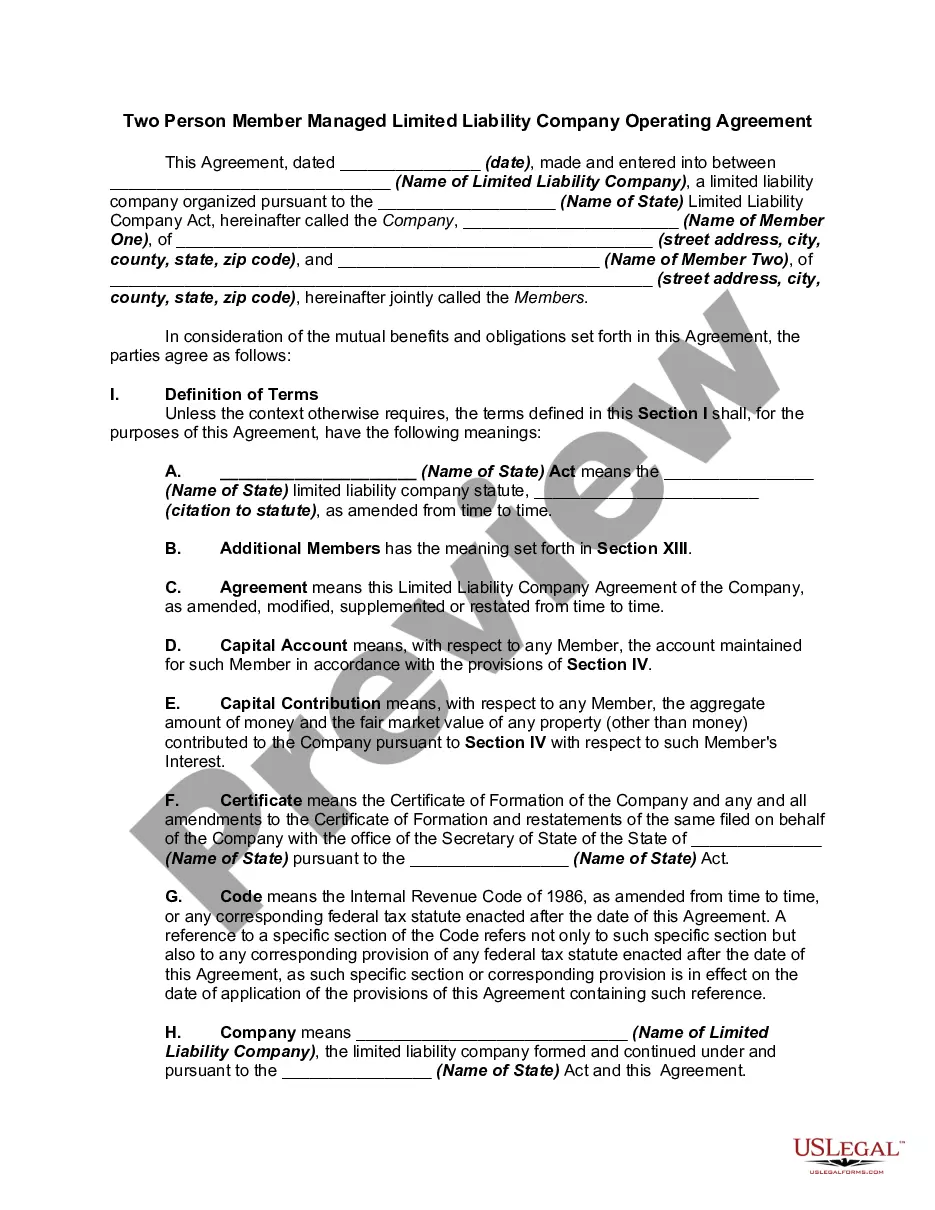

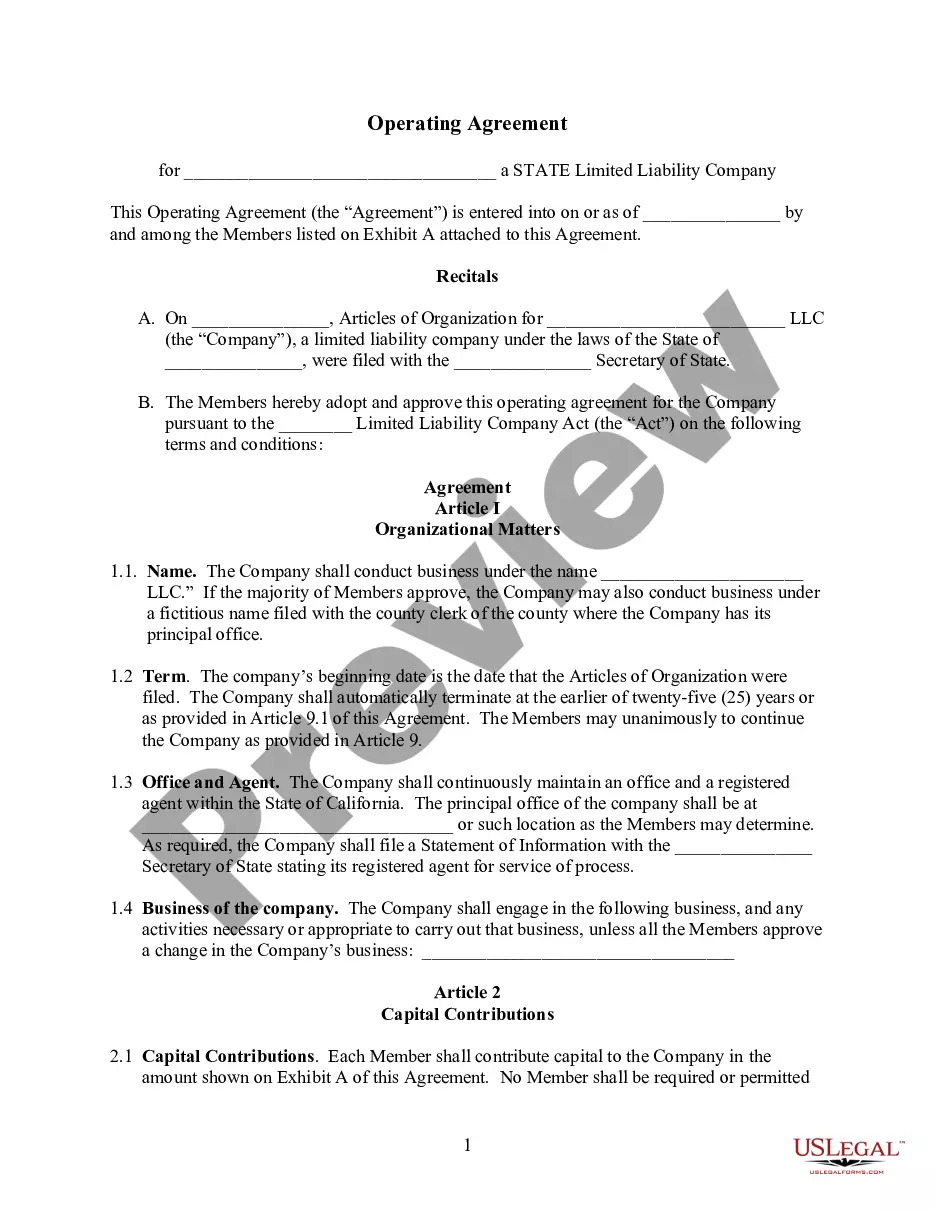

Virgin Islands LLC Operating Agreement for Two Partners

Description

How to fill out LLC Operating Agreement For Two Partners?

If you wish to fully access, download, or print authorized document templates, utilize US Legal Forms, the largest collection of legal forms available online.

Take advantage of the site's simple and convenient search to find the documents you require. Numerous templates for business and personal purposes are categorized by types, jurisdictions, or keywords.

Use US Legal Forms to locate the Virgin Islands LLC Operating Agreement for Two Partners in just a few clicks.

Every legal document template you acquire is yours permanently. You will have access to every form you downloaded within your account. Click on the My documents section and select a form to print or download again.

Compete and download, and print the Virgin Islands LLC Operating Agreement for Two Partners with US Legal Forms. There are thousands of professional and state-specific forms you can use for your business or personal needs.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to obtain the Virgin Islands LLC Operating Agreement for Two Partners.

- You can also access forms you have previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure that you have chosen the form for the correct state/territory.

- Step 2. Utilize the Preview option to review the form's content. Don’t forget to check the details.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find other versions of the legal form template.

- Step 4. Once you have found the form you need, select the Purchase now button. Choose the payment plan you prefer and enter your credentials to register for an account.

- Step 5. Complete the transaction. You can use your Visa or Mastercard or PayPal account to finalize the purchase.

- Step 6. Choose the format of the legal form and download it to your system.

- Step 7. Complete, modify, and print or sign the Virgin Islands LLC Operating Agreement for Two Partners.

Form popularity

FAQ

A BVI company can be incorporated quickly, with a flexible organisational structure and minimal financial reporting requirements. BVI companies are ideal for startup companies as they can be operated from anywhere in the world and there are no restrictions on where a BVI company can carry out its business.

