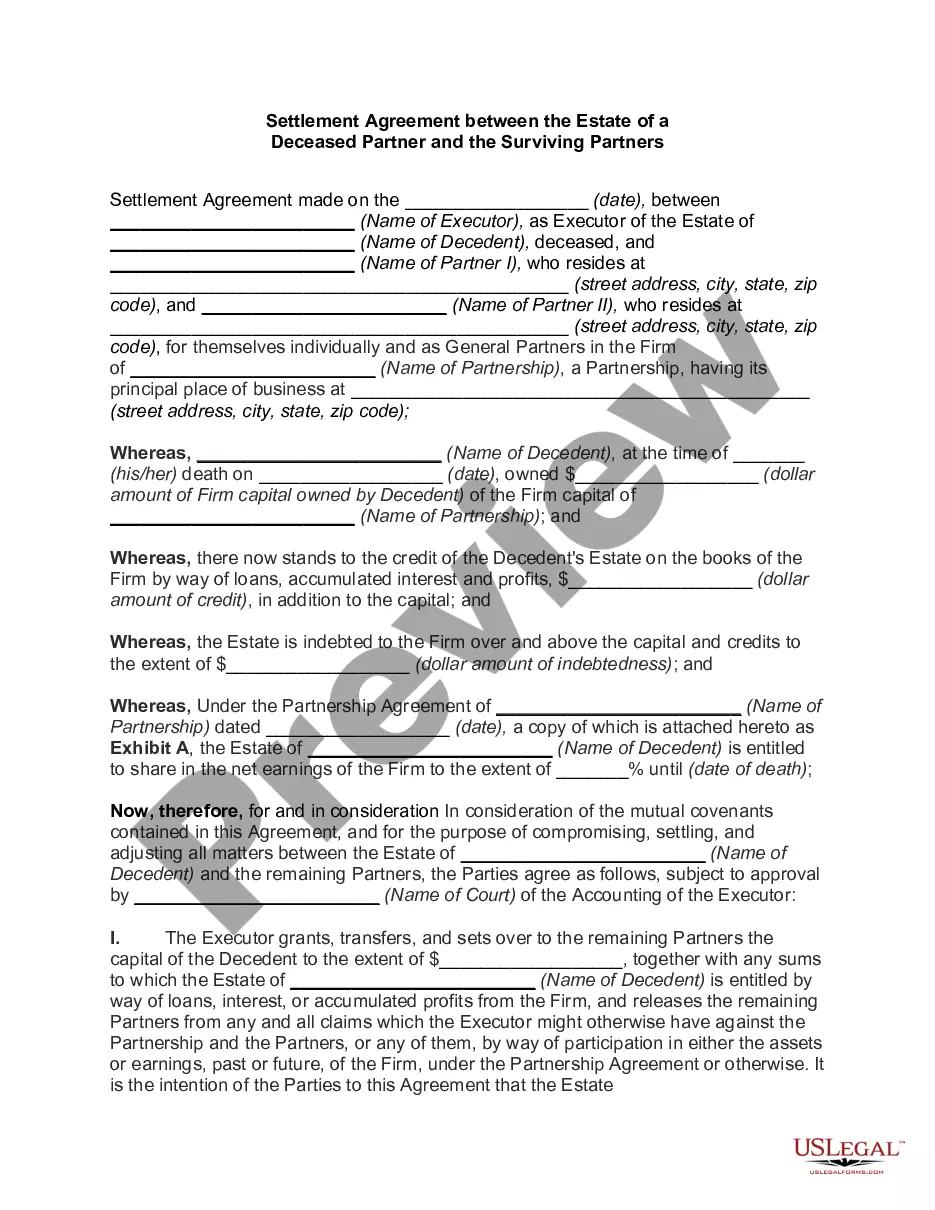

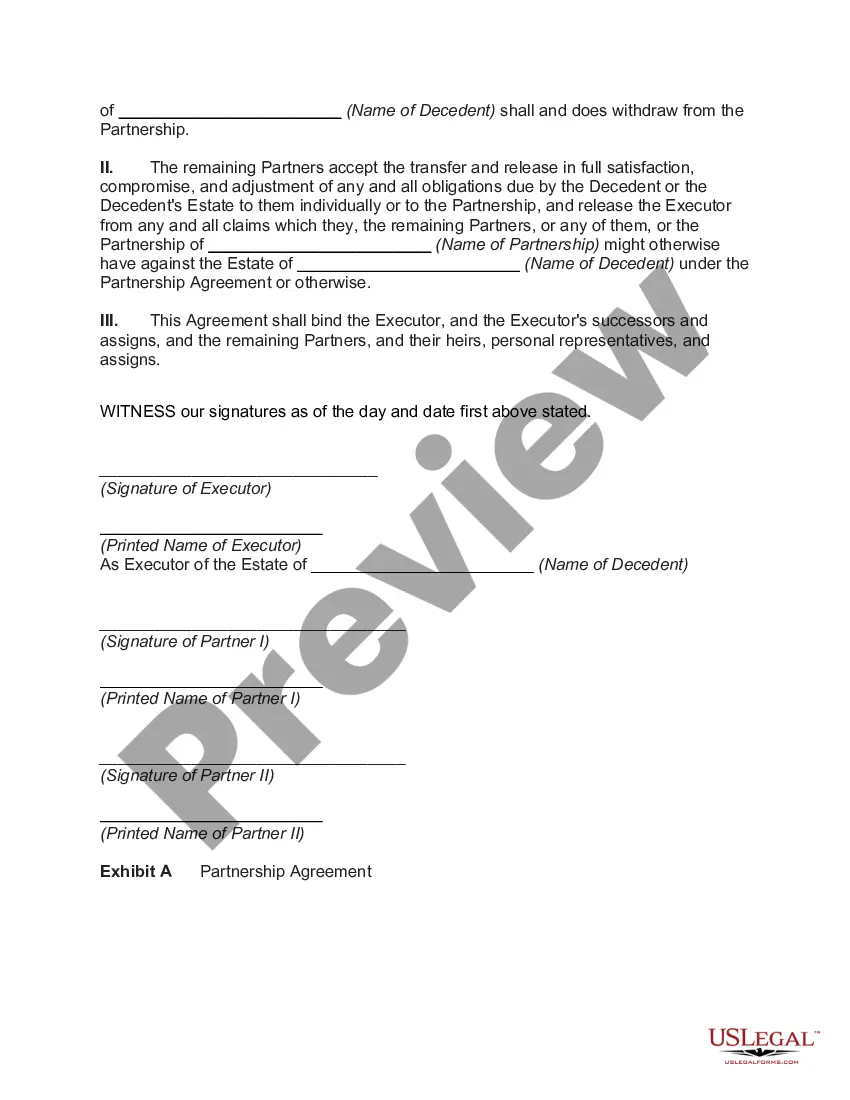

Title: Understanding the Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners Introduction: The Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners is a legal document that governs the resolution of assets, liabilities, and interests following the death of a partner in a business or partnership. This agreement plays a crucial role in ensuring a smooth transition and equitable distribution of the deceased partner's estate. In this article, we will delve into the intricacies of this agreement, its significance, and potential variations. Key Terms and Keywords: 1. Virgin Islands Settlement Agreement 2. Deceased Partner 3. Surviving Partners 4. Estate 5. Business Partnership 6. Assets 7. Liabilities 8. Transition 9. Equitable Distribution Types of Virgin Islands Settlement Agreement: 1. Comprehensive Settlement Agreement: This type of settlement agreement encompasses all aspects related to the partner's estate, including assets, liabilities, debts, rights, obligations, and interests. It provides a comprehensive framework for resolving these matters and is suitable for complex partnerships with significant assets or multiple surviving partners. 2. Asset-Specific Settlement Agreement: In certain cases, there may be a need to focus solely on a specific asset or group of assets held by the deceased partner in the business. An asset-specific settlement agreement is designed to address the distribution, valuation, and transfer of these specific assets. This type of agreement may be suitable when there are minimal liabilities or an agreement regarding other assets has already been reached. 3. Debt Resolution Settlement Agreement: If the deceased partner had outstanding debts or obligations, a debt resolution settlement agreement can be utilized to specify how these will be resolved. This agreement may involve the surviving partners assuming responsibility for the debts, arranging for repayment, or negotiating with creditors to settle outstanding amounts. It focuses primarily on the financial aspects of the partner's estate. 4. Profit Sharing Settlement Agreement: Partnerships often involve shared profits and revenue. In some cases, a settlement agreement may be required to outline how the deceased partner's share will be distributed among the surviving partners or their estates. This agreement ensures transparency and avoids disputes by clearly defining how future profits will be allocated. Conclusion: The Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners is a vital legal instrument that