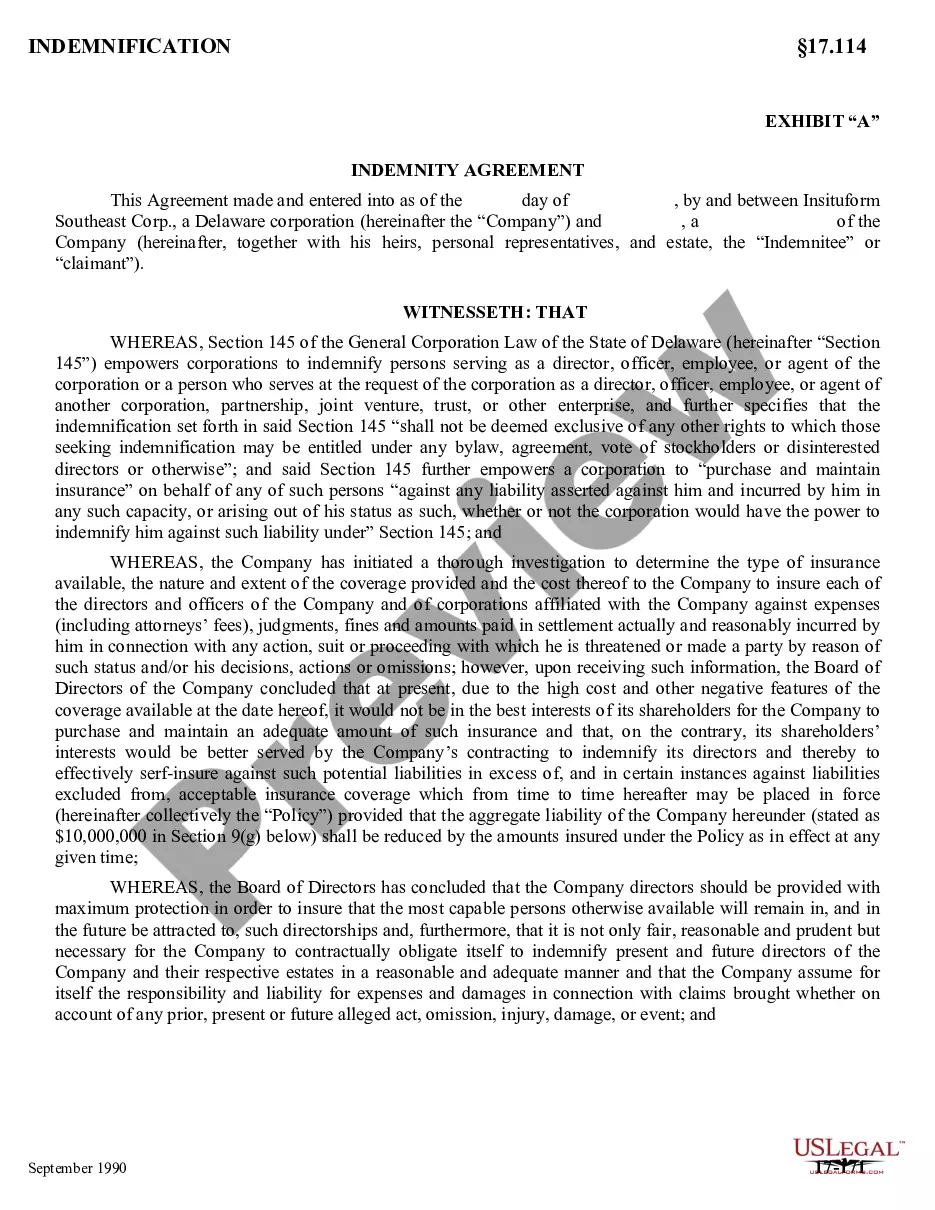

17-102E 17-102E . . . Indemnification Agreements between corporation and its directors and non-director officers at level of Vice President and above. The proposal states that Board anticipates that, if these Indemnification Agreements are ratified and approved, corporation may enter into similar Indemnification Agreements with new directors and non-director officers at same levels without seeking stockholder approval or ratification and that stockholder who votes in favor of ratification and approval sought herein may be estopped from making a claim that such future agreements are invalid