Tax year and filing requirements There is no requirement for BVI companies to submit a tax return since there is no corporation tax in the BVI.

To get started:Create a business plan.Register your trade name and/or corporation with the Office of the Lieutenant Governor.Select a good location and obtain a copy of an unsigned lease or letter of intent from the owner.Obtain a business license from the V.I. Department of Licensing and Consumer Affairs (DLCA)

There are no strict reporting requirements in BVI and an IBC does not need to prepare financial statements or company accounts. The company should maintain only those accounts or records which the company directors consider to be necessary for their own use; and these can be kept anywhere in the world.

Here are the steps to incorporating in the British Virgin Islands:Step 1: Reserve your Company Name. The first step is to reserve a company name with the BVI Registry.Step 2: Appoint a Registered Agent.Step 3: Open a bank account.Step 4: Submit all relevant documents.

Unlike most U.S. states, the USVI requires corporations to have a minimum of three directors, three officers, a president, treasurer and secretary. Corporate directors are not allowed. Stock must also be registered and there is a minimum capital requirement of $1,000.

Anyone can form a limited liability company (LLC) in the USA; you don't need to be a US citizen or a US company. Foreign citizens and foreign companies can form an LLC in the USA.

To start a business in the U.S. Virgin Islands you will need to obtain a business license from the Department of Licensing and Consumer Affairs (DLCA). DLCA will complete the "One Step" review process with the following government agencies: Police Department. VI Bureau of Internal Revenue (tax clearance)

Those looking to form LLCs in the US Virgin Islands must have both a local registered agent and a local office address. This address will be used for process service requests. Your agent who forms the company for you (such as this one) should automatically include this for you in the initial filing.

There are no accounting and audit requirements. However, under The BVI Mutual Legal Assistance (Tax Matters) (Amendment) Act, 2012, Companies are required to retain records and underlying documentation for a period of at last five years from the date of transaction.