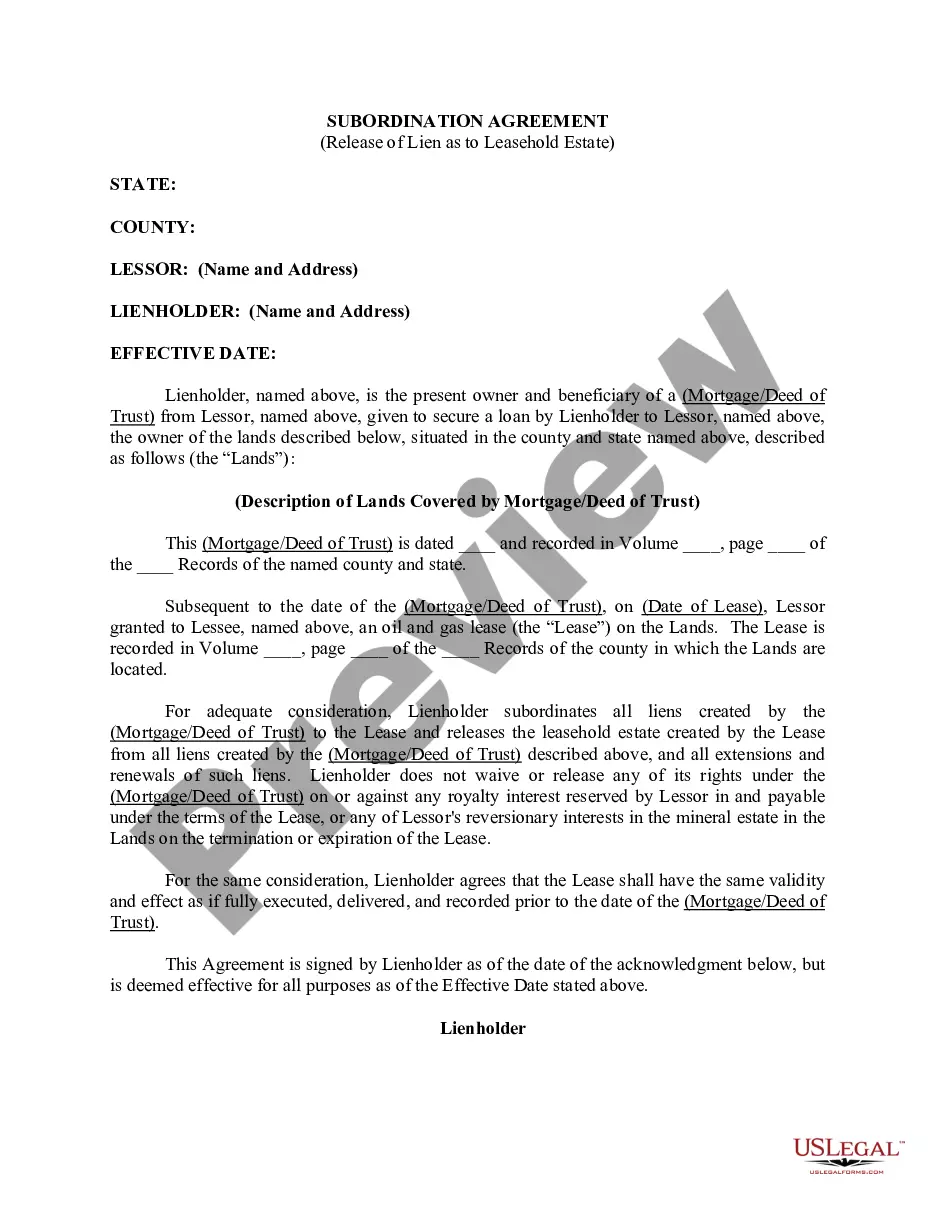

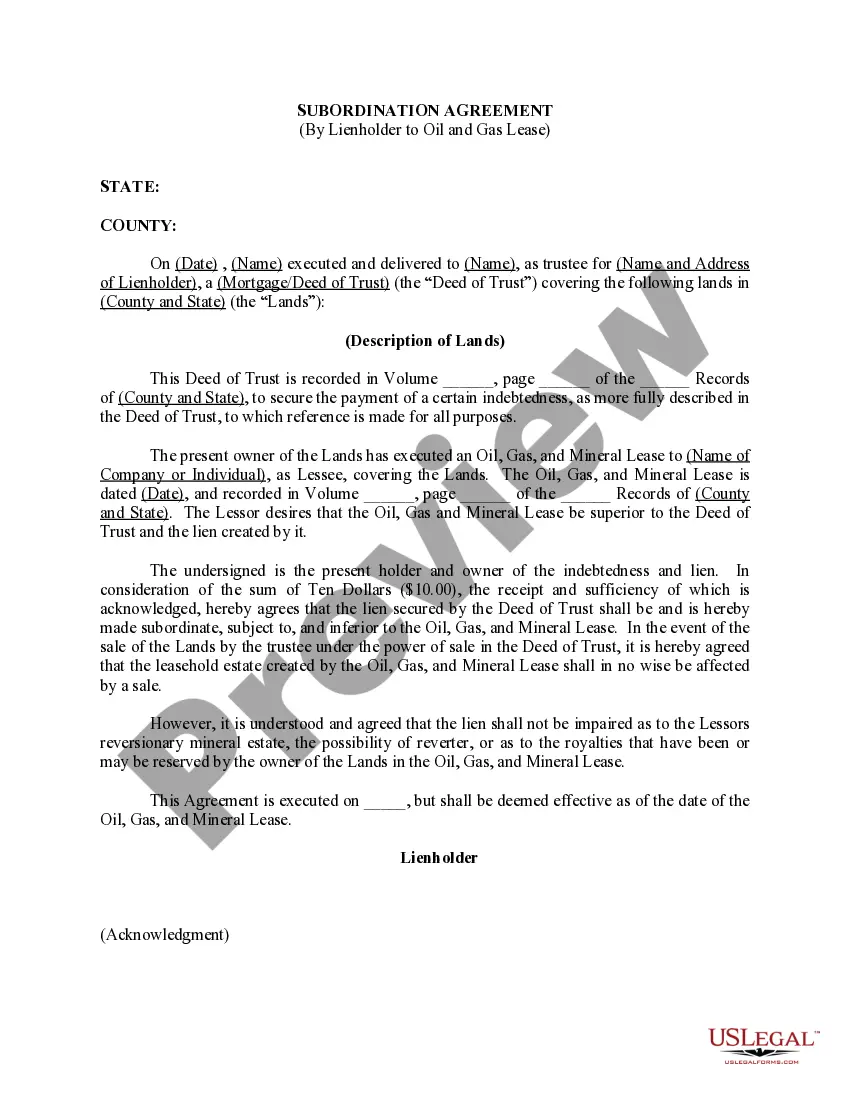

Virgin Islands Subordination Agreement with no Reservation by Lienholder

Description

How to fill out Subordination Agreement With No Reservation By Lienholder?

US Legal Forms - one of several biggest libraries of lawful varieties in the United States - gives a wide array of lawful document templates you can download or produce. While using website, you can get 1000s of varieties for organization and personal functions, categorized by categories, suggests, or key phrases.You will discover the most recent versions of varieties just like the Virgin Islands Subordination Agreement with no Reservation by Lienholder within minutes.

If you already possess a registration, log in and download Virgin Islands Subordination Agreement with no Reservation by Lienholder in the US Legal Forms library. The Download switch can look on each and every form you look at. You have accessibility to all previously acquired varieties from the My Forms tab of your own account.

If you wish to use US Legal Forms for the first time, listed below are straightforward guidelines to help you started:

- Make sure you have chosen the best form for your metropolis/region. Click the Review switch to examine the form`s information. Look at the form information to actually have selected the correct form.

- If the form does not match your specifications, use the Lookup industry at the top of the screen to find the the one that does.

- If you are happy with the shape, verify your selection by clicking on the Buy now switch. Then, select the pricing prepare you favor and give your qualifications to sign up to have an account.