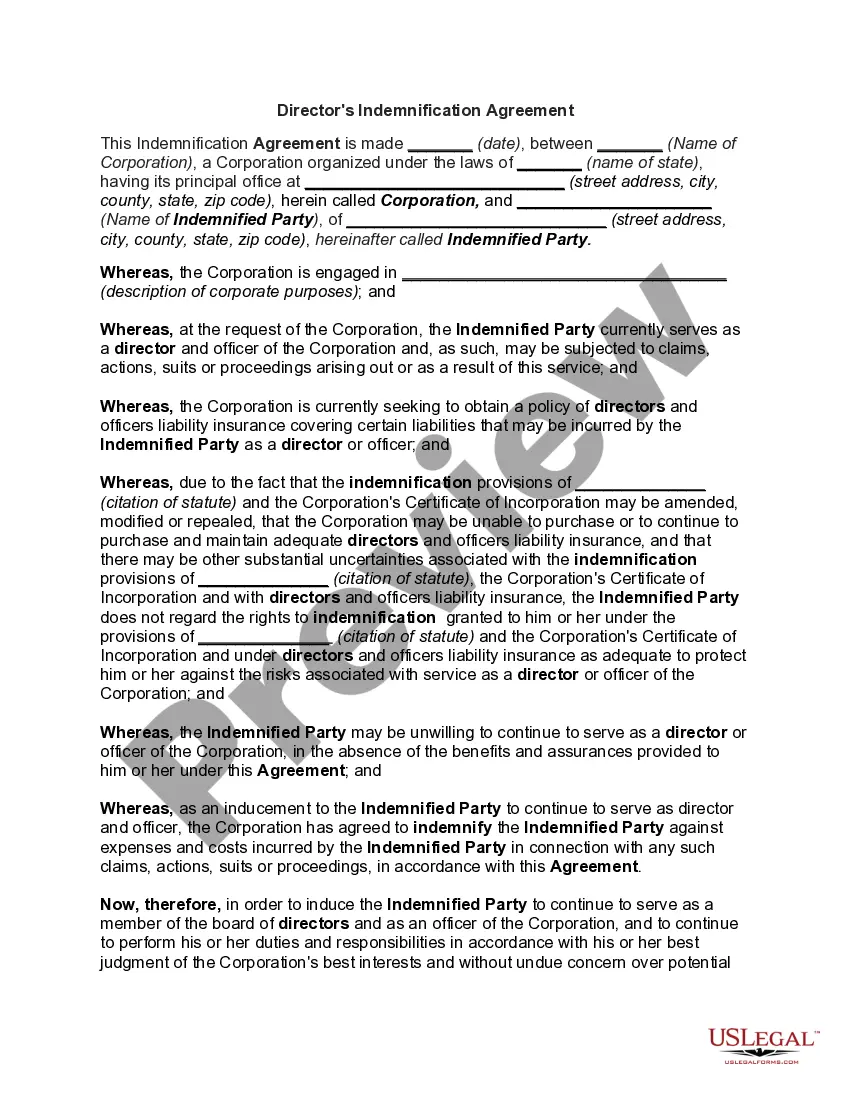

Virgin Islands Indemnification Agreement between Corporation and Its Directors and Non-Director Officers at Vice President Level and Above

Category:

State:

Multi-State

Control #:

US-CC-17-102E

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Indemnification Agreement Between Corporation And Its Directors And Non-Director Officers At Vice President Level And Above?

You can devote hours on-line trying to find the legal papers template that suits the federal and state requirements you will need. US Legal Forms offers a large number of legal types that are evaluated by specialists. You can easily obtain or print out the Virgin Islands Indemnification Agreement between Corporation and Its Directors and Non-Director Officers at Vice President Level and Above from my service.

If you already possess a US Legal Forms bank account, you can log in and click the Obtain key. After that, you can full, edit, print out, or signal the Virgin Islands Indemnification Agreement between Corporation and Its Directors and Non-Director Officers at Vice President Level and Above. Each legal papers template you purchase is your own property forever. To have yet another backup of the obtained type, check out the My Forms tab and click the corresponding key.

If you are using the US Legal Forms web site the very first time, follow the simple instructions below:

- Initially, make sure that you have selected the best papers template for the area/metropolis of your choice. Read the type outline to ensure you have picked the correct type. If accessible, use the Review key to look with the papers template too.

- If you wish to discover yet another version from the type, use the Search industry to find the template that suits you and requirements.

- After you have discovered the template you would like, just click Purchase now to proceed.

- Find the pricing strategy you would like, enter your qualifications, and sign up for your account on US Legal Forms.

- Complete the deal. You can utilize your bank card or PayPal bank account to pay for the legal type.

- Find the file format from the papers and obtain it to your gadget.

- Make modifications to your papers if required. You can full, edit and signal and print out Virgin Islands Indemnification Agreement between Corporation and Its Directors and Non-Director Officers at Vice President Level and Above.

Obtain and print out a large number of papers web templates while using US Legal Forms site, that offers the largest variety of legal types. Use skilled and state-distinct web templates to tackle your small business or personal requirements.

