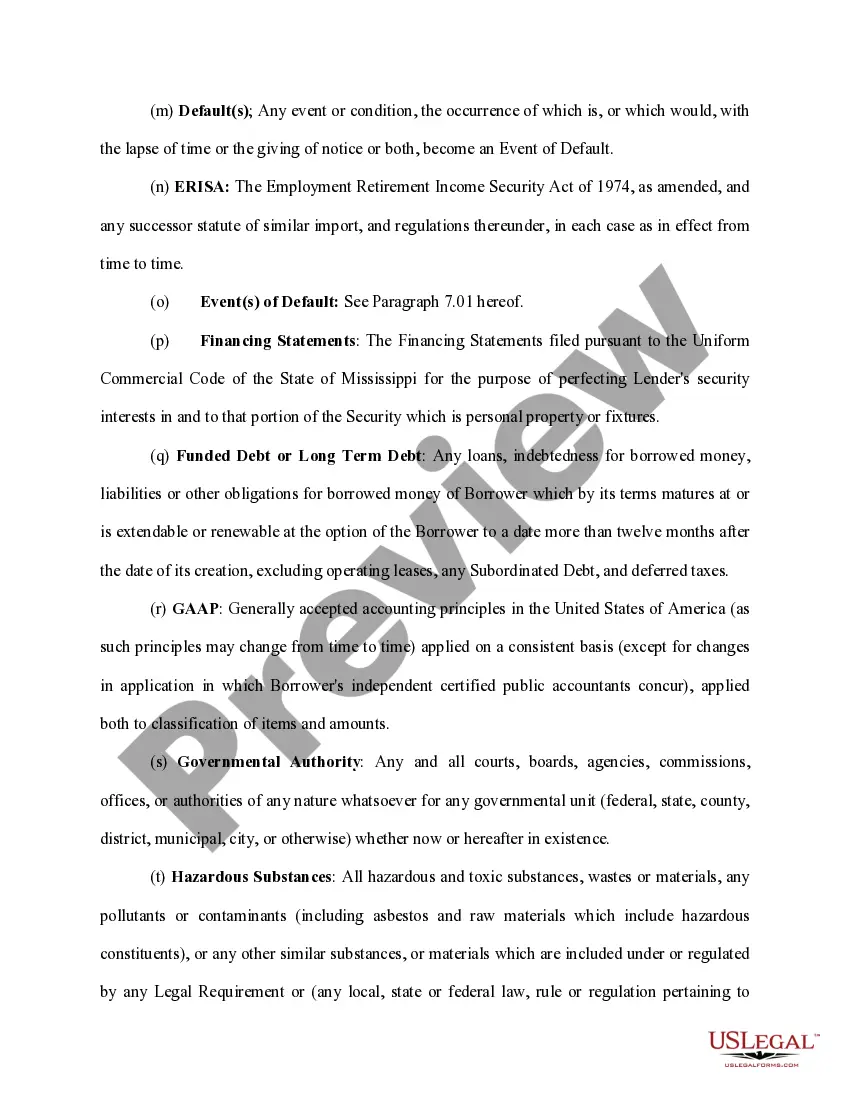

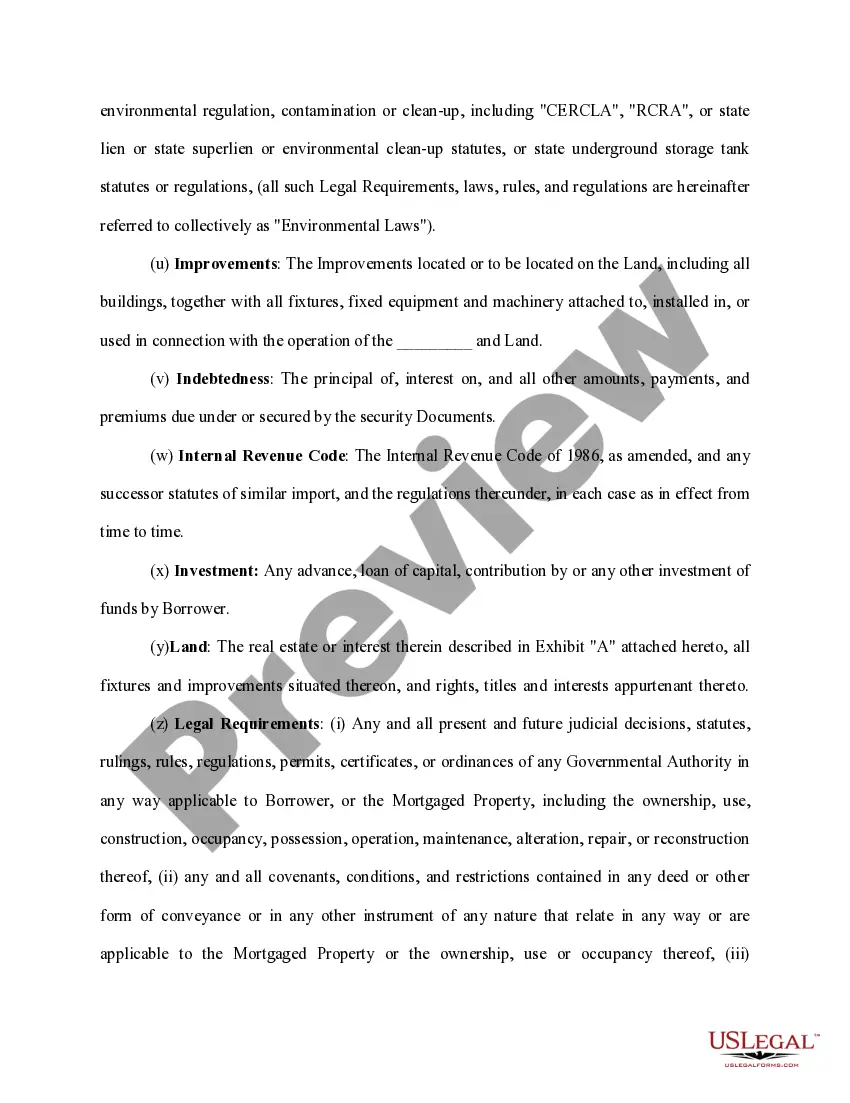

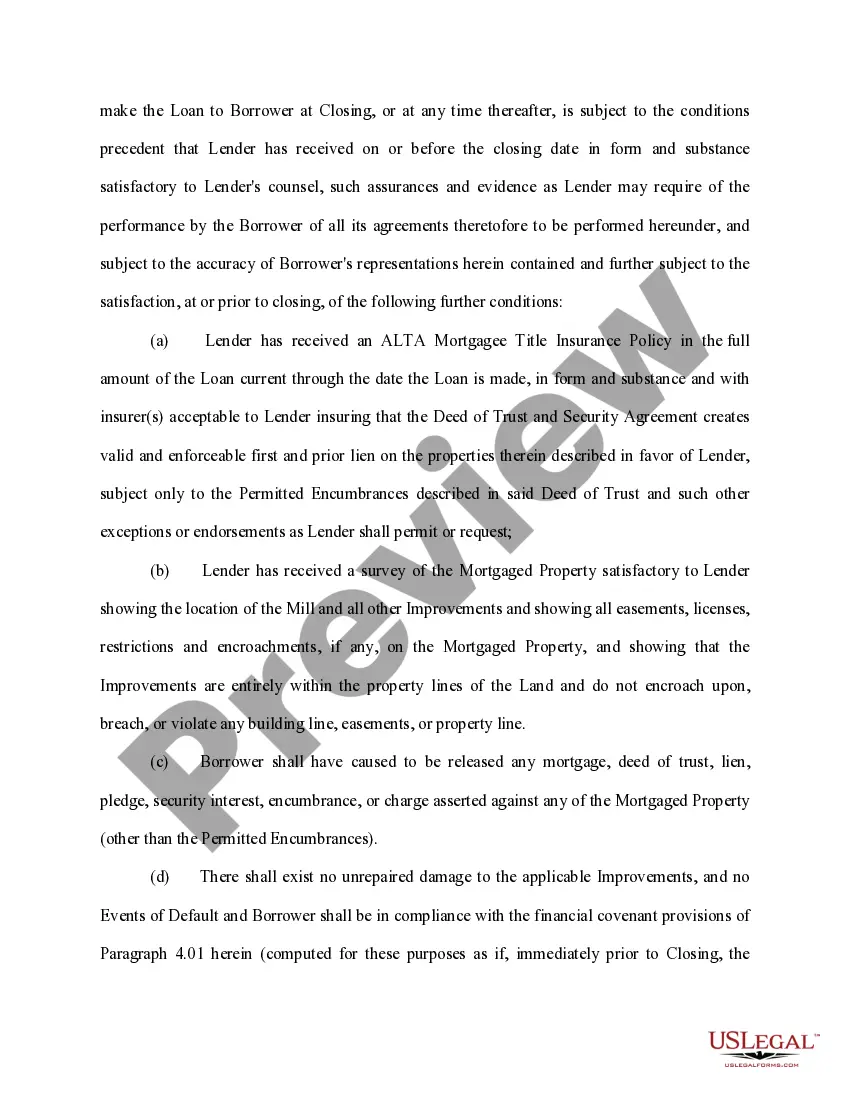

The Virgin Islands Loan Agreement for Business is a legally binding contract designed to establish the terms and conditions under which a loan will be granted to a business entity operating in the Virgin Islands. This agreement serves as a crucial document that outlines the rights and responsibilities of both parties involved in the loan transaction. The Virgin Islands Loan Agreement for Business typically consists of several essential components, including: 1. Parties involved: This section identifies the lender, who is typically a financial institution or individual, and the borrower, who is the business entity seeking financial assistance. 2. Loan terms: This section lays out the specific details of the loan, such as the principal amount, interest rate, repayment period, and any associated fees or penalties. It is important to clearly define these terms to ensure mutual understanding and to avoid potential disputes or misunderstandings. 3. Loan purpose: The agreement should explicitly state the purpose for which the loan is being obtained. It can be for various business needs, such as financing expansion projects, purchasing equipment, meeting working capital requirements, or funding other business-related activities. 4. Security or collateral: If the lender requires collateral to secure the loan, this section will detail the specific assets that the borrower pledges as security. This ensures that the lender has the right to claim those assets in the event of loan default. 5. Repayment terms: The repayment section outlines the schedule, frequency, and method of loan repayment. It may include provisions related to installment amounts, grace periods, and any late payment penalties. Clear repayment terms are crucial to avoid payment disputes and maintain a good borrower-lender relationship. 6. Default and remedies: This portion of the agreement specifies the consequences if the borrower fails to meet the agreed-upon repayment terms. It may include penalties, acceleration clauses (allowing the lender to demand immediate repayment of the entire outstanding amount), or other remedies available to the lender in case of default. Different types of Virgin Islands Loan Agreements for Business may include: 1. Term loans: These are loans with fixed repayment periods and regular installments over a predetermined time frame. Term loans are commonly used to finance long-term investments or major expenses like purchasing real estate, equipment, or vehicles. 