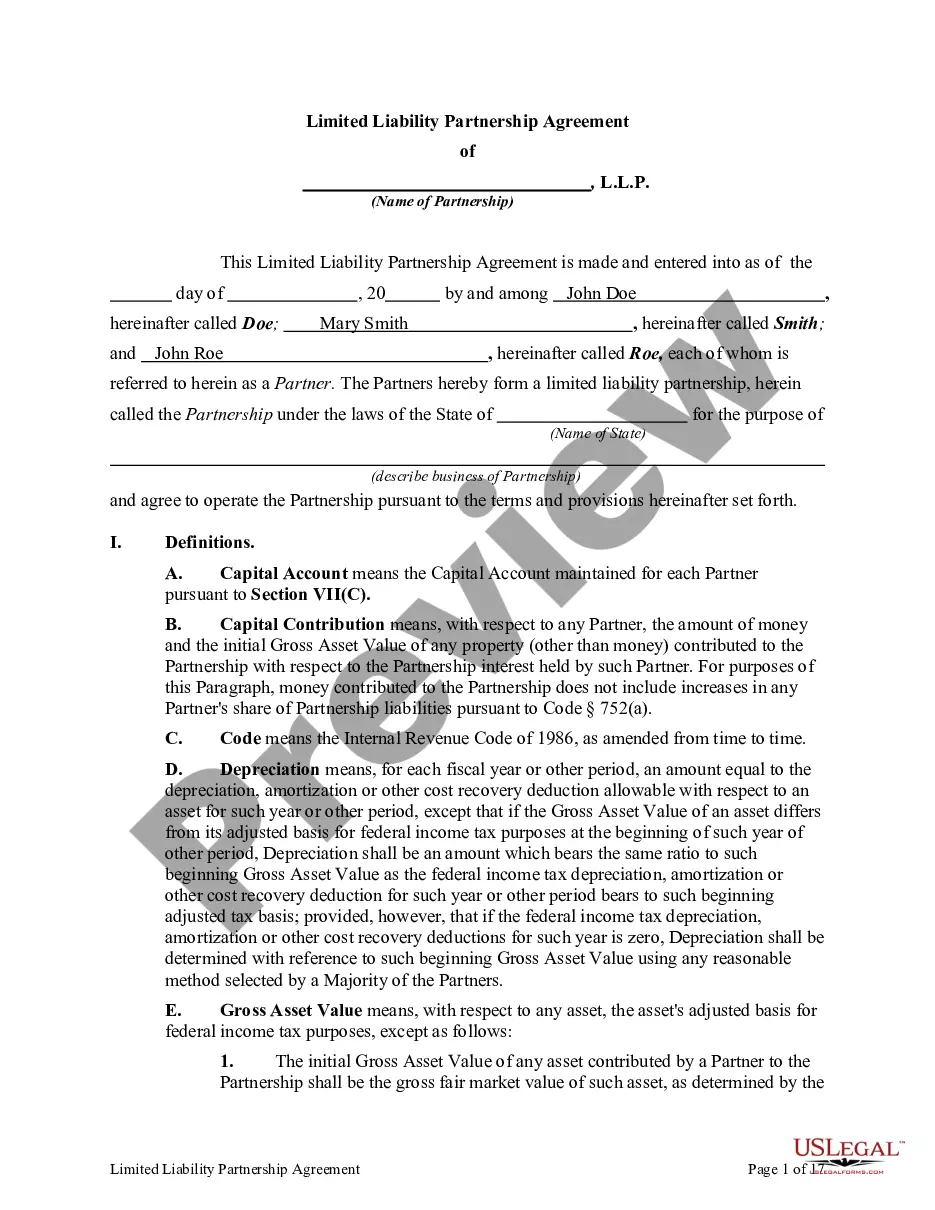

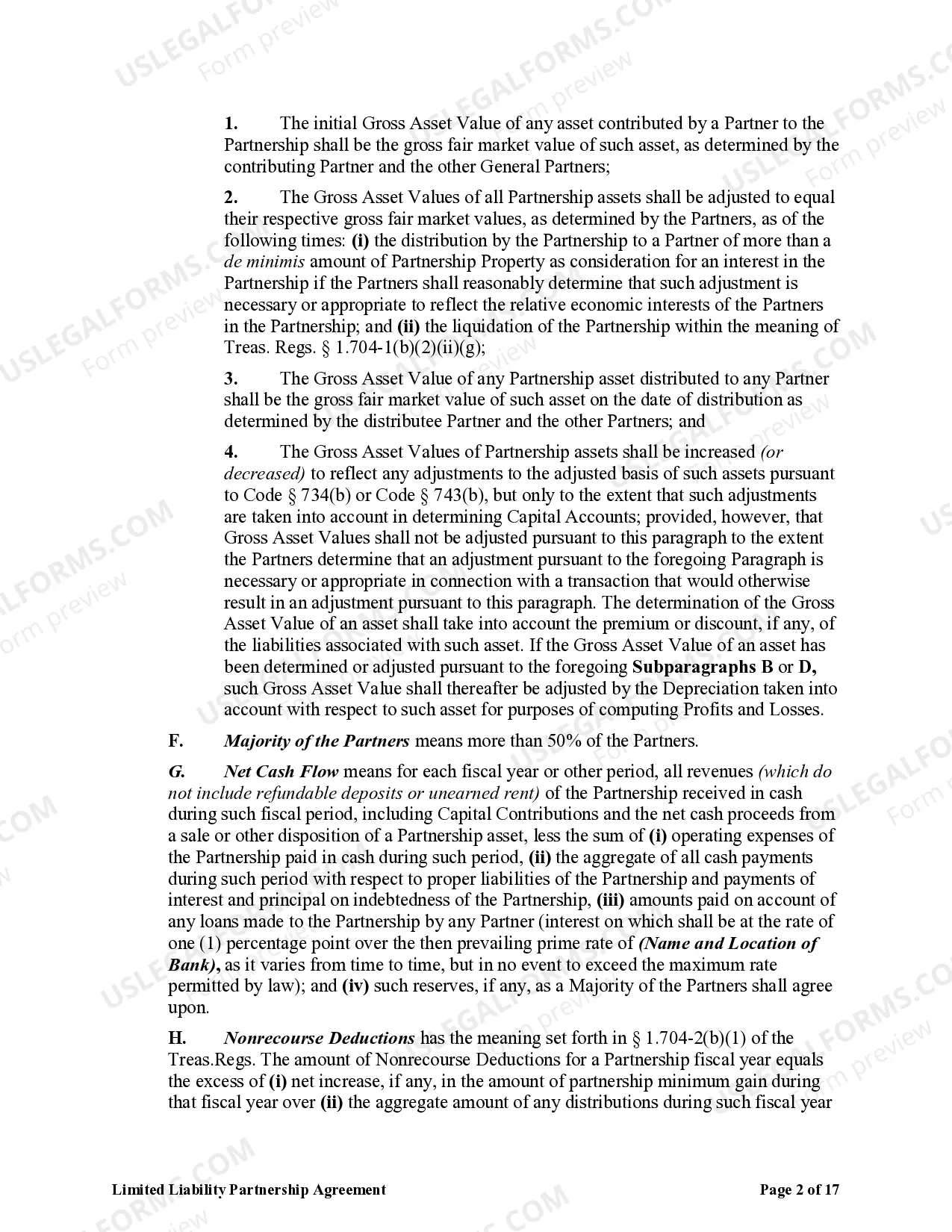

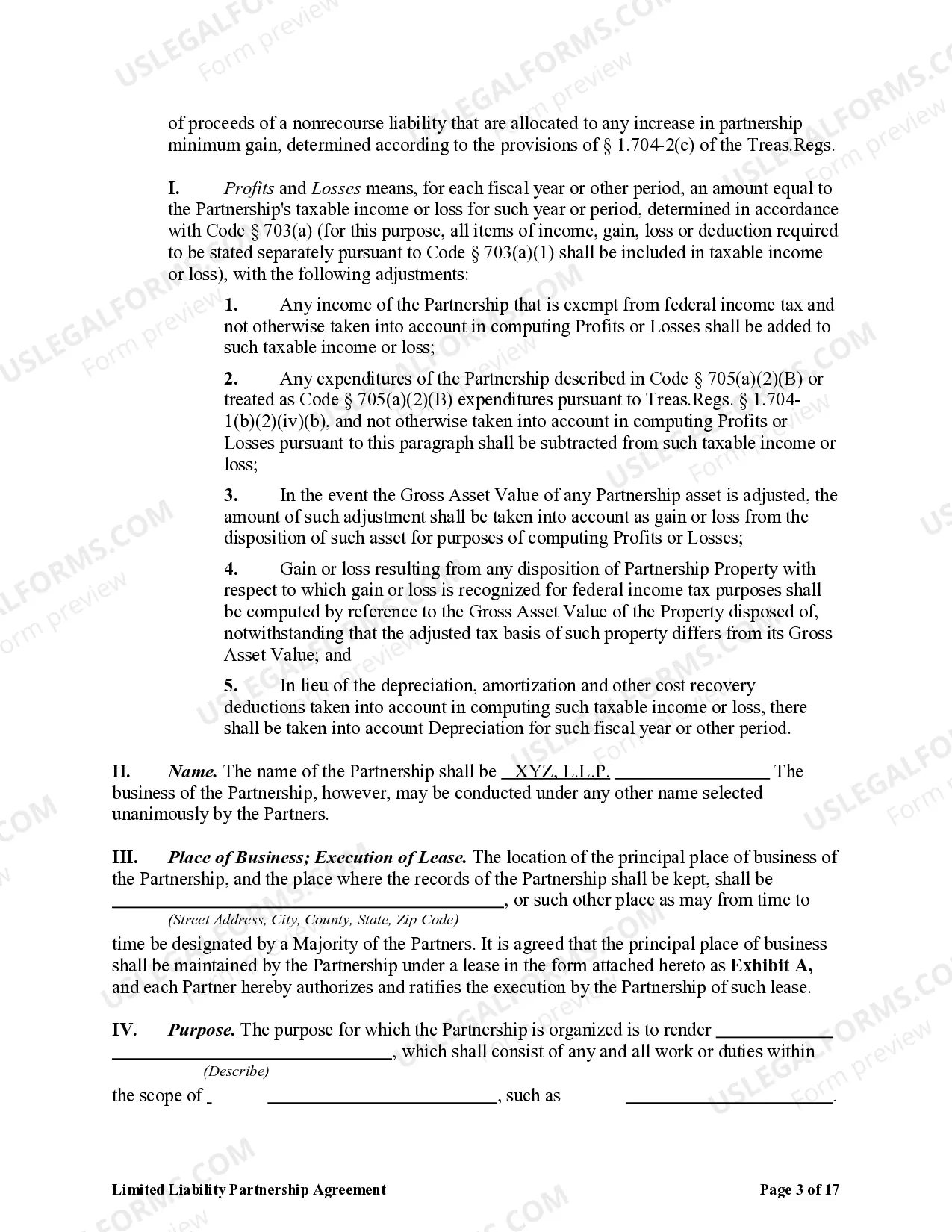

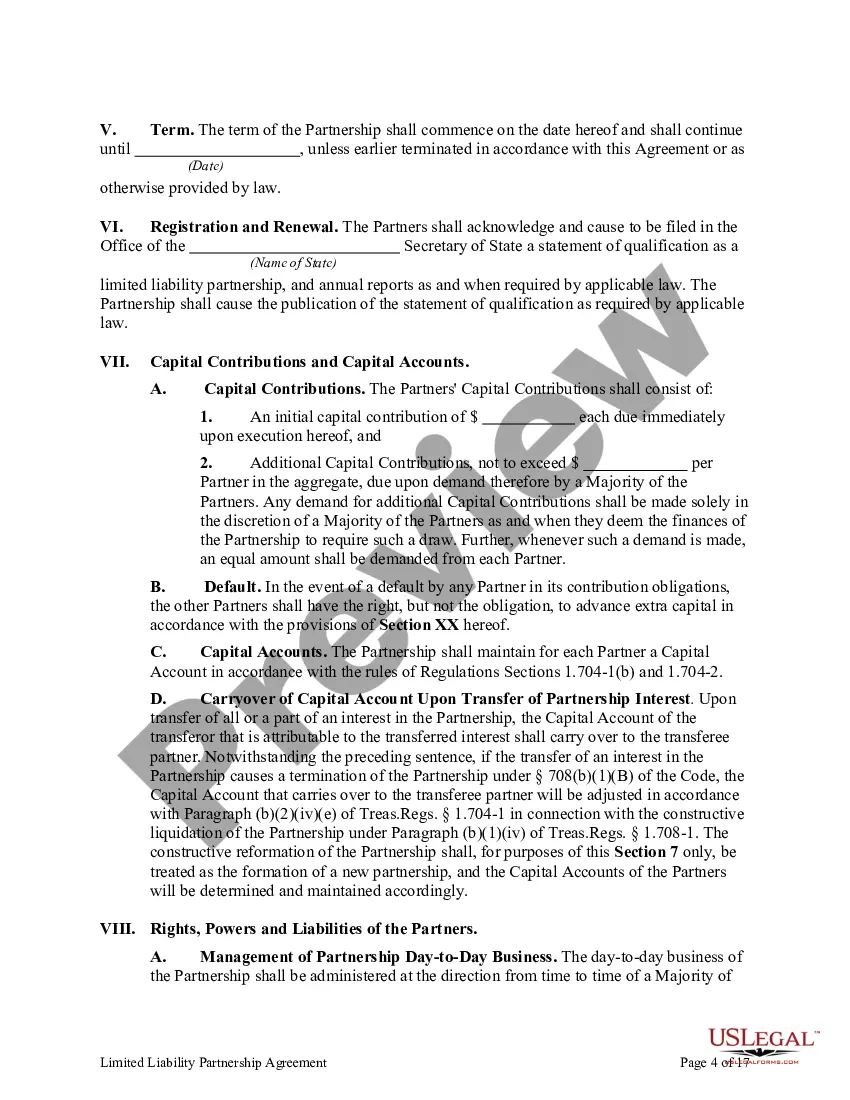

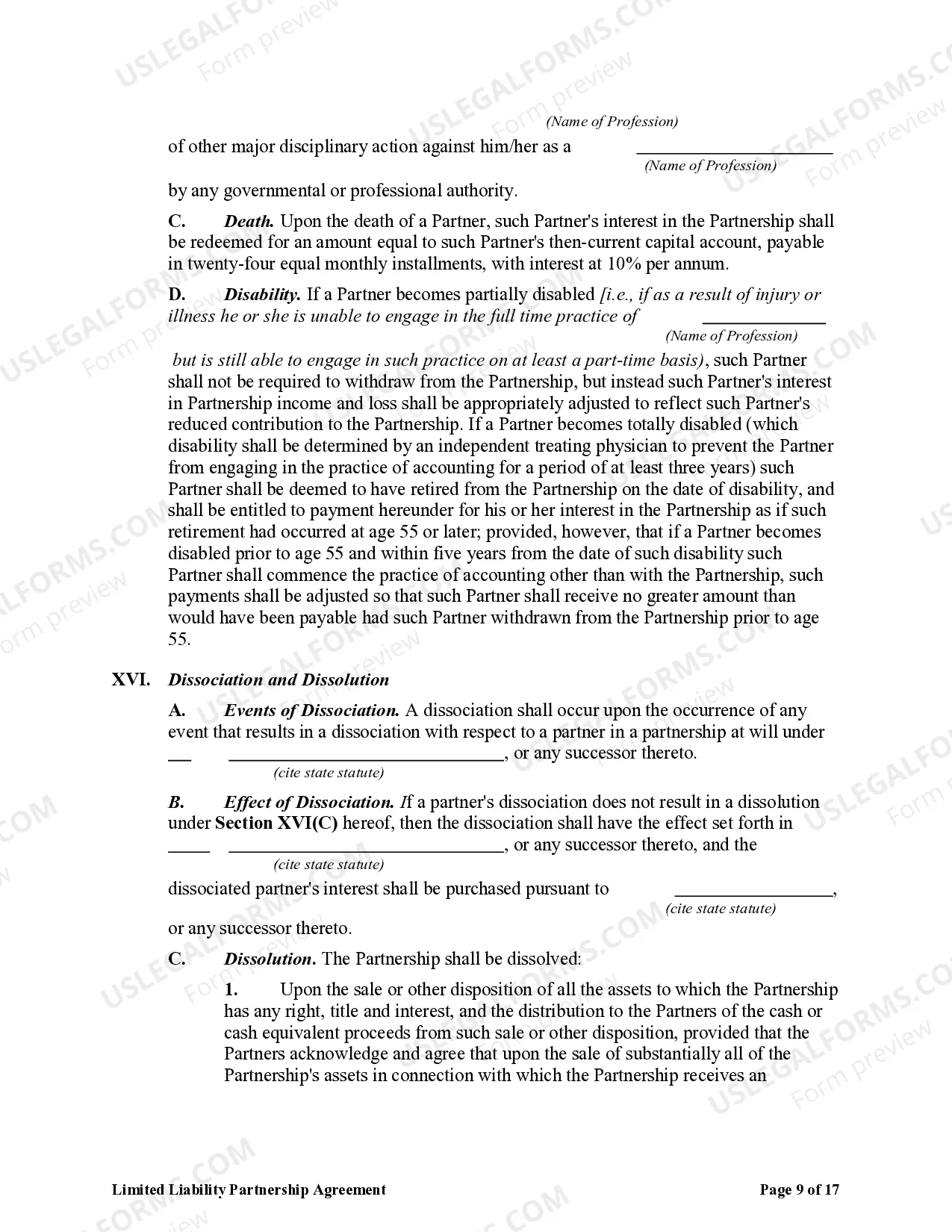

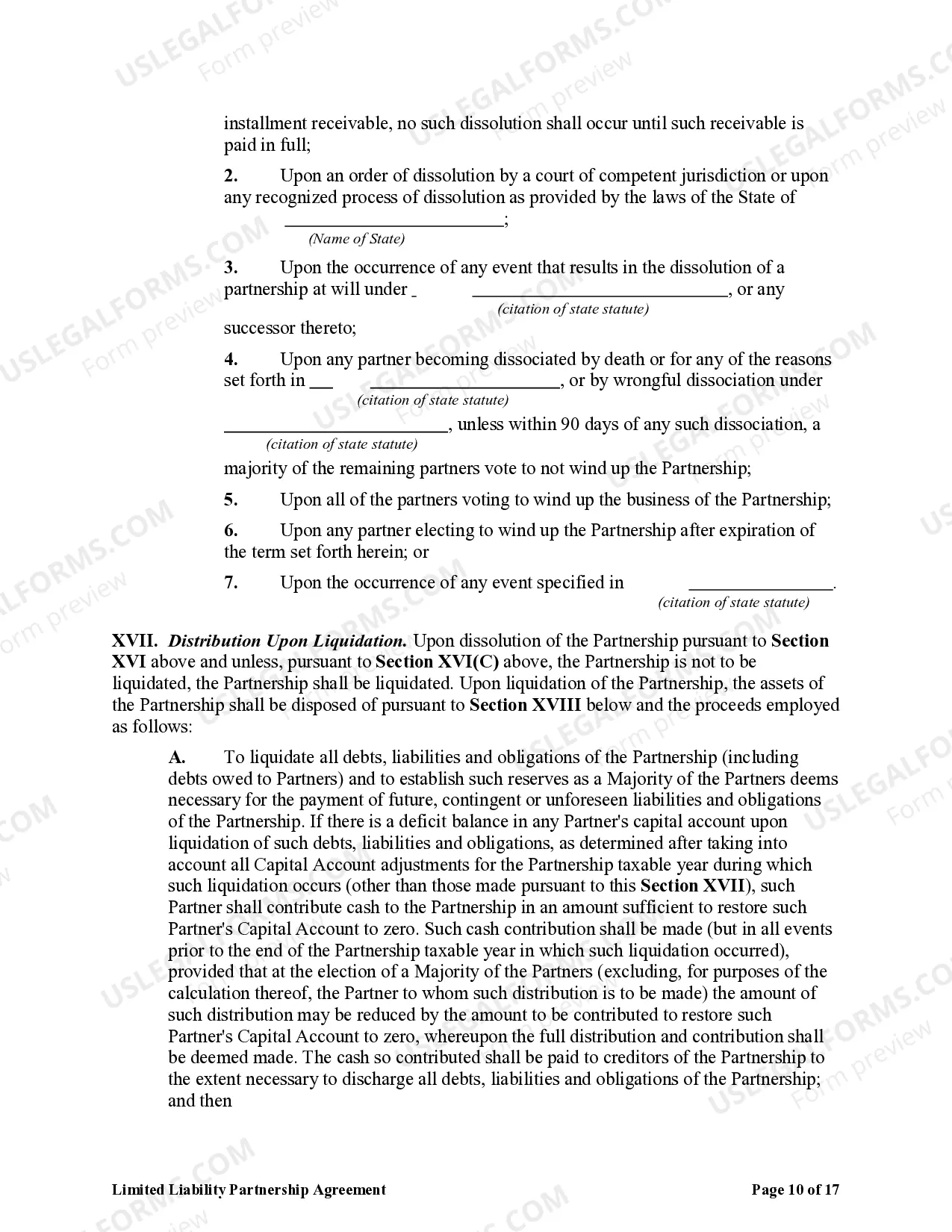

A Vermont Limited Liability Partnership Agreement (LLP) is a legal document that outlines the specific terms, conditions, and responsibilities of partners in a limited liability partnership based