facilitates the smooth and fair resolution of assets, liabilities, and interests following the death of a partner. Whether opting for a comprehensive agreement, an asset-specific agreement, a debt resolution agreement, or a profit-sharing agreement, the involved parties should seek the assistance of legal professionals to ensure compliance with the relevant laws and achieve a fair and equitable settlement.

Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners

Description

How to fill out Virgin Islands Settlement Agreement Between The Estate Of A Deceased Partner And The Surviving Partners?

Choosing the best authorized record design can be a have a problem. Obviously, there are tons of themes available on the net, but how will you find the authorized form you want? Take advantage of the US Legal Forms website. The service gives a large number of themes, for example the Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners, which can be used for enterprise and private requirements. All of the types are examined by professionals and meet federal and state demands.

Should you be previously signed up, log in for your account and click the Acquire button to have the Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners. Utilize your account to appear throughout the authorized types you have purchased formerly. Check out the My Forms tab of the account and acquire one more copy of the record you want.

Should you be a fresh customer of US Legal Forms, allow me to share basic directions that you can follow:

- Initial, make sure you have selected the appropriate form for your metropolis/region. You can look through the shape making use of the Review button and look at the shape information to ensure it is the right one for you.

- In the event the form fails to meet your requirements, make use of the Seach field to obtain the appropriate form.

- When you are positive that the shape is suitable, click the Buy now button to have the form.

- Opt for the prices plan you desire and enter the necessary details. Build your account and pay for an order utilizing your PayPal account or charge card.

- Choose the submit formatting and down load the authorized record design for your system.

- Total, edit and print and signal the attained Virgin Islands Settlement Agreement between the Estate of a Deceased Partner and the Surviving Partners.

US Legal Forms is definitely the most significant local library of authorized types where you can find different record themes. Take advantage of the company to down load appropriately-manufactured documents that follow express demands.