2. Working capital loans: These loans are designed to provide businesses with short-term funding to cover day-to-day operational expenses, manage inventory, and support cash flow needs. 3. Revolving lines of credit: Unlike term loans, revolving lines of credit provide businesses with access to a predetermined credit limit, which can be utilized, repaid, and reused multiple times. This type of loan offers flexibility and is often used to manage fluctuations in cash flow or address short-term funding needs. In summary, the Virgin Islands Loan Agreement for Business is a vital legal document that outlines the terms and conditions of a loan granted to a business operating in the Virgin Islands. It ensures transparency, clarity, and mutual understanding between the lender and the borrower, safeguarding the interests of both parties.

Virgin Islands Loan Agreement for Business

Description

How to fill out Virgin Islands Loan Agreement For Business?

Have you been in the placement that you will need papers for either organization or individual reasons just about every day? There are tons of authorized papers templates available on the Internet, but discovering versions you can depend on is not simple. US Legal Forms gives thousands of develop templates, such as the Virgin Islands Loan Agreement for Business, that are composed in order to meet federal and state specifications.

When you are currently familiar with US Legal Forms web site and possess an account, simply log in. Following that, you are able to acquire the Virgin Islands Loan Agreement for Business web template.

Should you not offer an account and wish to begin using US Legal Forms, abide by these steps:

- Find the develop you want and ensure it is for the correct metropolis/county.

- Make use of the Review key to review the shape.

- Look at the explanation to actually have selected the proper develop.

- In the event the develop is not what you`re seeking, utilize the Search discipline to discover the develop that fits your needs and specifications.

- Once you get the correct develop, click Purchase now.

- Pick the rates program you desire, fill in the necessary info to make your account, and pay for the transaction using your PayPal or Visa or Mastercard.

- Choose a handy document formatting and acquire your duplicate.

