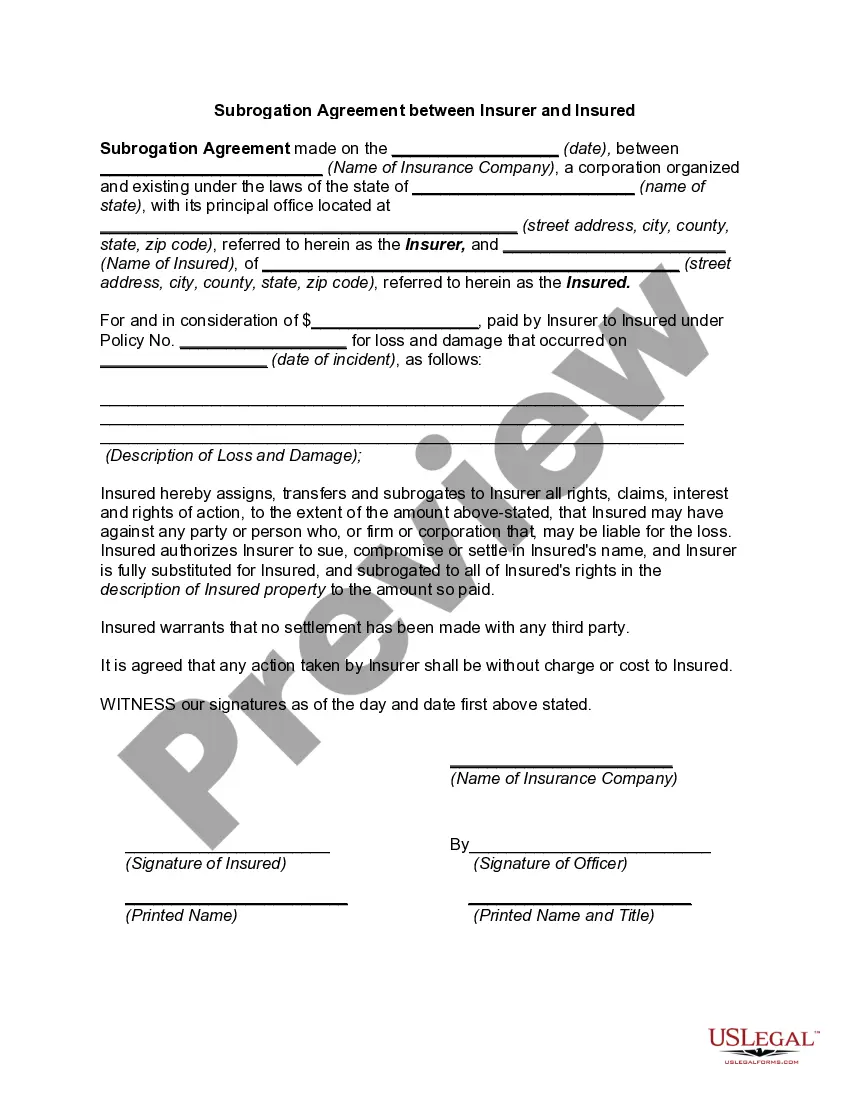

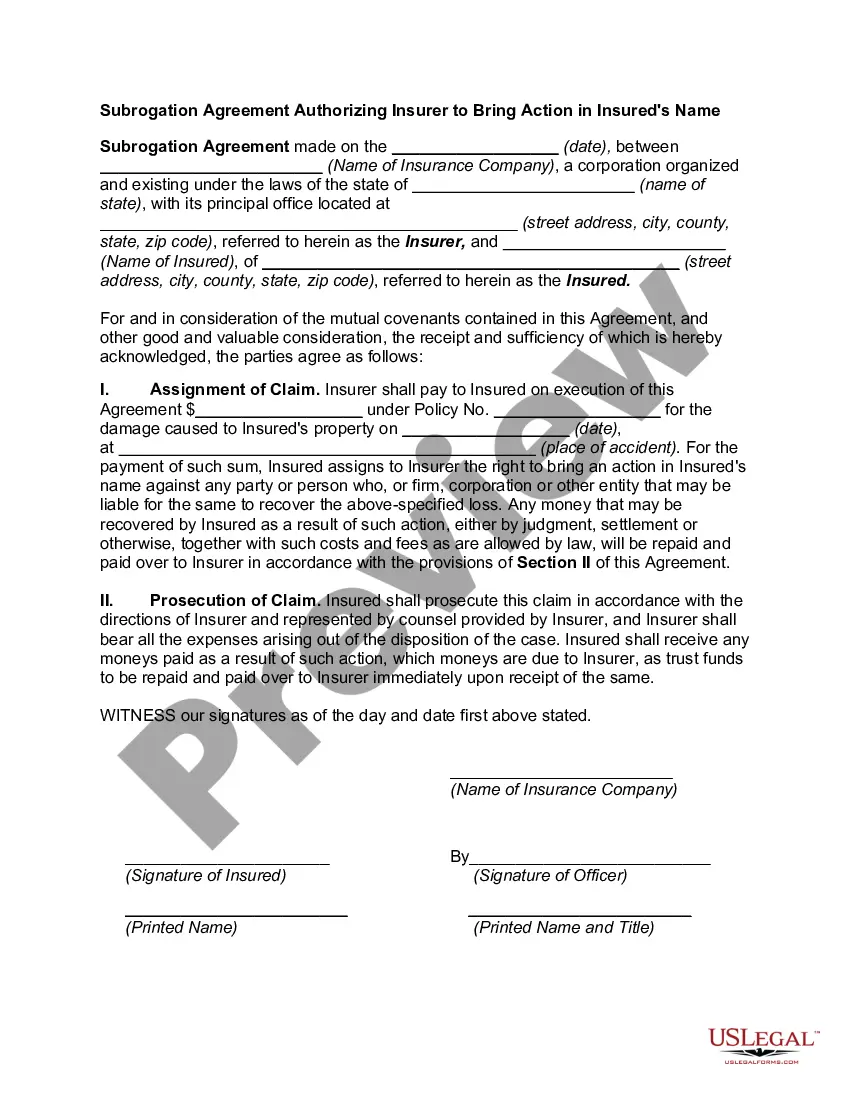

Virgin Islands Receipt for Payment of Loss for Subrogation

Description

How to fill out Receipt For Payment Of Loss For Subrogation?

Finding the right legal papers template can be quite a struggle. Of course, there are a variety of web templates available online, but how do you obtain the legal type you want? Utilize the US Legal Forms internet site. The services offers a huge number of web templates, like the Virgin Islands Receipt for Payment of Loss for Subrogation, which you can use for organization and personal requirements. All of the forms are checked by pros and meet up with state and federal specifications.

Should you be previously signed up, log in for your accounts and click on the Download key to obtain the Virgin Islands Receipt for Payment of Loss for Subrogation. Make use of accounts to appear with the legal forms you might have acquired earlier. Visit the My Forms tab of the accounts and acquire one more copy in the papers you want.

Should you be a whole new user of US Legal Forms, listed here are basic directions for you to comply with:

- Initially, make certain you have selected the proper type for the metropolis/region. It is possible to examine the shape utilizing the Review key and read the shape description to make certain it will be the best for you.

- When the type does not meet up with your needs, make use of the Seach industry to get the correct type.

- Once you are certain the shape is acceptable, go through the Buy now key to obtain the type.

- Choose the rates prepare you would like and type in the needed details. Create your accounts and buy an order with your PayPal accounts or bank card.

- Select the data file structure and download the legal papers template for your system.

- Full, modify and produce and indication the received Virgin Islands Receipt for Payment of Loss for Subrogation.

US Legal Forms is the most significant library of legal forms that you can discover different papers web templates. Utilize the service to download expertly-made paperwork that comply with express specifications.

