Virgin Islands Agreement to Extend Closing or Completion Date

Description

How to fill out Agreement To Extend Closing Or Completion Date?

US Legal Forms - one of the most prominent collections of legal documents in the United States - offers a range of legal document templates that you can download or print.

By utilizing the website, you can find thousands of forms for business and personal needs, categorized by types, states, or keywords. You can obtain the latest versions of forms such as the Virgin Islands Agreement to Extend Closing or Completion Date within moments.

If you possess a subscription, Log In and download the Virgin Islands Agreement to Extend Closing or Completion Date from your US Legal Forms library. The Download button will appear on each form you examine. You can access all previously saved forms in the My documents section of your account.

Every template you added to your account does not have an expiration date and remains yours indefinitely. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need.

Access the Virgin Islands Agreement to Extend Closing or Completion Date through US Legal Forms, one of the most extensive libraries of legal document templates. Utilize thousands of professional and state-specific templates that fulfill your business or personal requirements.

- Ensure you have selected the correct form for your city/state. Click the Review button to inspect the form's details. Check the form information to verify that you have chosen the right form.

- If the form does not fit your requirements, use the Search field located at the top of the page to find one that does.

- If you are satisfied with the form, confirm your selection by clicking on the Get now button. Next, choose your preferred pricing plan and provide your information to register for an account.

- Process the payment. Utilize your credit card or PayPal account to complete the transaction.

- Select the format and download the form onto your device.

- Edit. Complete, amend, print, and sign the saved Virgin Islands Agreement to Extend Closing or Completion Date.

Form popularity

FAQ

To register a company in the British Virgin Islands, you need to choose a business structure, prepare all necessary documents, and file them with the BVI Financial Services Commission. Additionally, consider local requirements and any potential need for a registered agent. Utilizing the Virgin Islands Agreement to Extend Closing or Completion Date can streamline this process, ensuring you stay compliant with regulatory timelines.

