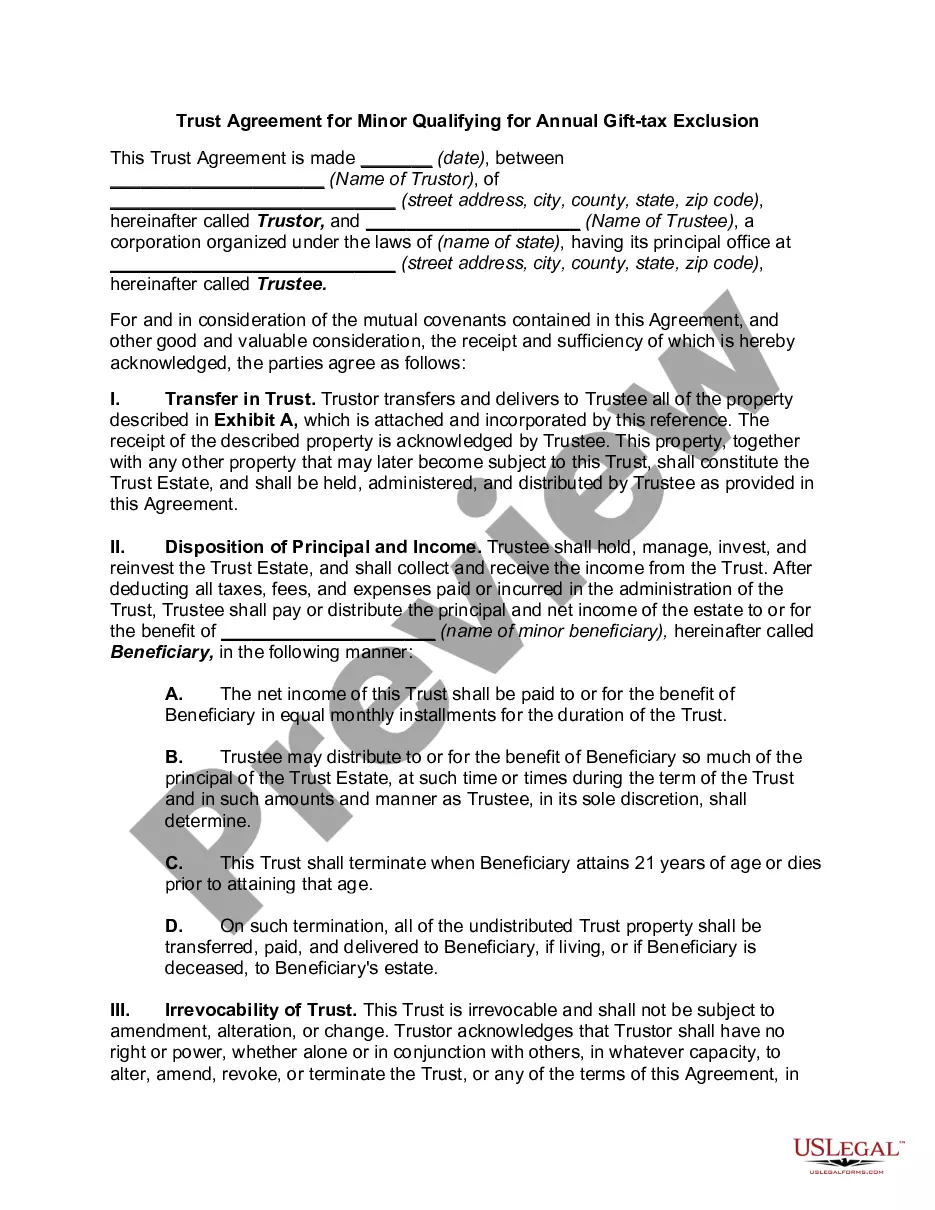

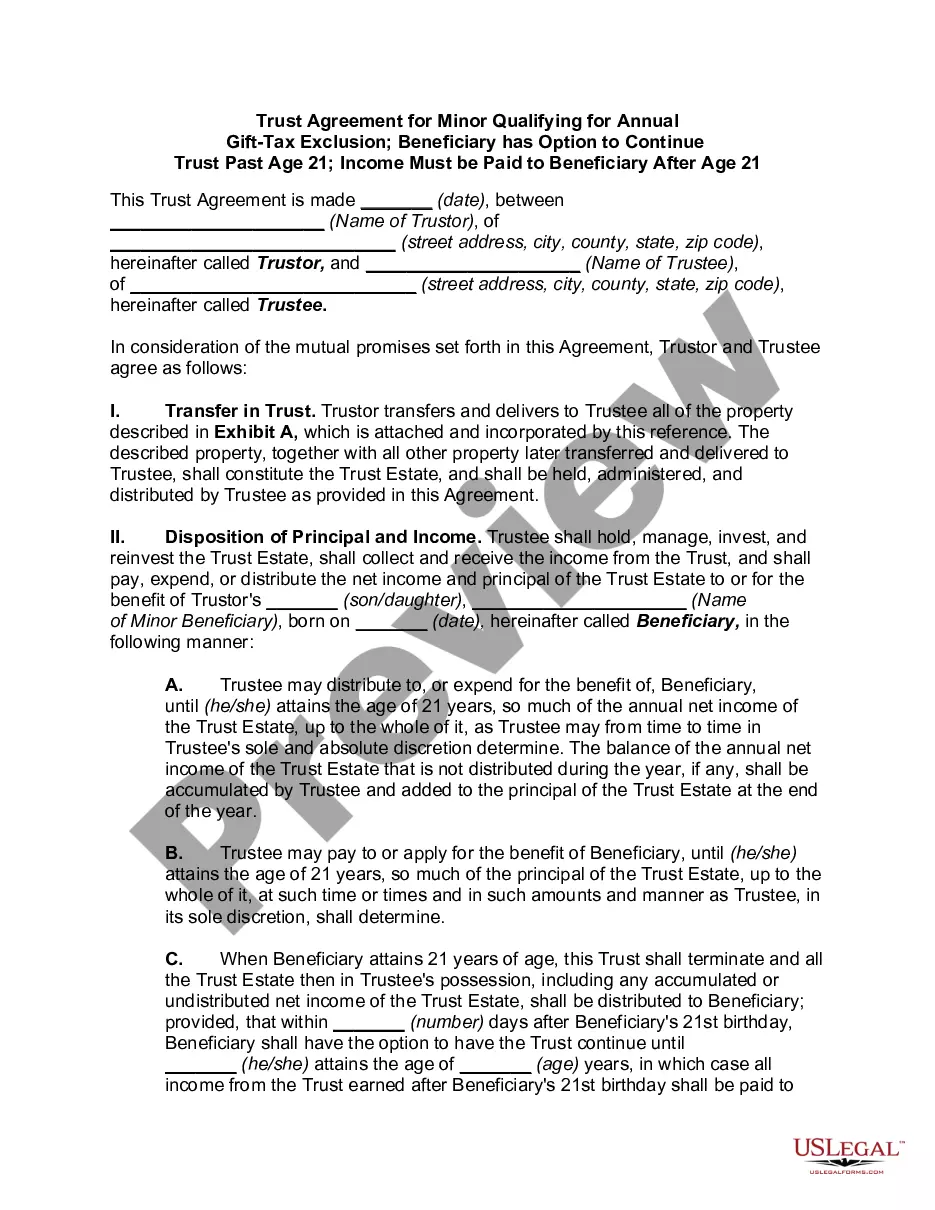

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children

Instant download

Description

Free preview

How to fill out Trust Agreement For Minors Qualifying For Annual Gift Tax Exclusion - Multiple Trusts For Children?

Identifying the correct genuine document format can be somewhat a challenge. Naturally, there are numerous formats available on the web, but how do you acquire the authentic type you need? Utilize the US Legal Forms platform. This service provides thousands of formats, such as the Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, which can be utilized for business and personal purposes. All templates are reviewed by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click on the Download button to obtain the Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. Use your account to search through the legal forms you have previously purchased. Navigate to the My documents section of your account and retrieve an additional copy of the document you need.

If you are a new user of US Legal Forms, here are straightforward steps you should follow: First, ensure you have selected the right form for your jurisdiction/state. You can review the form using the Preview button and examine the form outline to confirm it is suitable for you. If the form does not meet your requirements, employ the Search field to find the appropriate form. When you are confident that the form is accurate, click the Purchase now button to obtain the form.

- Choose the pricing plan you prefer and provide the necessary information.

- Create your account and complete the payment using your PayPal account or Visa or Mastercard.

- Select the document format and download the legal document to your device.

- Complete, modify, print, and sign the received Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children.

- US Legal Forms is the largest repository of legal forms where you can find various document formats.

- Take advantage of the service to download professionally crafted documents that adhere to state regulations.

Form popularity

FAQ

Vermont offers various trust types, including revocable trusts, irrevocable trusts, and special needs trusts, each serving distinct purposes. Revocable trusts allow flexibility as you can change terms during your lifetime, while irrevocable trusts provide asset protection. Understanding these options can help you choose the right structure, such as a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, to best meet your family's financial goals.

Creating a trust in Vermont typically involves drafting a trust document that outlines the terms and appoints a trustee. You can simplify this process by using UsLegalForms, which offers tailored templates for establishing a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. Once your trust document is complete, ensure to sign it and fund the trust with the desired assets.

