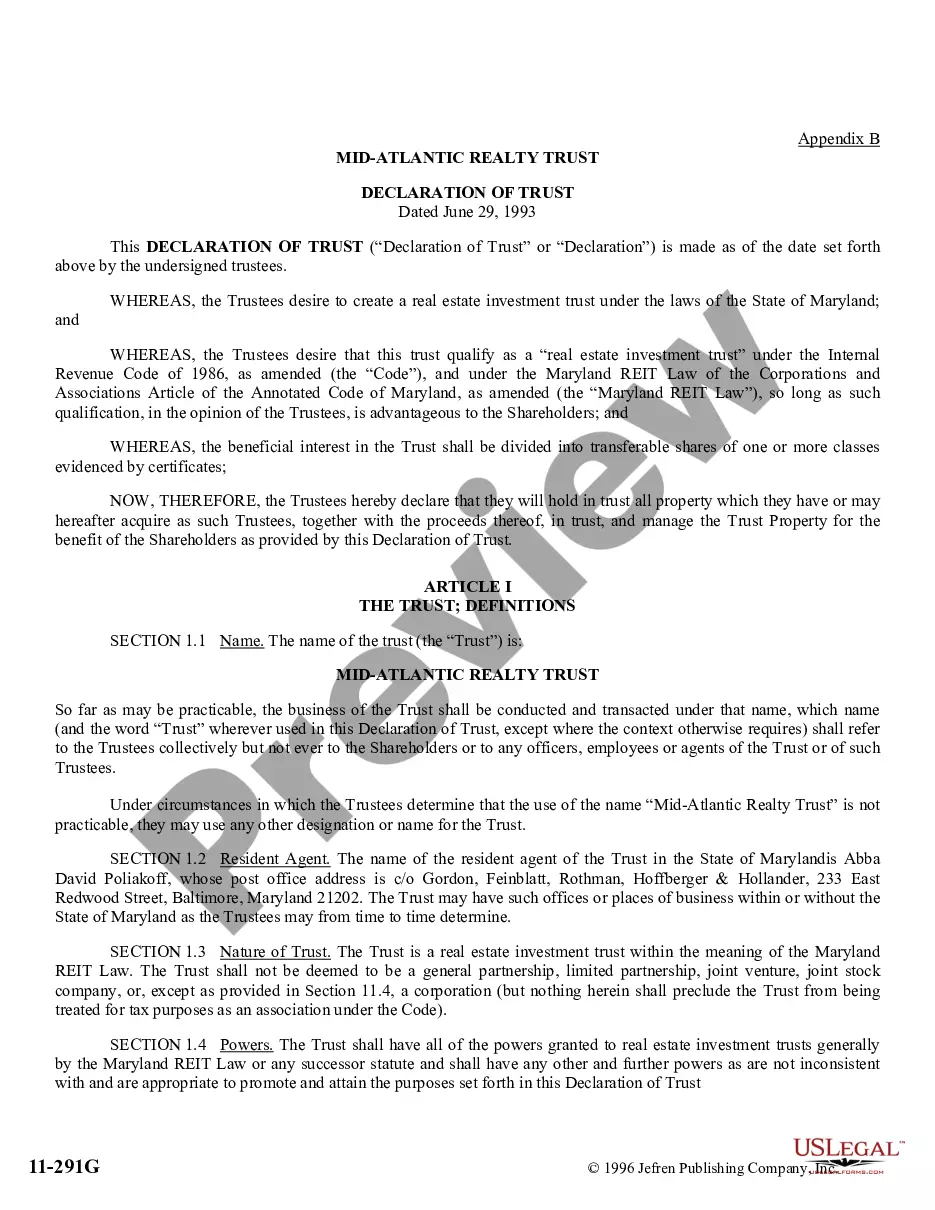

This document is a 53-page Declaration of Trust. It includes definitions of all relevant terms, as well as the constitution, capital accounts, valuations and prices, issue of units, register of unitholders, transmission, redemption of units, and every other necessary clause that constitutes a valid Declaration of Trust.

Virgin Islands Declaration of Trust

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Declaration Of Trust?

If you have to full, obtain, or produce authorized document web templates, use US Legal Forms, the most important collection of authorized forms, that can be found on the Internet. Take advantage of the site`s simple and handy lookup to discover the papers you need. Various web templates for business and individual uses are categorized by groups and suggests, or search phrases. Use US Legal Forms to discover the Virgin Islands Declaration of Trust in just a couple of mouse clicks.

When you are currently a US Legal Forms customer, log in for your accounts and then click the Obtain switch to get the Virgin Islands Declaration of Trust. Also you can gain access to forms you previously saved within the My Forms tab of the accounts.

Should you use US Legal Forms the first time, follow the instructions listed below:

- Step 1. Be sure you have selected the shape for your appropriate town/land.

- Step 2. Use the Preview method to look through the form`s articles. Do not neglect to see the explanation.

- Step 3. When you are not happy with the kind, utilize the Research industry near the top of the monitor to find other variations in the authorized kind web template.

- Step 4. Upon having discovered the shape you need, click on the Get now switch. Opt for the pricing prepare you prefer and include your references to register for the accounts.

- Step 5. Process the financial transaction. You should use your charge card or PayPal accounts to complete the financial transaction.

- Step 6. Pick the formatting in the authorized kind and obtain it on the gadget.

- Step 7. Total, change and produce or signal the Virgin Islands Declaration of Trust.

Every authorized document web template you purchase is the one you have eternally. You may have acces to every kind you saved inside your acccount. Select the My Forms area and choose a kind to produce or obtain once more.

Be competitive and obtain, and produce the Virgin Islands Declaration of Trust with US Legal Forms. There are many expert and state-certain forms you can utilize to your business or individual requirements.

Form popularity

FAQ

A declaration of trust, or nominee declaration, appoints a trustee to oversee assets for the benefit of another person or people. The declaration also describes the assets that are to be held in the trust and how they are to be managed.

It's a legal document, also referred to as a deed of trust, which records the financial arrangements between everyone who has a financial interest in the property. This could be necessary if you're buying as a joint owner or getting help from someone else, such as a parent.

Trusts are generally created by a private document to which the settlor, the trustees and any protector are the only parties. The trust instrument does not have to be filed with any public body in the BVI, and information relating to the trust is not accessible by the general public.

The most common example of when a declaration of trust is used is the situation where an adult son or daughter borrows money for a deposit on a first house from his or her parents. The parents may have a mortgage already, and the terms of that mortgage prevent them from borrowing under another.

Three certainties Certainty of intention: it must be clear that the testator intends to create a trust. Certainty of subject matter: it must be clear what property is part of the trust and property, including sum of money, cannot be separated. Certainty of objects: it must be clear who the beneficiaries (objects) are.

Local Requirements BVI trusts are subject to a US$200 Trust Duty payable on the execution of the trust deed. BVI trusts are exempt from all local registration requirements and all BVI taxes if the trust Beneficiaries are not residents of the BVI.