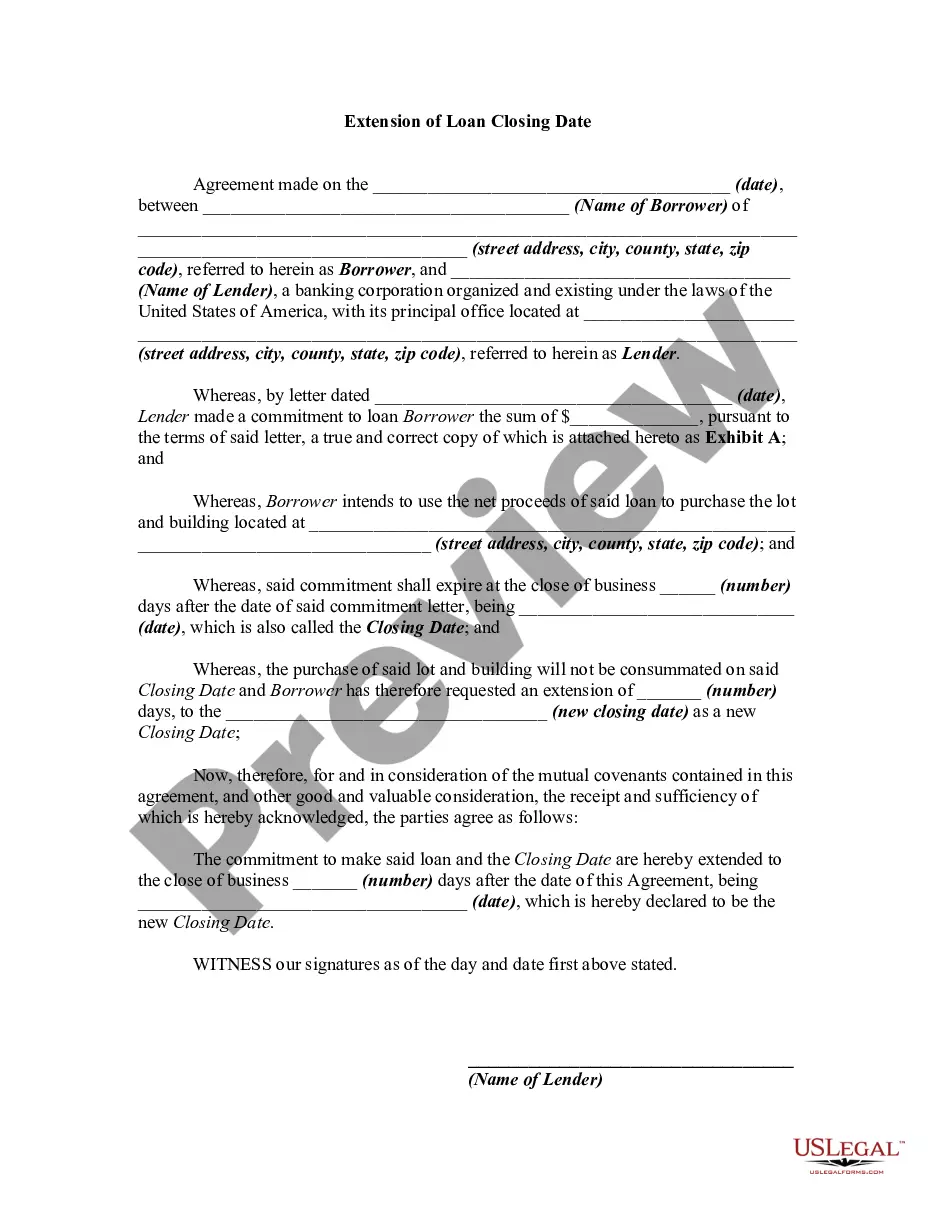

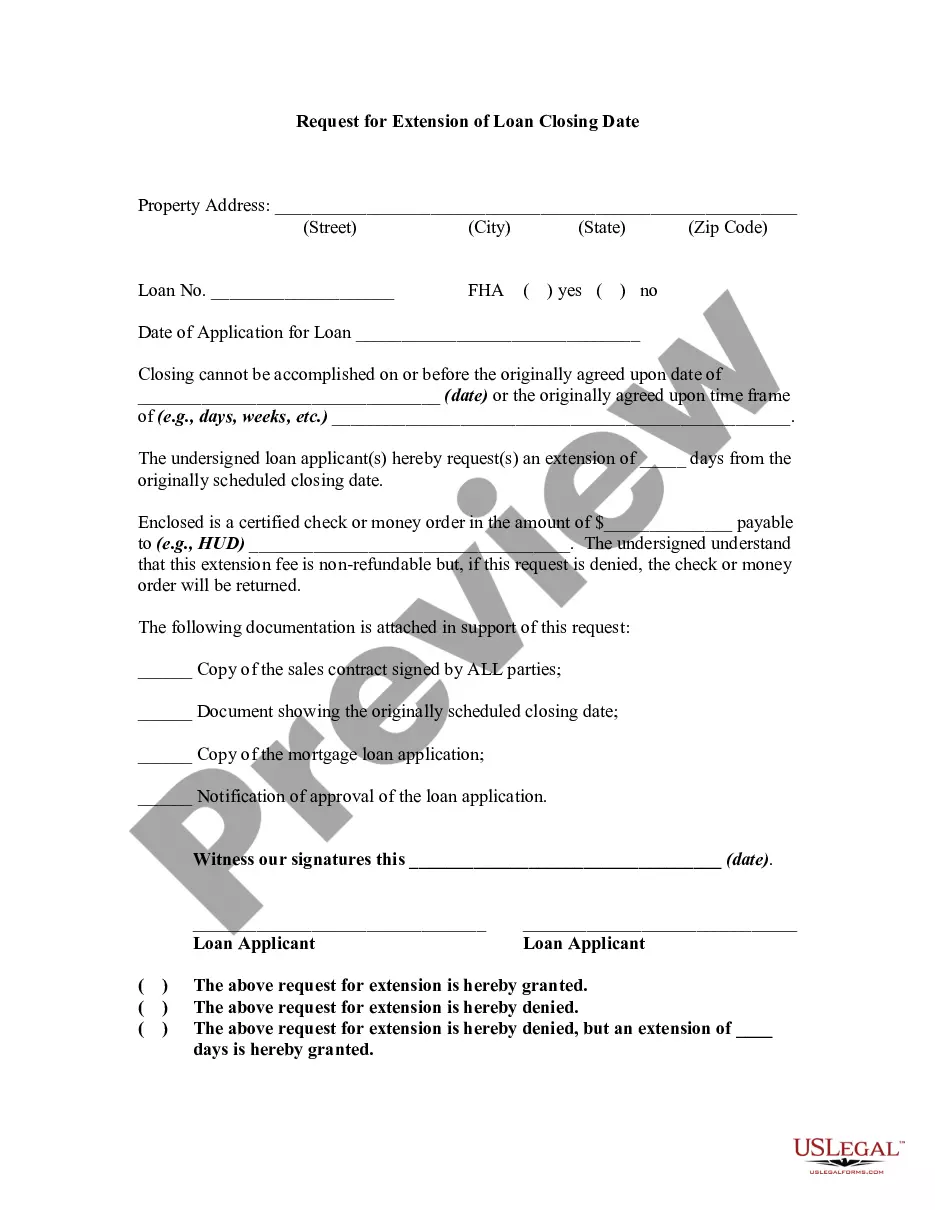

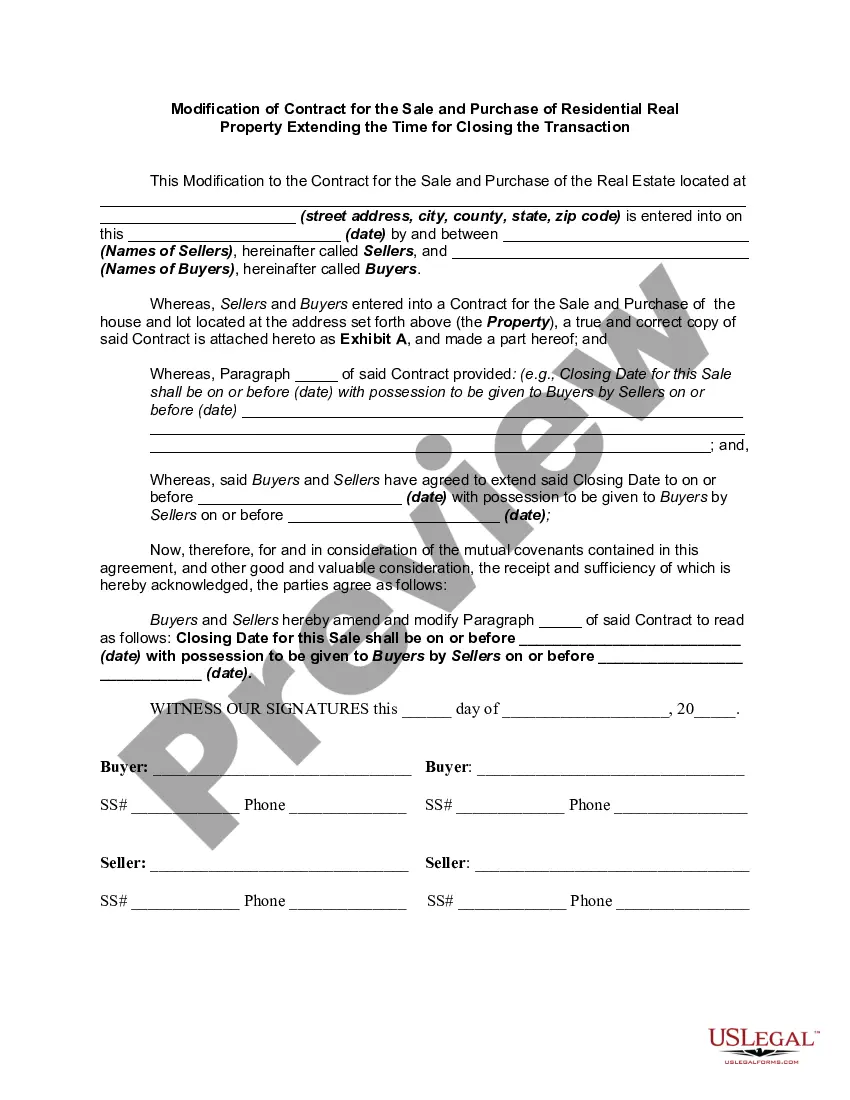

One action you can take is relatively simple: grant the buyer an extension, no strings attached. Your real estate agent can negotiate a new closing date that generally will add an additional 10 to 30 days to the closing date, giving the buyer more time to tie up their loose ends.

In all cases, a legally binding closing date is specified in a sales contract. In most circumstances, the seller can cancel the deal if the buyer is not ready to close by that date. Some contract cancellation possibilities can benefit both the buyer and the seller.

If the buyer uncovers issues but still wants to buy the house, the buyer can request the seller address the issues. If the seller agrees, both parties may agree to extend the closing date to provide the needed time for the seller to correct the issues.

What happens if the lender misses the closing date? If the lender doesn't approve your loan by the closing date, then the purchase contract may expire. The seller might agree to push back the closing date to allow you more time to get your loan, but they don't have to.

Therefore, we promote strict editorial integrity in each of our posts. A closing date is like a term paper deadline: you need to meet it. But life happens, and sometimes you need an extension. In fact, about 1 in 4 closings experience delays, according to the National Association of Realtors (NAR).

