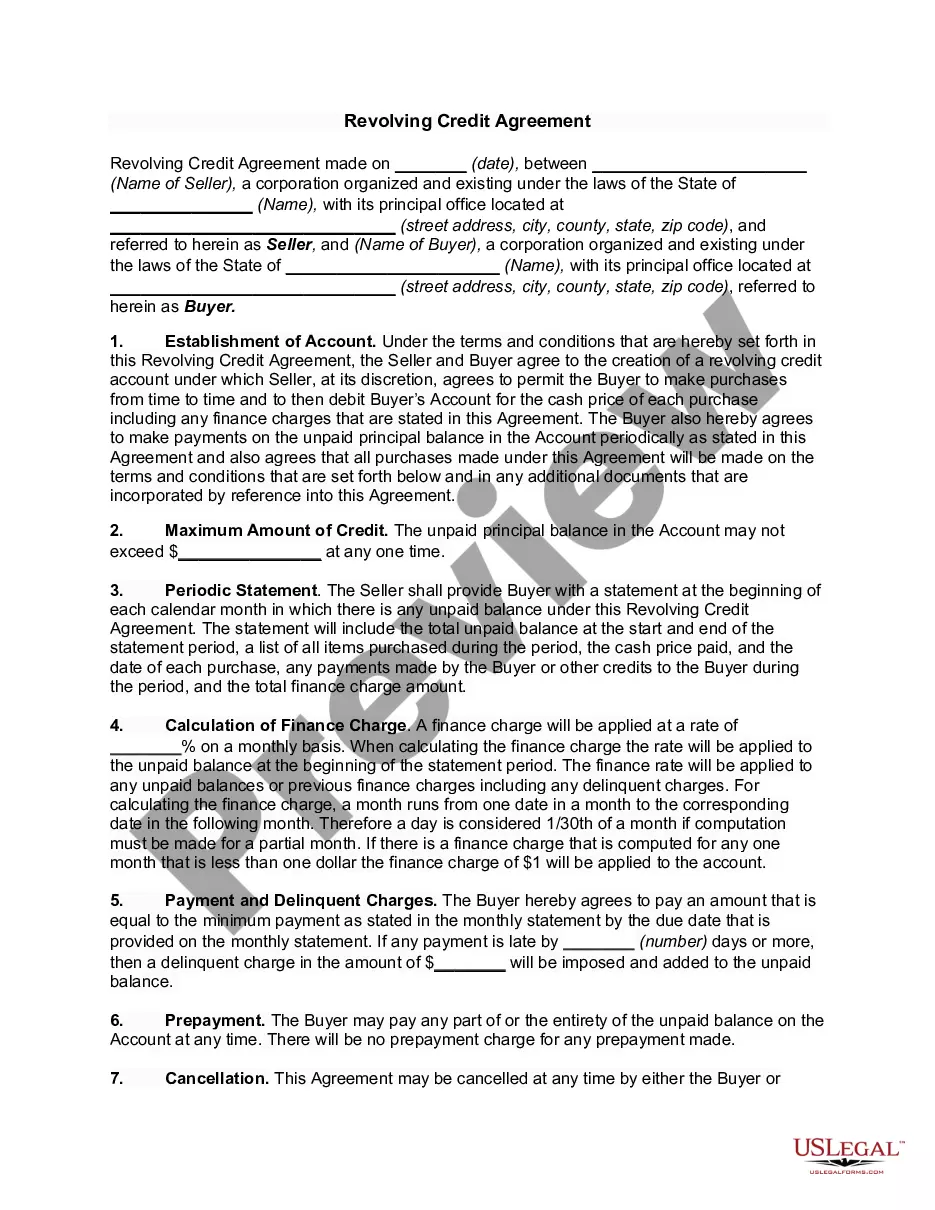

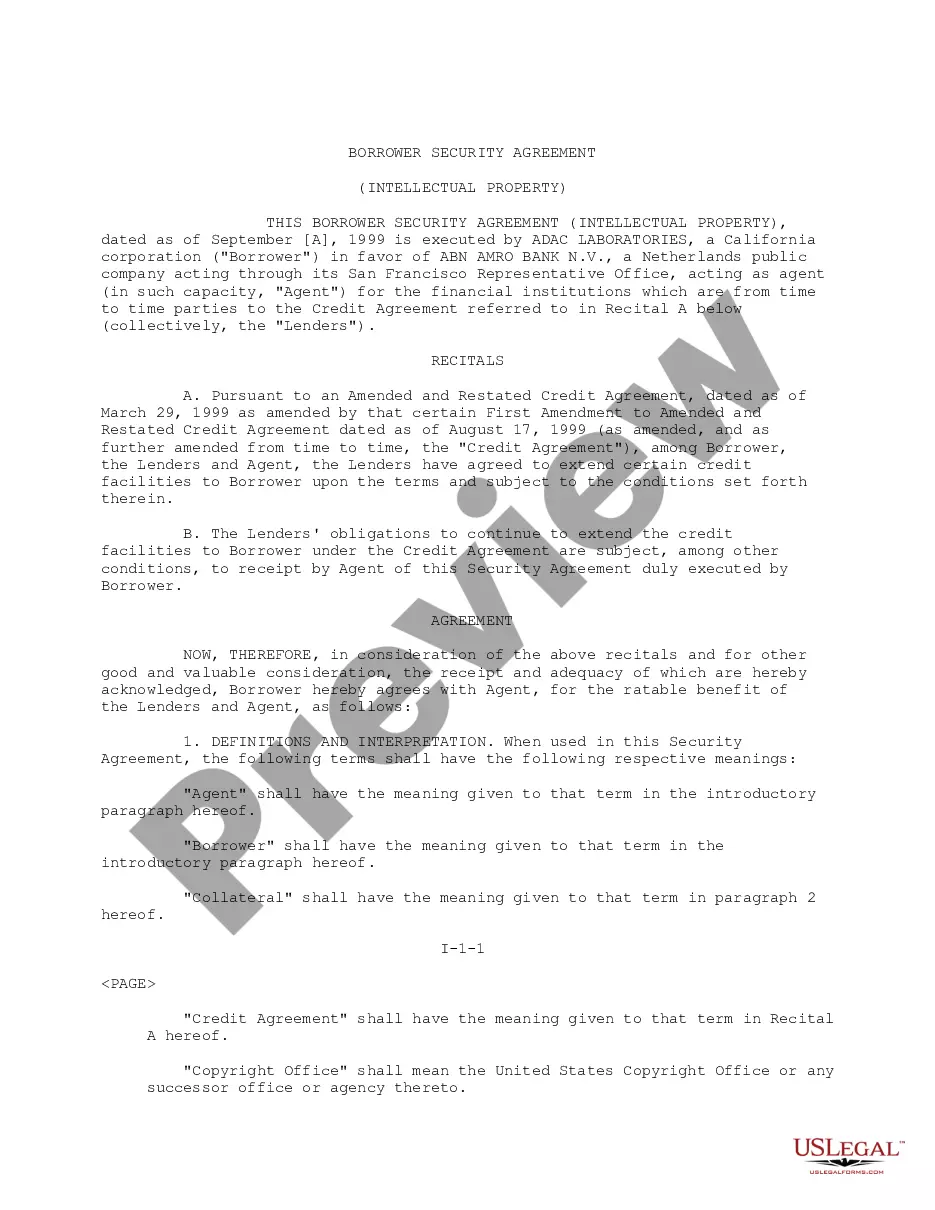