A common mistake parents encounter when creating a trust fund is failing to review and fund the trust properly. Without transferring assets into the trust, it does not serve its intended purpose. It's essential to ensure that a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children is set up correctly and that all relevant assets are designated to the trust.

The simplest way to establish a trust is by using a reliable legal service like UsLegalForms. This platform provides templates that guide you through the process of creating a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. By following the provided instructions and customizing the template to your needs, you can efficiently set up a trust.

The child tax credit in Vermont provides financial aid to families raising children through tax deductions. This credit can reduce the overall tax burden, helping parents save more. When establishing a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, understanding available credits can enhance your financial strategy while providing for your children.

Yes, Vermont does grant automatic extensions for filing state income tax returns. Taxpayers can obtain a six-month extension by submitting the proper form, usually without needing to provide a reason. If you are planning to create a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, understanding this extension can provide necessary time to complete your estate planning.

The amount left from a $50,000 salary after taxes in Vermont depends on various factors, including your filing status and deductions. Generally, you can expect to retain approximately $37,500 to $40,000 after federal and state taxes. Consider the impact of a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children on your overall finances, as it can offer unique tax benefits.

The Vermont tax refund process requires the completion of the appropriate forms when filing your state tax returns, typically completed on Form 111. Your refund depends on various factors, including your income and applicable deductions. Setting up a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can influence your financial situation, so keep the tax implications in mind when seeking refunds.

Vermont Form 111 is the state income tax form used by individuals to report personal income. This form ensures taxpayers accurately declare their earnings and taxes owed or refunds expected. When establishing a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, it is crucial to understand your tax implications, as this form may come into play.

The main difference between UTMA and 2503c lies in the account's management and flexibility. UTMA accounts offer broader investment options and allow minors to gain access to funds at age 21, while a 2503c trust limits distribution until the child turns 21. If you are considering a Vermont Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, understanding these distinctions will help in selecting the right option for your family.