Form popularity

FAQ

Indemnity insurance is one way to be protected against claims or lawsuits. This insurance protects the holder from paying the full amount of a settlement, even if it is his fault. Many businesses require indemnity for their directors and executives because lawsuits are common.

Section 145(b) empowers a corporation to indemnify its directors against expenses incurred in connection with the defense or settlement of an action brought by or in the right of the corporation, subject to the standard of conduct determination, and except that no indemnification may be made as to any claim to which ...

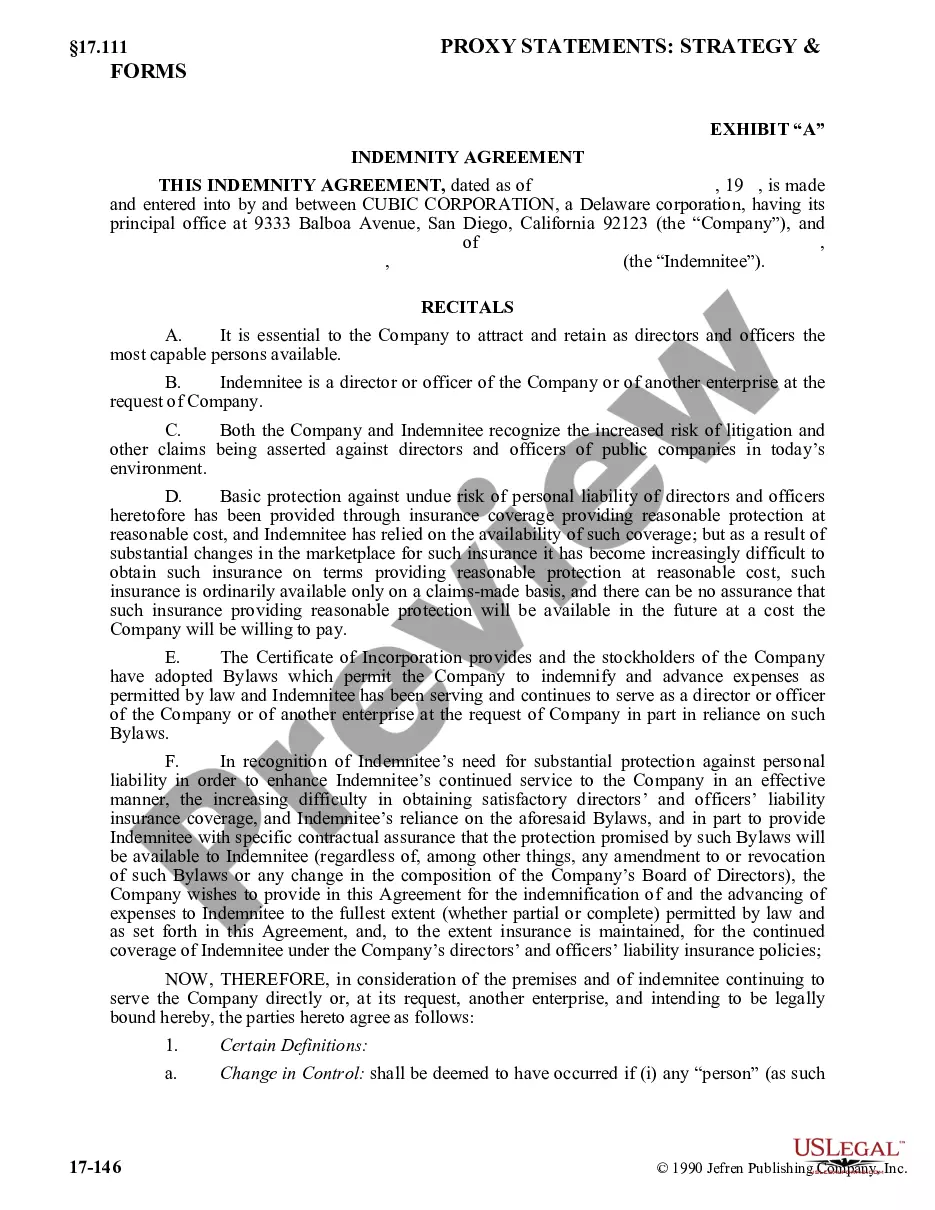

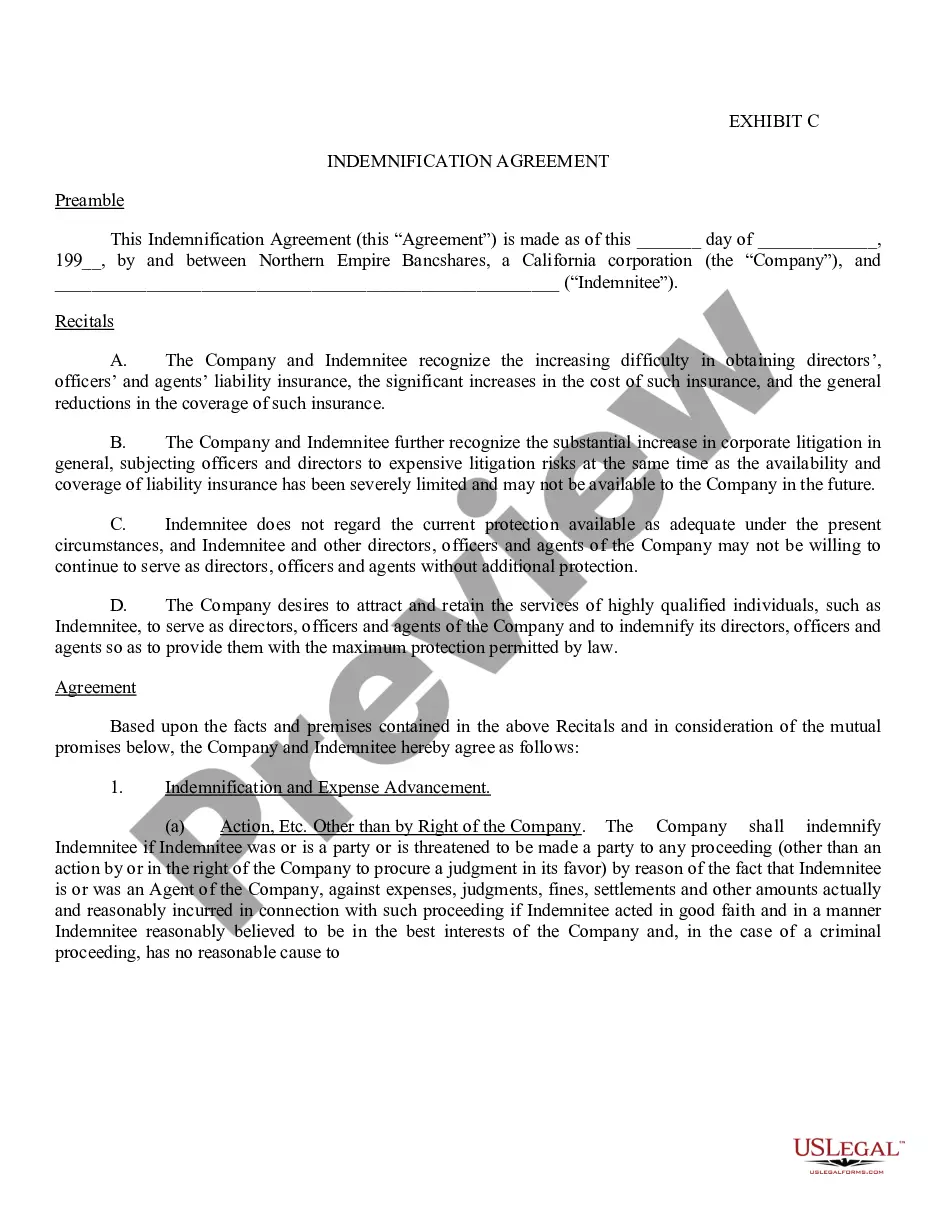

In the indemnification agreement, the corporation agrees to reimburse the director or officer for losses incurred in legal proceedings related to their service as a corporate director or officer to the maximum extent permitted by law.

Indemnification clauses are contractual provisions that require one party (the ?Indemnitor?) to indemnify another party (the ?Indemnitee?) for losses that the Indemnitee may suffer. In prime contracts, the owner usually is the Indemnitee and the contractor is the Indemnitor.

Indemnification, also referred to as indemnity, is an undertaking by one party (the indemnifying party) to compensate the other party (the indemnified party) for certain costs and expenses, typically stemming from third-party claims.

Typically, an insurance contract dictates that the insurer, also known as the indemnitor, agrees to compensate the other party involved (the insured or the indemnitee) for any damage or losses in return for premiums paid by the insured. University of Wisconsin System. "Hold Harmless and Indemnity Agreements."

The indemnity clause is a risk-shifting provision that requires the contractor to defend, reimburse, and ?hold harmless? the owner and architect from claims and liability ?arising out of? the contractor's work.

Insurance ? The indemnification agreement typically will require that the company provide D&O liability insurance that protects the indemnitee to the same extent as the most favorably insured of the company's and its affiliates' current directors and officers.