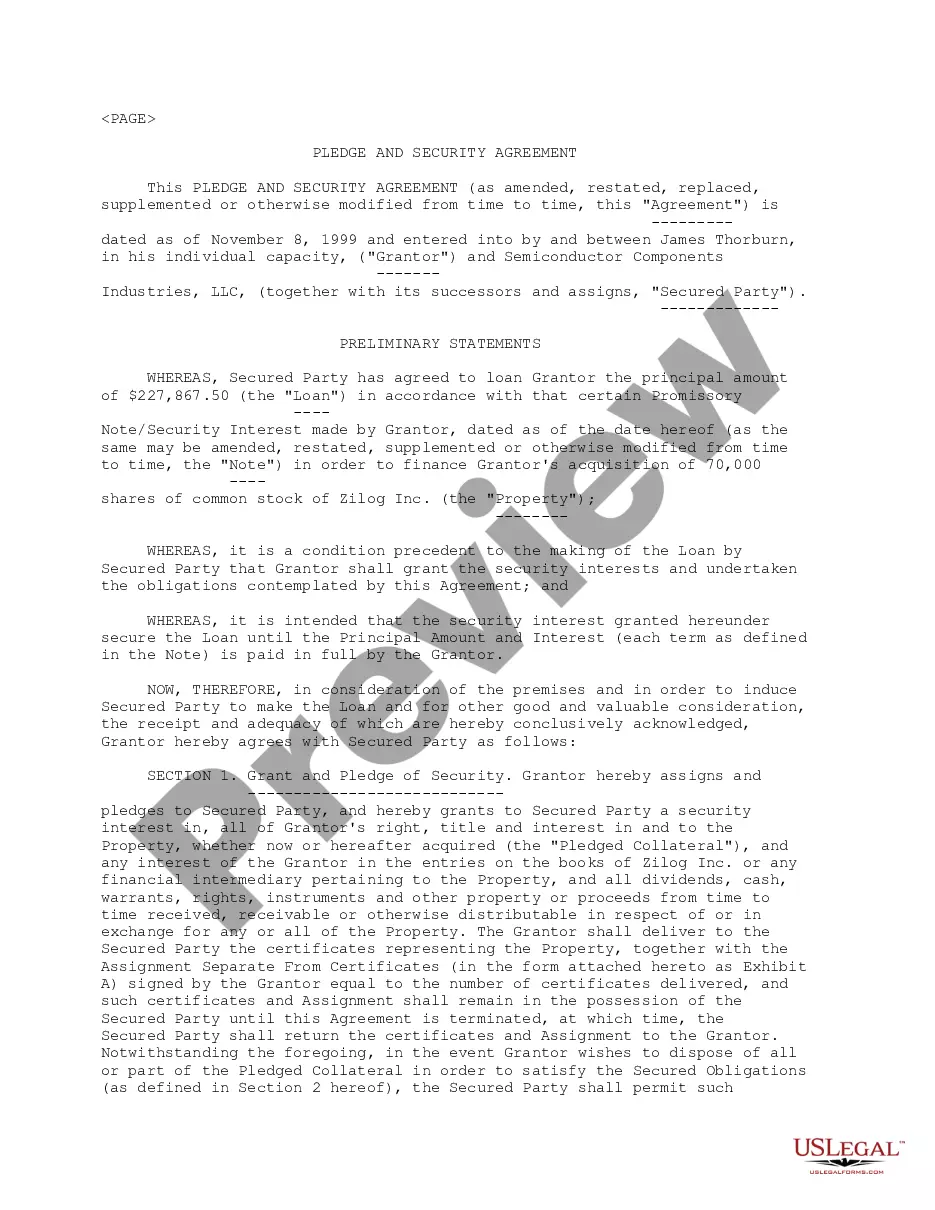

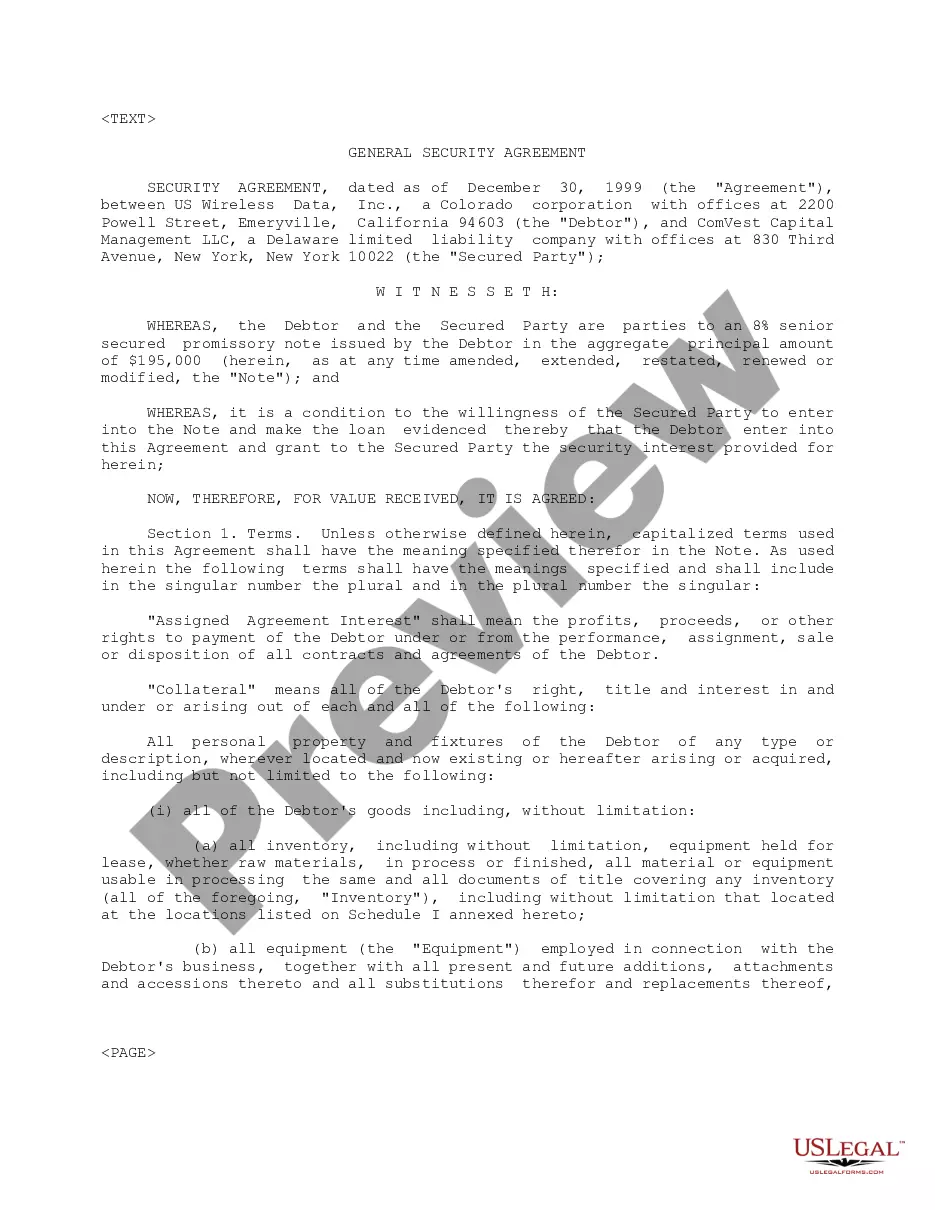

Virgin Islands Borrower Security Agreement regarding the extension of credit facilities

