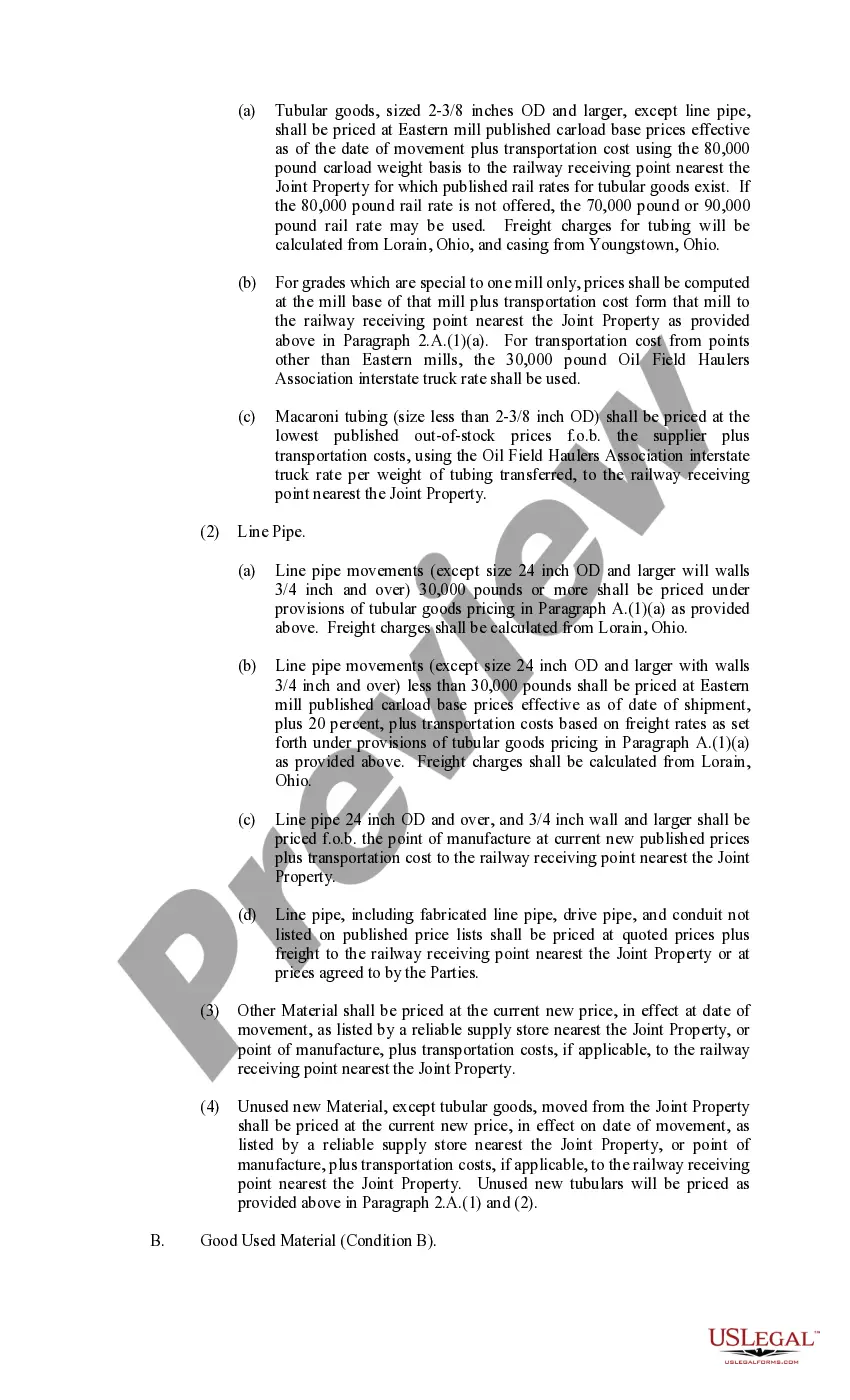

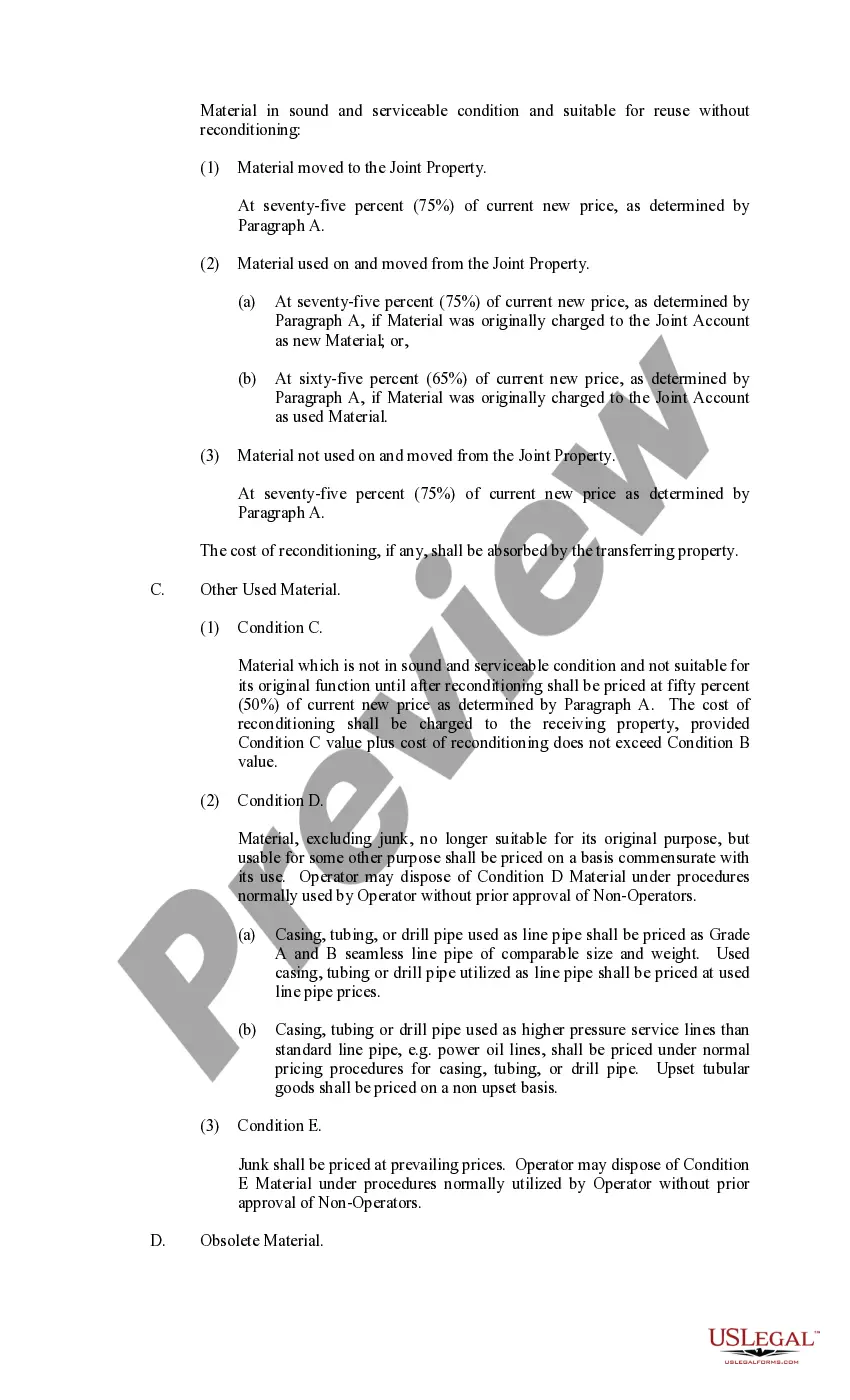

The Virgin Islands Exhibit C Accounting Procedure Joint Operations is a comprehensive set of guidelines and procedures used in accounting for joint operations in the Virgin Islands. These accounting procedures are designed to ensure accuracy, transparency, and compliance with local regulations for businesses operating in joint ventures or partnerships. One type of the Virgin Islands Exhibit C Accounting Procedure Joint Operations is specifically tailored for oil and gas exploration and production activities. This accounting procedure involves detailed documentation and reporting of revenue, expenses, and capital expenditures related to oil and gas operations. It includes provisions for cost recovery, sharing of production costs, and allocation of revenues among joint venture partners. Another type of the Virgin Islands Exhibit C Accounting Procedure Joint Operations caters to the tourism and hospitality industry. This accounting procedure focuses on accounting for joint operations involving hotels, resorts, and tour operators. It covers aspects such as revenue recognition, cost of goods sold, and allocation of expenses, ensuring accurate financial reporting for joint ventures in the sector. Furthermore, there is a subsection of the Virgin Islands Exhibit C Accounting Procedure Joint Operations designed for construction projects. This particular accounting procedure outlines specific guidelines for joint operations related to construction contracts, including cost tracking, progress billing, and revenue recognition based on completion milestones or percentage of completion. In all types of the Virgin Islands Exhibit C Accounting Procedure Joint Operations, key keywords and concepts that are important to understand include revenue recognition, expense allocation, cost sharing, joint venture agreements, local regulations' compliance, financial reporting, capital expenditures, cost recovery, and profit/loss distributions. These accounting procedures are essential for businesses engaged in joint operations in the Virgin Islands as they provide a standardized framework for accurate and transparent accounting practices, ensuring the financial success and accountability of joint ventures in various industries.

