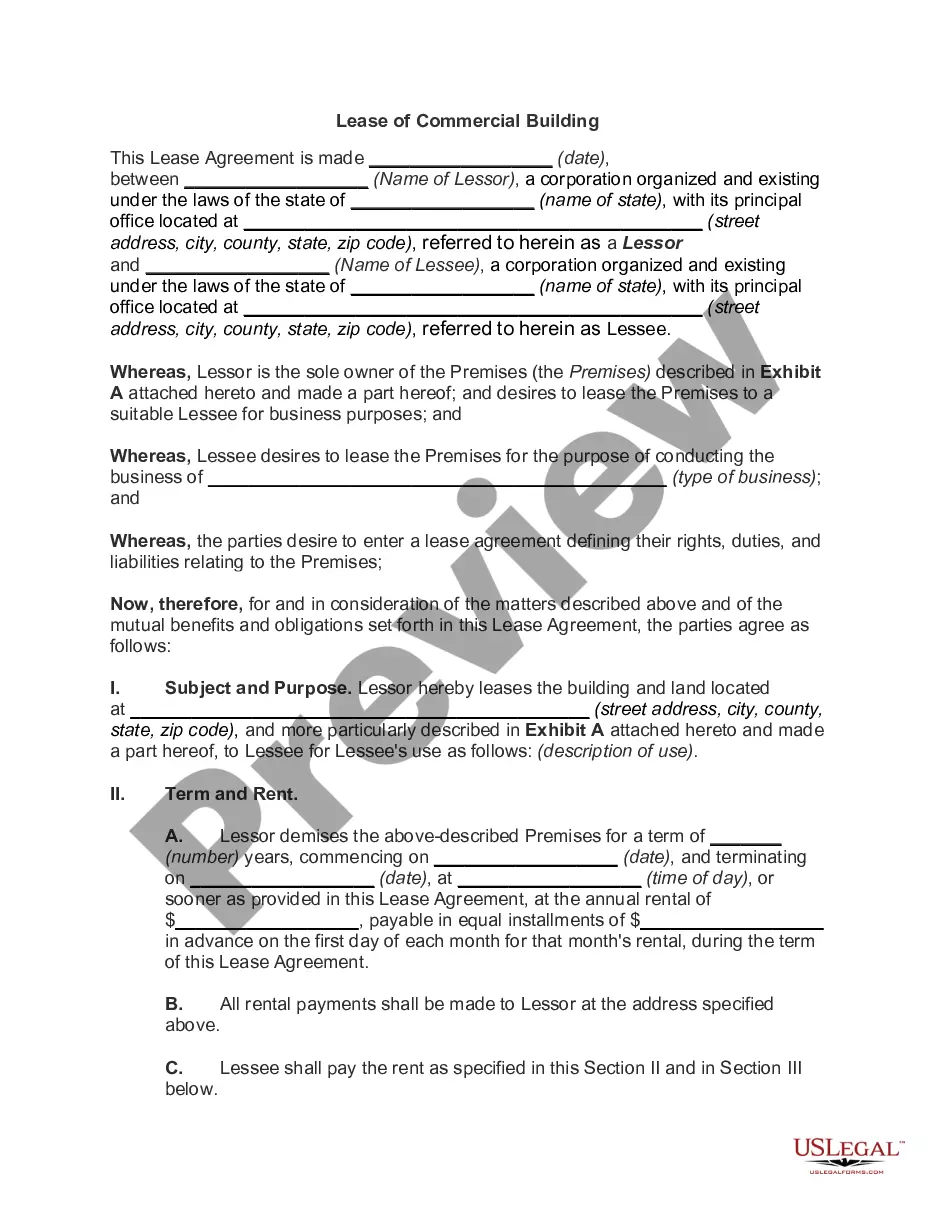

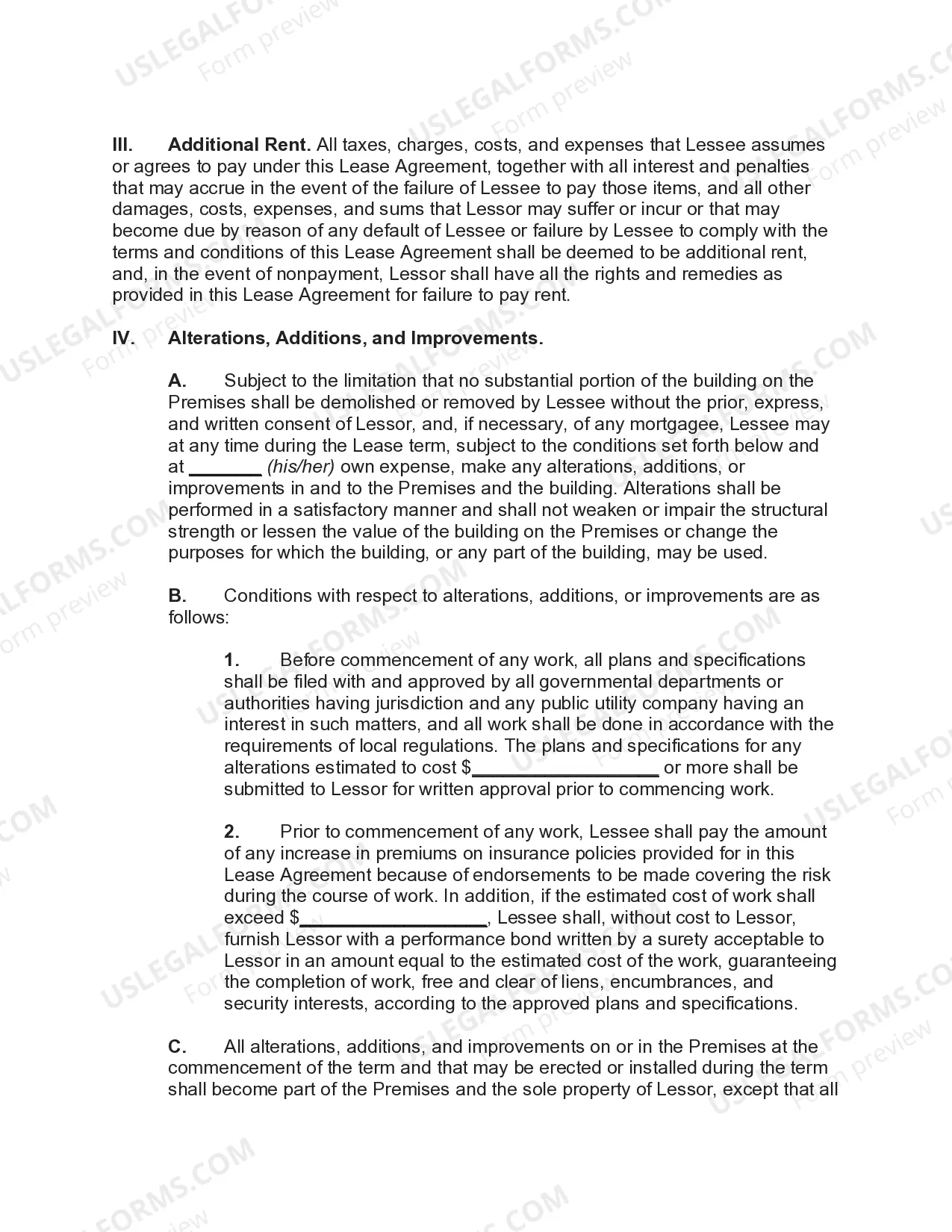

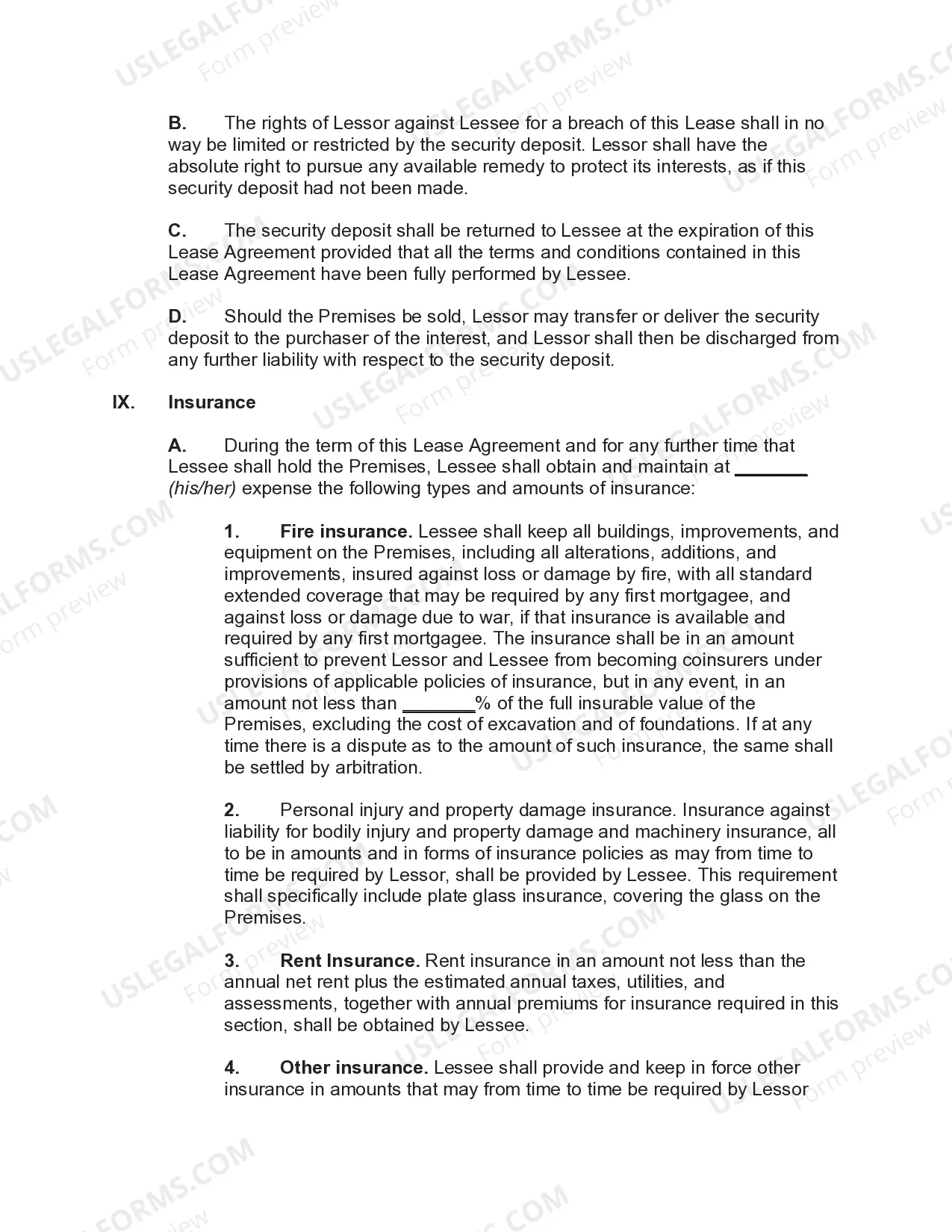

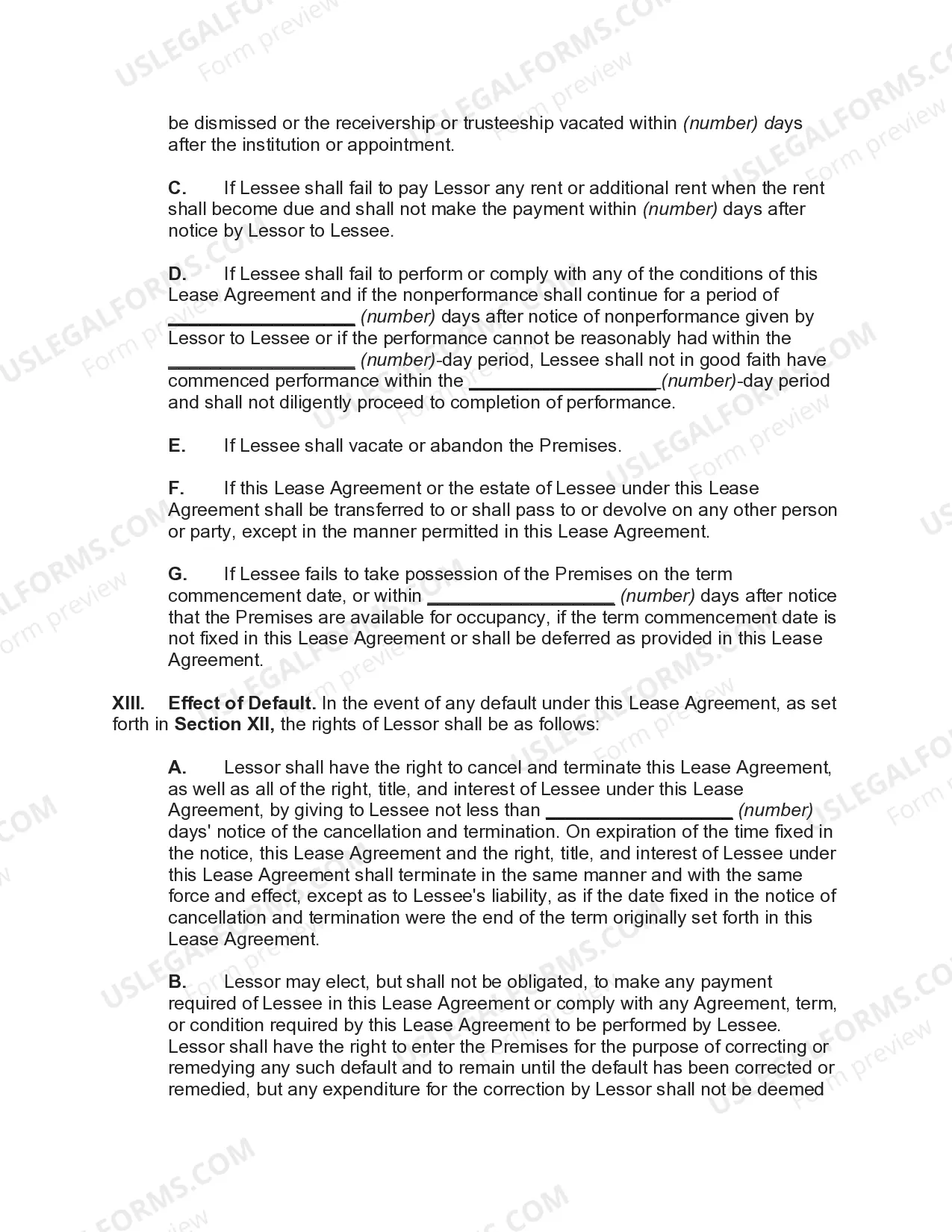

A Virgin Islands lease of a commercial building refers to the legal agreement entered into by the owner (lessor) and a tenant (lessee) for the rental of commercial property in the Virgin Islands, a group of islands located in the Caribbean Sea. This contractual arrangement allows businesses to occupy and utilize the property for their commercial activities in exchange for regular rental payments. Virgin Islands Commercial Building Lease Agreement: 1. Triple Net Lease: A common type of lease, where the lessee assumes responsibility for all property-related costs, including real estate taxes, insurance, and maintenance expenses. 2. Gross Lease: This lease type requires the lessor to bear most property expenses, including taxes and maintenance costs, while the lessee pays a fixed monthly rent. 3. Percentage Lease: Often used in retail spaces, the tenant pays a base monthly rent plus a percentage of their sales revenue. 4. Short-term Lease: Typically a lease agreement for a period of one year or less, suitable for businesses with temporary needs, such as pop-up stores or seasonal businesses. 