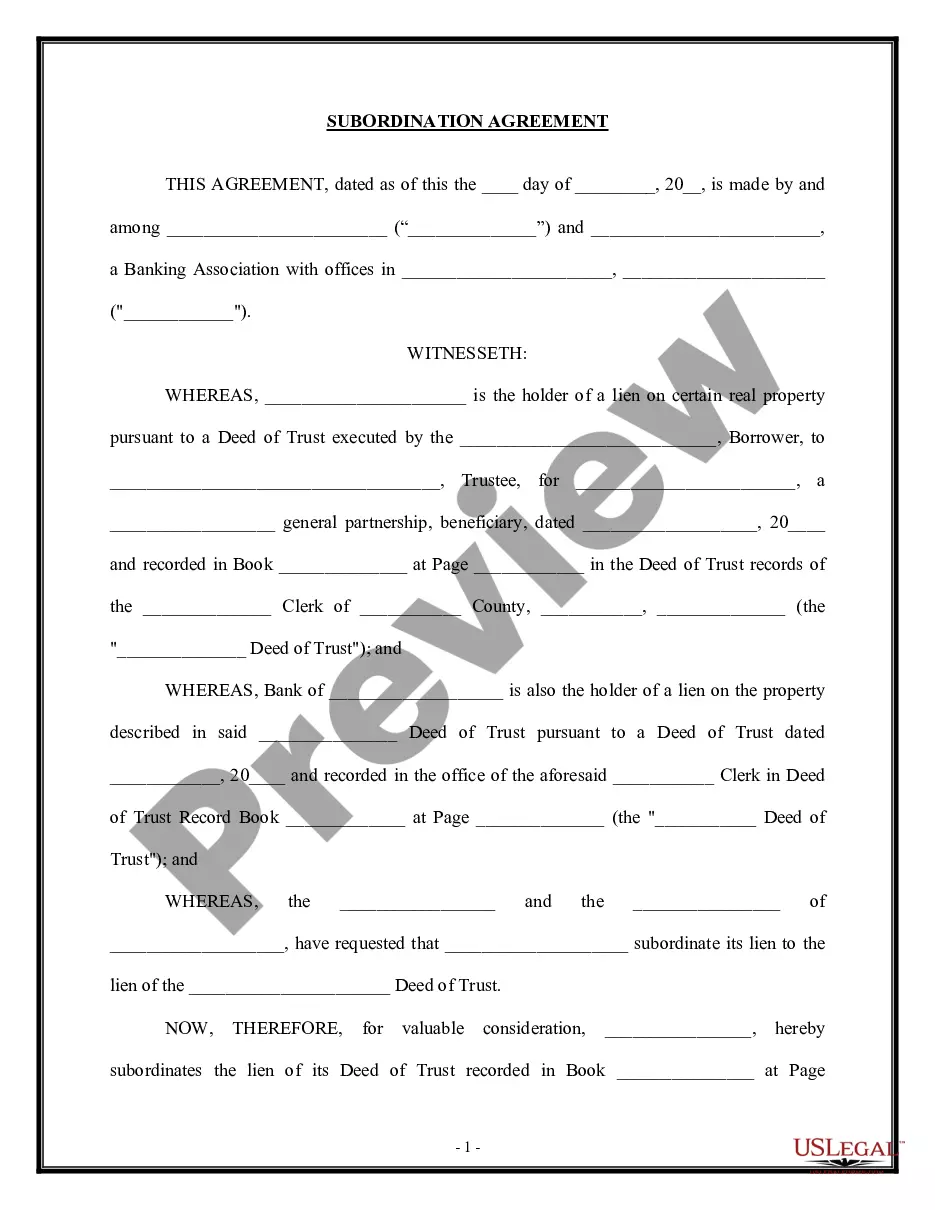

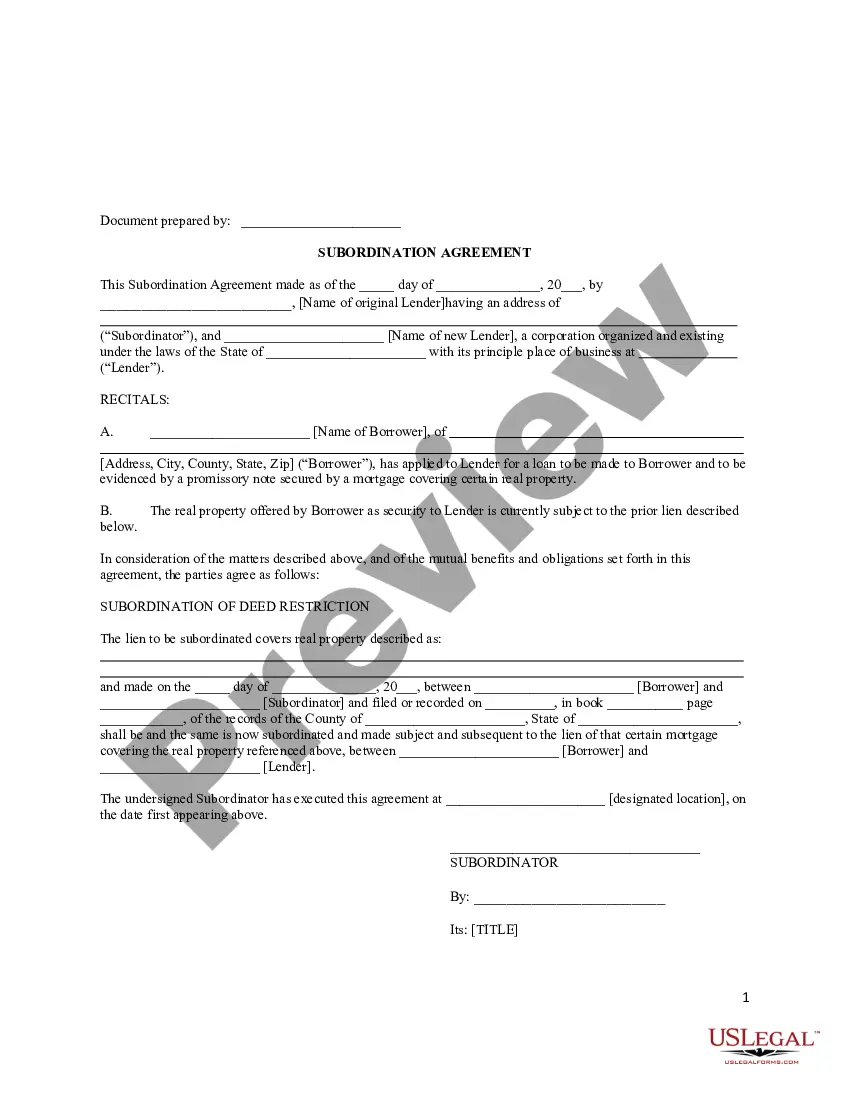

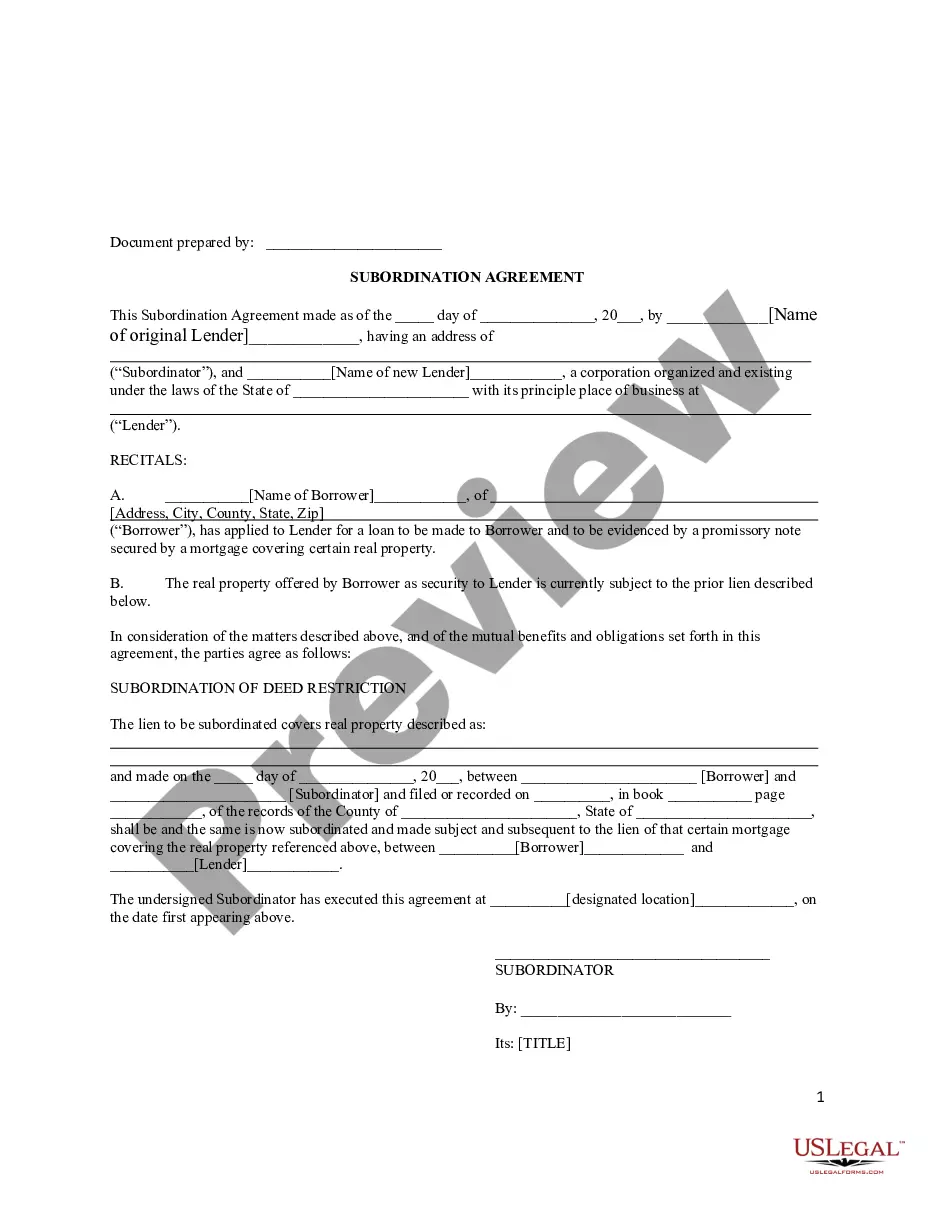

Virgin Islands Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Are you presently inside a place the place you will need papers for either business or specific uses just about every working day? There are a variety of legal file templates available on the Internet, but finding ones you can trust isn`t simple. US Legal Forms delivers a large number of form templates, like the Virgin Islands Subordination Agreement Subordinating Existing Mortgage to New Mortgage, that are created in order to meet state and federal requirements.

Should you be previously acquainted with US Legal Forms site and get a free account, basically log in. Next, it is possible to obtain the Virgin Islands Subordination Agreement Subordinating Existing Mortgage to New Mortgage format.

Should you not come with an account and need to start using US Legal Forms, abide by these steps:

- Get the form you will need and make sure it is for your correct city/county.

- Take advantage of the Review button to review the form.

- Look at the information to actually have chosen the proper form.

- When the form isn`t what you`re looking for, take advantage of the Lookup field to discover the form that fits your needs and requirements.

- If you obtain the correct form, just click Get now.

- Pick the rates strategy you need, fill in the necessary information and facts to produce your bank account, and pay for your order using your PayPal or Visa or Mastercard.

- Decide on a hassle-free data file formatting and obtain your backup.

Locate every one of the file templates you have purchased in the My Forms menu. You can obtain a extra backup of Virgin Islands Subordination Agreement Subordinating Existing Mortgage to New Mortgage any time, if necessary. Just click on the required form to obtain or print out the file format.

Use US Legal Forms, one of the most substantial collection of legal forms, to conserve efforts and prevent errors. The services delivers appropriately created legal file templates that you can use for an array of uses. Make a free account on US Legal Forms and start creating your daily life easier.

Form popularity

FAQ

A subordinated loan agreement (SLA) must be filed with NFA at least ten days prior to the proposed effective date of the agreement.