- Approach the purchase. Utilize your Visa or Mastercard or PayPal account to perform the purchase.

- Pick the structure and download the shape in your system.

- Make changes. Fill up, change and produce and signal the acquired Virgin Islands Subordination Agreement with no Reservation by Lienholder.

Every template you added to your bank account does not have an expiration day and is also the one you have forever. So, if you would like download or produce yet another backup, just visit the My Forms segment and then click in the form you need.

Get access to the Virgin Islands Subordination Agreement with no Reservation by Lienholder with US Legal Forms, probably the most substantial library of lawful document templates. Use 1000s of expert and express-certain templates that meet your business or personal requires and specifications.

Form popularity

FAQ

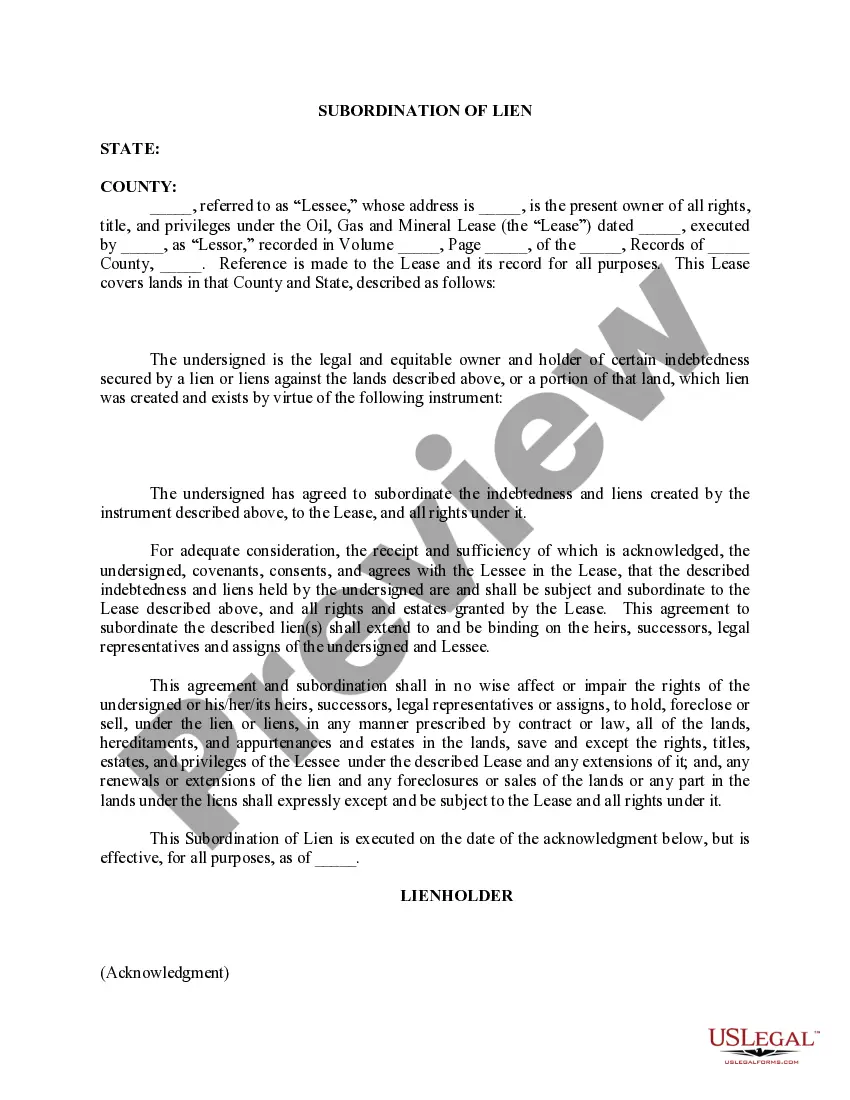

What Is A Subordinate Mortgage? Subordination in itself is the act of placing something in a lower-ranking position. Mortgage subordination boils down to a ranking system on the liens secured by your home. A lien is a legal agreement that grants the lender a right to repossess the property if you default on the loan.

