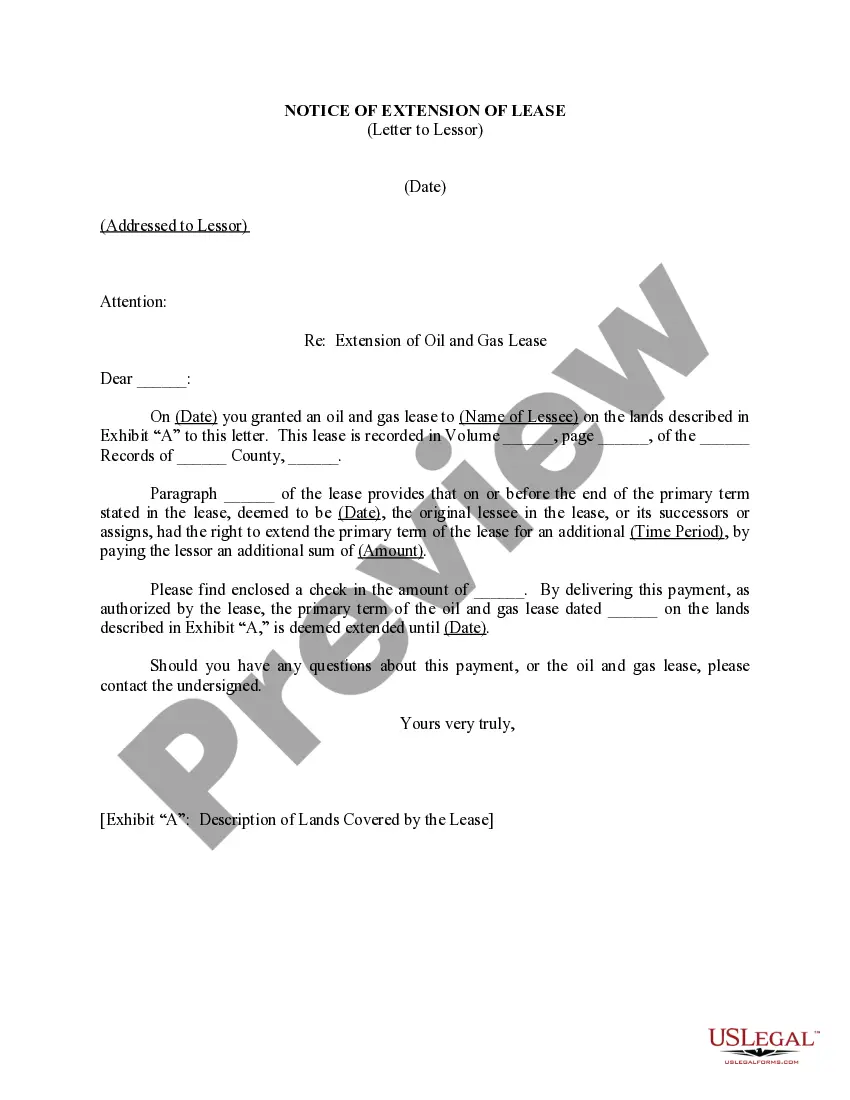

Virgin Islands Notice of Extension of Primary Term of Lease For Recording

Description

How to fill out Notice Of Extension Of Primary Term Of Lease For Recording?

If you wish to total, down load, or print legal file themes, use US Legal Forms, the greatest assortment of legal varieties, which can be found on-line. Take advantage of the site`s simple and practical look for to obtain the paperwork you want. A variety of themes for company and individual uses are categorized by groups and suggests, or key phrases. Use US Legal Forms to obtain the Virgin Islands Notice of Extension of Primary Term of Lease For Recording in a number of mouse clicks.

If you are already a US Legal Forms client, log in to the account and click on the Obtain key to obtain the Virgin Islands Notice of Extension of Primary Term of Lease For Recording. You can even accessibility varieties you in the past downloaded within the My Forms tab of your own account.

If you use US Legal Forms for the first time, refer to the instructions under:

- Step 1. Ensure you have chosen the shape for your right town/land.

- Step 2. Utilize the Review option to look over the form`s content material. Never forget about to see the information.

- Step 3. If you are not satisfied with all the type, use the Research field at the top of the display screen to find other types of the legal type template.

- Step 4. Once you have located the shape you want, click on the Purchase now key. Select the rates program you like and add your accreditations to sign up for the account.

- Step 5. Procedure the purchase. You can use your bank card or PayPal account to complete the purchase.

- Step 6. Find the format of the legal type and down load it on the gadget.

- Step 7. Comprehensive, change and print or signal the Virgin Islands Notice of Extension of Primary Term of Lease For Recording.

Every legal file template you acquire is the one you have forever. You might have acces to each and every type you downloaded with your acccount. Click on the My Forms area and pick a type to print or down load once more.

Compete and down load, and print the Virgin Islands Notice of Extension of Primary Term of Lease For Recording with US Legal Forms. There are many skilled and status-distinct varieties you can utilize for your company or individual requirements.

Form popularity

FAQ

ASC 842 is a lease accounting standard by the Financial Accounting Standards Board (FASB), requiring all leases longer than 12 months to be reflected on a company's balance sheet. This enhances financial transparency by giving a clear picture of an entity's lease obligations.

In these situations, to determine the lease term under FASB ASC 842, an entity must first determine if the lease is no longer enforceable if both the lessee and the lessor each have the right to terminate the lease without permission from the other party with no more than an insignificant Page 3 penalty.

Any difference between the carrying amounts of the right-of-use asset and the lease liability should be recorded in the income statement as a gain or loss; if a termination penalty is paid, that amount should be included in the gain or loss on termination.

For operating leases, ASC 842 requires recognition of a right-of-use asset and a corresponding lease liability upon lease commencement. With the changes introduced under ASC 842, all leases are now presented on both the balance sheet and income statement whether they are operating or finance (capital) leases.

Basically, these all-or-nothing practical expedients say that: You don't need to reassess the lease classification for any expired or existing leases. You don't need to reevaluate whether any existing or expired contracts contain leases.

Under ASC 842, both the lessor and lessee are required to separately account for the land component unless this would have an insignificant effect on the entity's accounting practice. The lessee would record a right-of-use asset and a lease liability in the balance sheet.

Lease modification: A change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease (for example, adding or terminating the right to use one or more underlying assets, or extending or shortening the contractual lease term).

Definition from ASC 842 Glossary Short-Term Lease: A lease that, at the commencement date, has a lease term of 12 months or less and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise.