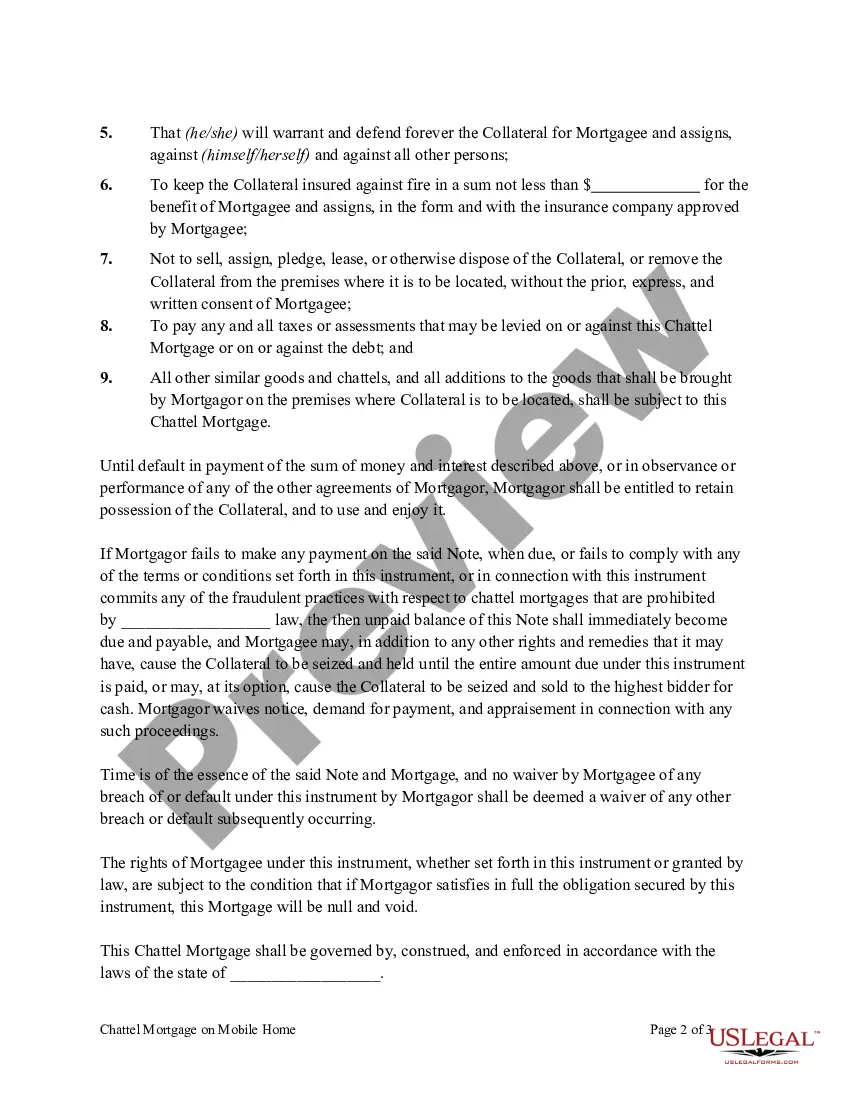

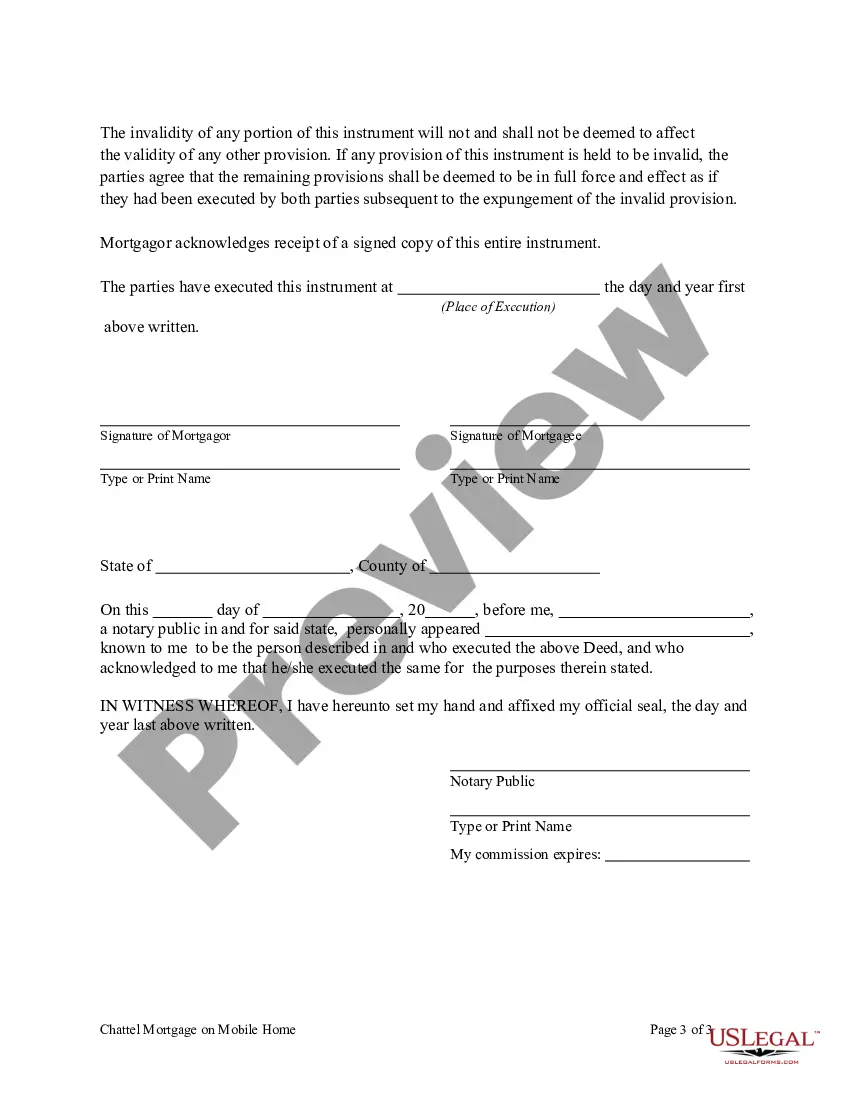

Vermont Chattel Mortgage on Mobile Home: A Detailed Description A Vermont Chattel Mortgage on a Mobile Home refers to a specialized financial agreement concerning the purchase or refinancing of a mobile home. It is a form of secured loan that allows individuals to secure funds for mobile home purchases while using the home itself as collateral. In Vermont, Chattel Mortgages are primarily designed for mobile homes placed on rented lots or private property where the homeowner does not own the land. Since mobile homes are considered personal property and not considered real estate, a Chattel Mortgage is used to establish a legal claim on the home. It ensures that in case of default, the lender has the right to seize and sell the mobile home to recover any outstanding debt. Key Features and Process: 1. Security Agreement: A Chattel Mortgage involves entering into a security agreement between the borrower (buyer) and the lender. The agreement outlines the terms and conditions of the loan, including repayment obligations, interest rates, and any fees associated with the mortgage. 2. Collateral: The mobile home itself serves as collateral for the loan. The borrower grants a security interest to the lender, giving them the right to repossess the home if the borrower fails to meet their payment obligations. 3. Title Search: Prior to finalizing the mortgage, a title search is typically conducted by the lender to ensure the mobile home has clear ownership and no existing liens or encumbrances. 4. Perfecting the Mortgage: To perfect the mortgage, a Uniform Commercial Code (UCC) Financing Statement is filed with the Vermont Secretary of State to establish the lender's secured interest in the mobile home. This filing protects the lender's interest in case of bankruptcy or competition with other creditors. Different Types of Vermont Chattel Mortgage on Mobile Home: 1. Purchase Chattel Mortgage: This type of mortgage is used when an individual intends to buy a mobile home and requires financing. The loan is secured against the mobile home from the moment of purchase. 2. Refinance Chattel Mortgage: This form of Chattel Mortgage allows individuals to refinance an existing loan on their mobile home. Borrowers can avail themselves of a lower interest rate or better loan terms, thereby reducing their monthly payments. 3. Second Lien Chattel Mortgage: In some cases, homeowners may need additional funds and wish to retain their primary mortgage. A second lien Chattel Mortgage is used in such scenarios, allowing individuals to borrow against the equity in their mobile home. Conclusion: A Vermont Chattel Mortgage on a Mobile Home is a financial tool that enables individuals to purchase or refinance their mobile homes using the home itself as collateral. By understanding the various types of Chattel Mortgages available, individuals can make informed decisions based on their specific needs, financial standing, and mobile homeownership circumstances.

Vermont Chattel Mortgage on Mobile Home

Description

How to fill out Vermont Chattel Mortgage On Mobile Home?