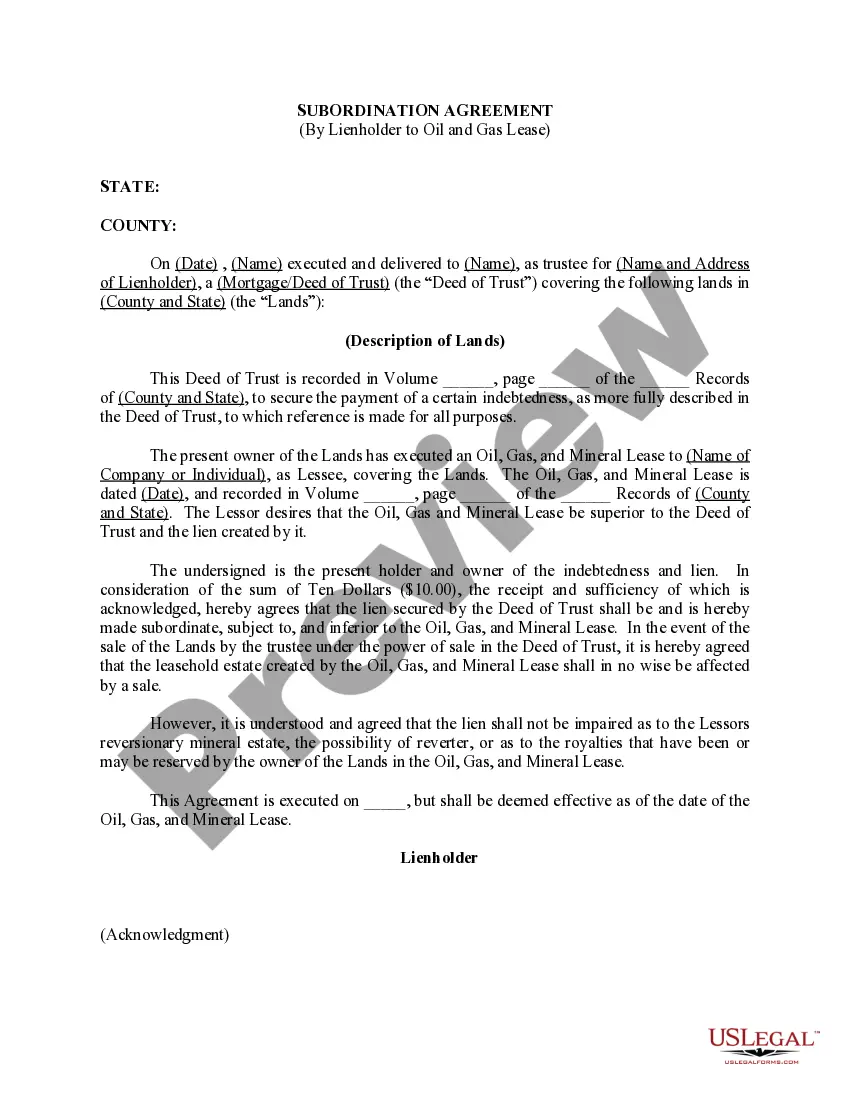

Subordination agreements may be included in existing deeds of trust or may be outlined in an independent contract. In situations where two deeds of trust are being recorded concurrently, the lien priority is typically handled by instructing the title company as to which security instrument will be recorded first.

A subordination clause serves to protect the lender if a homeowner defaults. If this happens, the lender then has the legal standing to repossess the home and cover their loan's outstanding balance first. If other subordinate mortgages are involved, the secondary liens will take a backseat in this process.

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date.

A subordination real estate mortgage clause gives the loan it's in reference to first lien position. It states that any other loans or liens on the property take a second lien position. Most first mortgage lenders won't fund a loan unless there is a subordination clause giving them first lien position.

Lenders can execute what are referred to as executory subordination agreements. Executory subordination agreements are essentially a promise to enter into a subordination agreement in the future if another loan enters the picture, like a construction loan.

A subordination agreement must be signed and acknowledged by a notary and recorded in the official records of the county to be enforceable.

Any subsequent loan that is taken out after your initial purchase loan is considered to be a junior-lien or subordinate mortgage. Therefore, subordinate financing is the use of two or more mortgages to finance the purchase of real estate or using your home's equity for liquid cash.