5. Long-term Lease: A lease that extends for a significant duration, usually multiple years, providing stability and security for tenants planning for long-term business operations. 6. Sublease: In some cases, the original lessee may sublet the commercial building to a third party, known as the sublessee, who then pays rent and assumes limited rights and responsibilities. When entering a Virgin Islands commercial building lease, several key elements are typically included: — Rental Amount: The agreed-upon monthly or annual rent to be paid by the lessee. — Lease Term: Specifies the duration of the lease agreement, including the start and end dates. — Renewal Options: Specifies if the lease can be renewed after its expiration and under what terms. — Security Deposit: A refundable deposit paid by the lessee to protect against damages or breach of lease terms. — Maintenance and Repairs: Clearly outlines the party responsible for property upkeep, repairs, and maintenance costs. — Improvements and Modifications: Establishes guidelines for tenant modifications to the commercial building and handles ownership of such improvements at the lease's end. — Permitted Use: Specifies the authorized business activities that can be conducted on the premises. — Termination Clause: Outlines the conditions under which either party can terminate the lease agreement before its stated expiration date. Before signing a Virgin Islands lease of a commercial building, it is crucial for both parties to carefully review and negotiate the terms, seek legal advice, and understand their rights and obligations to ensure a mutually beneficial agreement.

Virgin Islands Lease of Commercial Building

Description

How to fill out Virgin Islands Lease Of Commercial Building?

Are you currently in a placement in which you need to have paperwork for sometimes business or specific functions nearly every day time? There are plenty of legitimate file templates available on the Internet, but locating types you can depend on isn`t simple. US Legal Forms offers thousands of form templates, much like the Virgin Islands Lease of Commercial Building, that are published in order to meet federal and state needs.

In case you are presently acquainted with US Legal Forms internet site and have an account, just log in. Following that, you can down load the Virgin Islands Lease of Commercial Building web template.

Should you not provide an account and would like to begin to use US Legal Forms, abide by these steps:

- Discover the form you will need and make sure it is for that right metropolis/state.

- Utilize the Preview option to analyze the form.

- See the outline to actually have selected the right form.

- When the form isn`t what you`re trying to find, take advantage of the Research field to get the form that fits your needs and needs.

- When you obtain the right form, just click Buy now.

- Pick the prices plan you want, fill in the desired info to make your account, and buy the order utilizing your PayPal or charge card.

- Choose a hassle-free file structure and down load your duplicate.

Find all of the file templates you have bought in the My Forms food selection. You may get a extra duplicate of Virgin Islands Lease of Commercial Building at any time, if possible. Just click on the needed form to down load or print out the file web template.

Use US Legal Forms, probably the most considerable variety of legitimate kinds, to conserve efforts and stay away from faults. The assistance offers skillfully created legitimate file templates which can be used for a range of functions. Make an account on US Legal Forms and begin generating your life a little easier.