Form popularity

FAQ

The insured's loss results in the insurer's obligation to pay the proceeds of the insurance policy. An insurance policy is the insurance contract that describes the conditions and circumstances under which the insurer will indemnify the insured or other named beneficiaries.

Most insurance policies require that the policyholder provide a signed Proof of Loss within 60 days of the insurance company's request.

Deductible. The amount of the loss which the insured is responsible to pay before benefits from the insurance company are payable. You may choose a higher deductible to lower your premium.

The Principle of Indemnity The insurance company promises to compensate the policyholder for the amount of the loss up to the amount agreed upon in the contract.

Subrogation allows your insurer to recoup costs (medical payments, repairs, etc.), including your deductible, from the at-fault driver's insurance company, if the accident wasn't your fault. A successful subrogation means a refund for you and your insurer.

Subrogation is a term describing a right held by most insurance carriers to legally pursue a third party that caused an insurance loss to the insured. This is done in order to recover the amount of the claim paid by the insurance carrier to the insured for the loss.

The theory behind a subrogation clause is that the insurance company should not have to bear the loss when someone else was to blame for the damages. Once the insurance company has paid the claim to the policyholder, it may look to see whether it can take legal action against another party to recover its losses.

Indemnity is a type of insurance compensation paid for damage or loss. When the term is used in the legal sense, it also may refer to an exemption from liability for damage. Indemnity is a contractual agreement between two parties in which one party agrees to pay for potential losses or damage caused by another party.