Payment subordination establishes the hierarchy of interest and principal payments in case of default or liquidation. Senior debt is paid first, followed by junior debt. Lien subordination does not imply payment subordination. In the case of default, payments must continue to be made to all senior lenders equally.

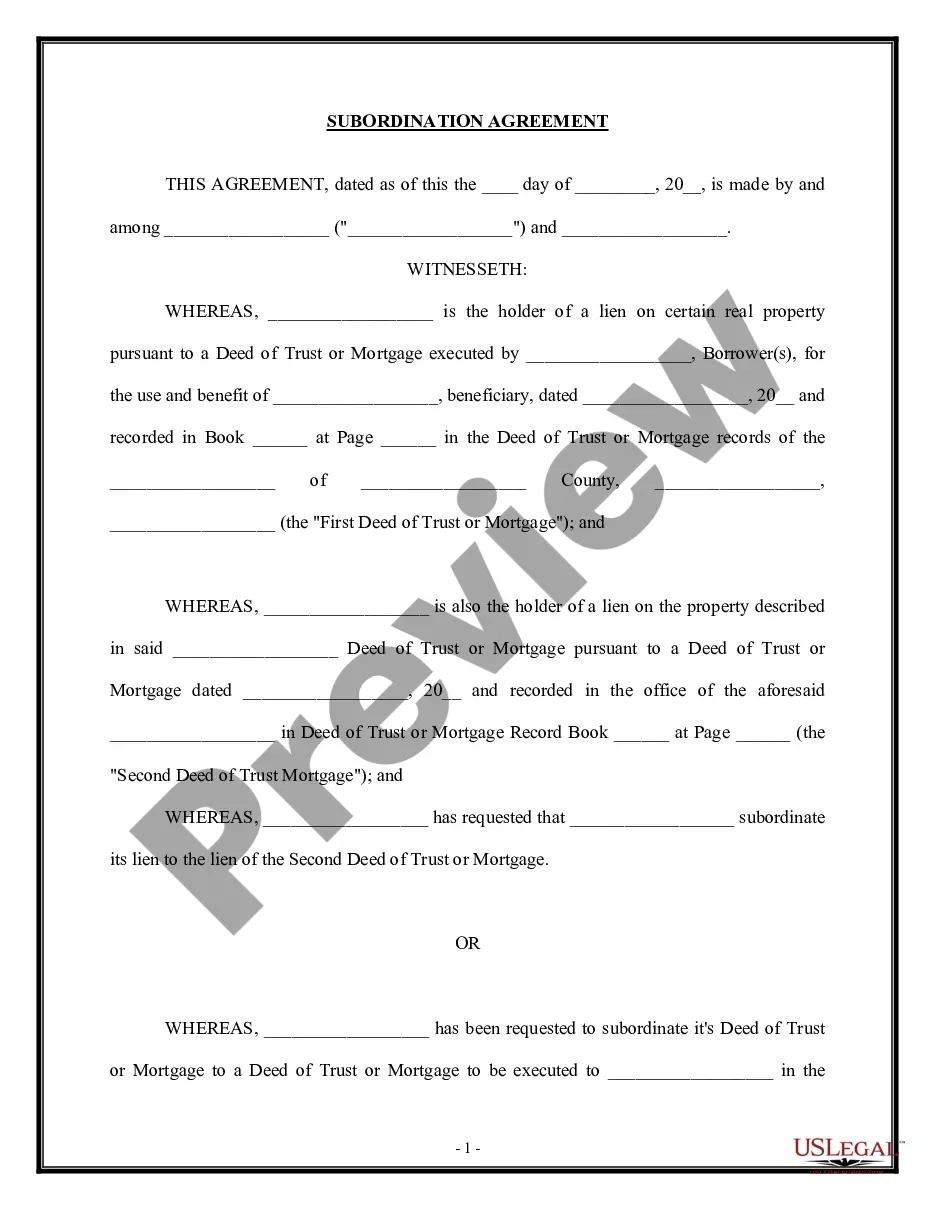

To adjust their priority, subordinate lienholders must sign subordination agreements, making their loans lower in priority than the new lender. A subordination agreement puts the new lender into first position and reassigns an existing mortgage to second position or third position, and so on.