The Virgin Islands Exhibit C Accounting Procedure Joint Operations is a comprehensive set of guidelines and procedures used in accounting for joint operations in the Virgin Islands. These accounting procedures are designed to ensure accuracy, transparency, and compliance with local regulations for businesses operating in joint ventures or partnerships. One type of the Virgin Islands Exhibit C Accounting Procedure Joint Operations is specifically tailored for oil and gas exploration and production activities. This accounting procedure involves detailed documentation and reporting of revenue, expenses, and capital expenditures related to oil and gas operations. It includes provisions for cost recovery, sharing of production costs, and allocation of revenues among joint venture partners. Another type of the Virgin Islands Exhibit C Accounting Procedure Joint Operations caters to the tourism and hospitality industry. This accounting procedure focuses on accounting for joint operations involving hotels, resorts, and tour operators. It covers aspects such as revenue recognition, cost of goods sold, and allocation of expenses, ensuring accurate financial reporting for joint ventures in the sector. Furthermore, there is a subsection of the Virgin Islands Exhibit C Accounting Procedure Joint Operations designed for construction projects. This particular accounting procedure outlines specific guidelines for joint operations related to construction contracts, including cost tracking, progress billing, and revenue recognition based on completion milestones or percentage of completion. In all types of the Virgin Islands Exhibit C Accounting Procedure Joint Operations, key keywords and concepts that are important to understand include revenue recognition, expense allocation, cost sharing, joint venture agreements, local regulations' compliance, financial reporting, capital expenditures, cost recovery, and profit/loss distributions. These accounting procedures are essential for businesses engaged in joint operations in the Virgin Islands as they provide a standardized framework for accurate and transparent accounting practices, ensuring the financial success and accountability of joint ventures in various industries.