Are you in the placement where you need to have paperwork for both enterprise or individual reasons almost every day? There are plenty of legitimate record templates accessible on the Internet, but locating ones you can trust isn`t simple. US Legal Forms gives a huge number of develop templates, just like the Vermont Chattel Mortgage on Mobile Home, that happen to be composed to fulfill federal and state specifications.

When you are presently acquainted with US Legal Forms site and also have a free account, basically log in. Next, you can down load the Vermont Chattel Mortgage on Mobile Home web template.

Should you not have an bank account and want to start using US Legal Forms, follow these steps:

- Obtain the develop you want and ensure it is for that correct area/area.

- Make use of the Preview option to check the shape.

- Look at the explanation to actually have chosen the appropriate develop.

- If the develop isn`t what you`re seeking, take advantage of the Lookup field to obtain the develop that meets your requirements and specifications.

- If you get the correct develop, simply click Get now.

- Pick the costs plan you need, complete the necessary information and facts to generate your bank account, and buy the order utilizing your PayPal or credit card.

- Pick a handy document format and down load your duplicate.

Locate every one of the record templates you may have bought in the My Forms food list. You can aquire a additional duplicate of Vermont Chattel Mortgage on Mobile Home anytime, if needed. Just select the essential develop to down load or produce the record web template.

Use US Legal Forms, by far the most substantial collection of legitimate kinds, in order to save efforts and prevent errors. The services gives professionally made legitimate record templates which you can use for a selection of reasons. Create a free account on US Legal Forms and initiate making your life easier.

Form popularity

FAQ

A real estate license is required only if the transaction involves the sale or lease of real property. The sale of manufactured homes without land attached requires a license from the Arizona Department of Real Estate or the Arizona Department of Housing.

A chattel mortgage is a type of loan that is secured by a movable piece of property. In contrast, a traditional mortgage is typically secured by a fixed property.

Certificate of Title. Bill of Sale and Odometer Disclosure (form VT-005) Lien Release, if applicable (form VT-08)

Answer: While the sale of a manufactured home (no real estate) requires a separate license from the Texas Department of Housing and Community Affairs (TDHCA), under a TDHCA exemption a TREC license holder can sell one manufactured home during a 12-month period without a TDHCA license (see Tex. Occ. Code 1201.003(24)).

Vermont statute requires that this Mobile Home Uniform Bill of Sale be signed by each Buyer and Seller, endorsed by the Town Clerk of the Town where the Mobile Home is located at the time of sale, and filed by Buyer with the Town Clerk of the Town where the Mobile Home will be located after the sale.

The State of Vermont does not regulate the installation and set up of manufactured or mobile homes. However, it is still important to check with your town officials for any local requirements.