Find every one of the papers templates you possess purchased in the My Forms food list. You may get a further duplicate of Virgin Islands Loan Agreement for Business any time, if necessary. Just go through the required develop to acquire or printing the papers web template.

Use US Legal Forms, the most extensive variety of authorized varieties, to conserve time as well as steer clear of faults. The support gives expertly manufactured authorized papers templates which you can use for a variety of reasons. Generate an account on US Legal Forms and start creating your lifestyle easier.

Form popularity

FAQ

How to Write a Business Loan Agreement Step 1 ? Set an Effective Date. ... Step 2 ? Identify the Parties. ... Step 3 ? Include the Loan Amount. ... Step 4 ? Create a Repayment Schedule. ... Step 5 ? Define Security Interests or Collateral. ... Step 6 ? Set an Interest Rate. ... Step 7 ? Late Payment Fees. ... Step 8 ? Determine Prepayment Options.

What is a Commercial Loan Agreement? A commercial loan agreement is a legal contract that outlines the terms and conditions of a business owner's line of credit. This type of financing helps small businesses put capital to work to grow their company.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

What Is a Commercial Loan? A commercial loan is a debt-based funding arrangement between a business and a financial institution such as a bank. It is typically used to fund major capital expenditures and/or cover operational costs that the company may otherwise be unable to afford.

A commercial loan is a form of credit that is extended to support business activity. Examples include operating lines of credit and term loans for property, plant and equipment (PP&E).

A Commercial Loan Agreement can be defined as a legally binding contract entered into between a lender, generally a bank, and a borrower, detailing all aspects and features of the monetary transfer involved in the commercial loan process.

Unlike residential loans, the terms of commercial loans typically range from five years (or less) to 20 years, and the amortization period is often longer than the term of the loan. A lender, for example, might make a commercial loan for a term of seven years with an amortization period of 30 years.

A business loan agreement is a legal document between you and your lender, whether that's a bank, credit union, online lender or even a family member. It serves both parties by clarifying everything about the loan, including its repayment schedule and any collateral that secures it.