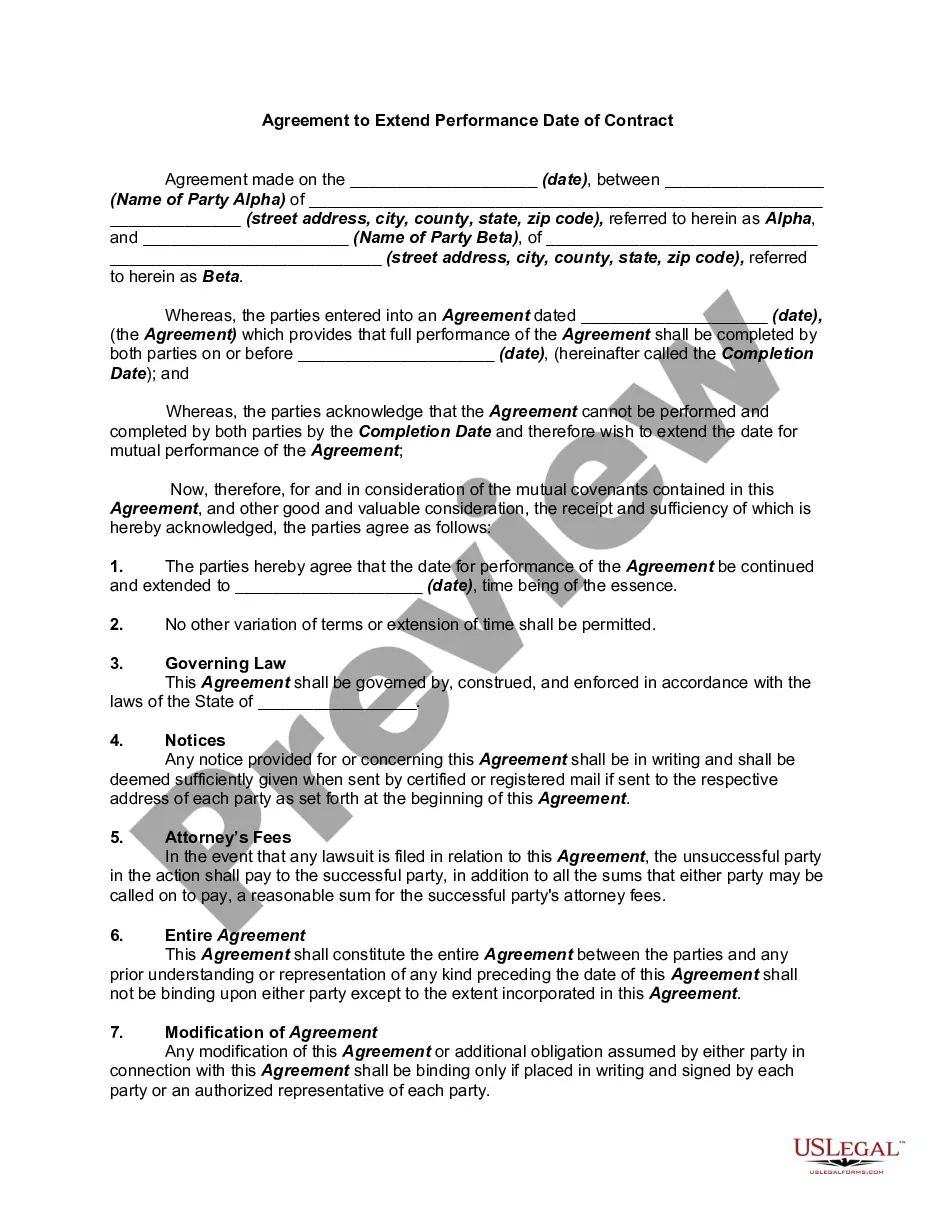

A contract extension agreement must contain:Names, addresses, and signatures of the contracting parties.Name, start date, and end date of the original contract.End date of the extension period.Changes to the contract including addition, removal, and deletion of the terms agreed upon in the original contract.

An extension addendum to contract is made when the parties agree to alter the terms or language of the original or existing agreement. An extension addendum to a contract may be made to change the original purchase price or to change the closing date of a real estate purchase.

How to Write1 Download The Paperwork Required To Postpone A Closing Date. The image on this page will deliver a quick preview of this addendum.2 Introduce This Paperwork With Basic Facts.3 Name The Desired Date.4 All The Signature Parties From The Original Contract Must Sign This Addendum.

How to Write1 Download The Paperwork Required To Postpone A Closing Date. The image on this page will deliver a quick preview of this addendum.2 Introduce This Paperwork With Basic Facts.3 Name The Desired Date.4 All The Signature Parties From The Original Contract Must Sign This Addendum.