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Borrower Security Agreement Regarding The Extension Of Credit Facilities?

Are you within a place where you need to have paperwork for possibly enterprise or specific purposes almost every time? There are tons of legal papers templates available on the net, but getting versions you can rely on isn`t effortless. US Legal Forms delivers a huge number of type templates, much like the Virgin Islands Borrower Security Agreement regarding the extension of credit facilities, which are composed to meet state and federal demands.

Should you be presently acquainted with US Legal Forms internet site and have a free account, basically log in. Afterward, you can download the Virgin Islands Borrower Security Agreement regarding the extension of credit facilities web template.

If you do not offer an accounts and wish to start using US Legal Forms, abide by these steps:

- Get the type you will need and ensure it is to the right metropolis/region.

- Utilize the Review key to examine the form.

- Look at the outline to ensure that you have chosen the proper type.

- When the type isn`t what you`re trying to find, take advantage of the Search industry to discover the type that meets your needs and demands.

- If you obtain the right type, click Get now.

- Choose the costs program you would like, complete the required details to produce your account, and pay for the transaction utilizing your PayPal or credit card.

- Pick a hassle-free data file structure and download your version.

Get every one of the papers templates you possess bought in the My Forms food list. You can obtain a additional version of Virgin Islands Borrower Security Agreement regarding the extension of credit facilities whenever, if required. Just select the needed type to download or produce the papers web template.

Use US Legal Forms, probably the most extensive selection of legal kinds, to conserve time as well as stay away from errors. The assistance delivers professionally made legal papers templates which you can use for a range of purposes. Generate a free account on US Legal Forms and start creating your daily life a little easier.

Form popularity

FAQ

A secured line of credit is guaranteed by collateral, such as a home. An unsecured line of credit is not guaranteed by any asset; one example is a credit card. Unsecured credit always comes with higher interest rates because it is riskier for lenders.

Secured loans are business or personal loans that require some type of collateral as a condition of borrowing. A bank or lender can request collateral for large loans for which the money is being used to purchase a specific asset or in cases where your credit scores aren't sufficient to qualify for an unsecured loan. What Is a Secured Loan? How They Work, Types, and How to ... Investopedia ? ... ? Loans Investopedia ? ... ? Loans

Examples of secured credit cards Platinum Secured Credit Card. Regular APR. 30.74% (Variable) ... Chime Secured Credit Builder Visa® Credit Card. Regular APR. ... Merrick Bank Secured VisaR. Regular APR. ... PetalR 1 No Annual Fee VisaR Credit Card. Regular APR. ... QuicksilverOne Cash Rewards Credit Card. Regular APR. Secured vs. Unsecured Credit Cards? What Is The Difference? - Time time.com ? personal-finance ? article ? secured-vs... time.com ? personal-finance ? article ? secured-vs...

Key Takeaways A security agreement is a document that provides a lender a security interest in a specified asset or property that is pledged as collateral. Security agreements often contain covenants that outline provisions for the advancement of funds, a repayment schedule, or insurance requirements.

A creditor is an individual or institution that extends credit to another party to borrow money usually by a loan agreement or contract.

A credit facility agreement refers to an agreement or letter in which a lender, usually a bank or other financial institution, sets out the terms and conditions under which it is prepared to make a loan facility available to a borrower. It is sometimes called a loan facility agreement or a facility letter.

Whether you're trying to improve your credit scores or start building a credit history, a secured credit card can be a great option. Because they are backed by a cash deposit, secured credit cards usually have more lenient approval requirements, making them more accessible to some borrowers than unsecured cards. What Is a Secured Credit Card & Does It Build Credit? - Equifax equifax.com ? credit-cards ? articles ? learn equifax.com ? credit-cards ? articles ? learn

Your credit will benefit from a secured loan if you make on-time payments. Payment history accounts for 35% of your FICO® Score? , making it the most significant single factor that impacts your creditworthiness. Positive payment history will remain on your credit report for 10 years after you pay off the loan. Should I Get a Secured Loan to Build My Credit? - Experian experian.com ? blogs ? should-i-get-a-secur... experian.com ? blogs ? should-i-get-a-secur...