Subordination agreements may be included in existing deeds of trust or may be outlined in an independent contract. In situations where two deeds of trust are being recorded concurrently, the lien priority is typically handled by instructing the title company as to which security instrument will be recorded first.

Two types of subordination agreements are: Executory Subordination and Automatic Subordination. These differ in the timing of when priority rights are given and the contractual performance required by the subordinated party.

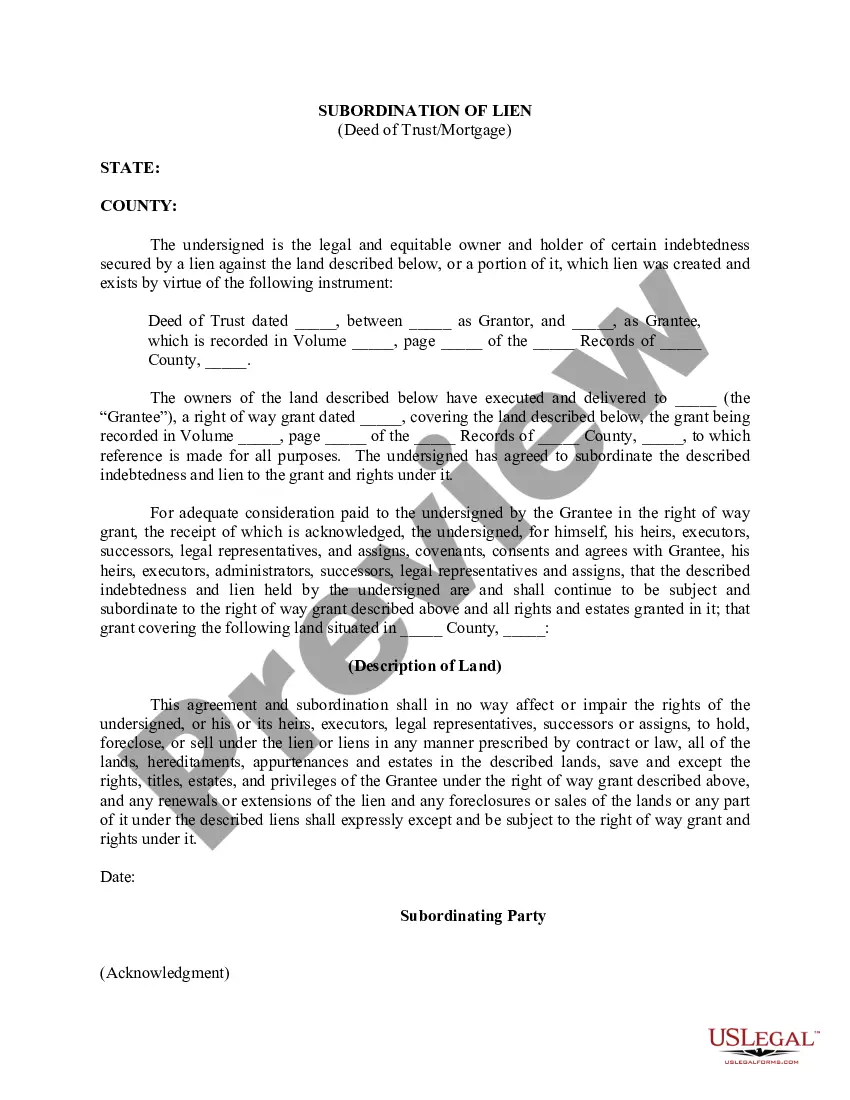

A Subordination Agreement is a legal document that establishes the priority of liens or claims against a specific asset.

A subordinate mortgage loan is any loan not in the first lien position. The subordination order goes by the order the loans were recorded. For example, your first mortgage (the mortgage used to buy the house) is recorded first because it's the first loan you borrow.

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.