in Vermont. An LLP is formed when professionals, such as lawyers, accountants, architects, or engineers, come together and choose to operate their business as a partnership, but with the added benefit of limited liability protection. A key characteristic of a Vermont LLP is that it provides personal liability protection to partners within the partnership. This means that each partner's personal assets are protected from certain partnership liabilities and debts, much like in a corporation. However, it's important to note that individual partners may still be held personally liable for their own actions and professional negligence. A Vermont LLP Agreement typically includes various provisions, such as: 1. Identification: The agreement identifies the partners' names, addresses, and the name of the LLP. 2. Purpose: The agreement highlights the specific professional services the partnership intends to provide. 3. Capital Contributions: It outlines the agreed-upon contributions made by each partner, which could be in the form of cash, property, or services. 4. Profit and Loss Allocations: The agreement states how the partnership's profits and losses will be distributed among the partners and any agreed-upon sharing percentages or formulas. 5. Decision-Making Authority: It specifies how major decisions will be made and whether all partners need to agree or if a majority vote can suffice. 6. Management and Control: The agreement outlines the roles and responsibilities of each partner and whether there will be a designated managing partner. 7. Withdrawal or Death of a Partner: It defines the procedures for a partner's withdrawal from the LLP or in the event of their death, including the buyout of their interest. 8. Dissolution: The agreement sets out the process for dissolving the LLP and how assets and liabilities will be distributed among the partners. In Vermont, there are no specific types of LLP agreements outlined by the state. However, partners can customize their LLP agreement based on their specific needs and requirements. For example, they may choose to incorporate additional clauses related to non-compete agreements, client ownership, or dispute resolution procedures. In conclusion, a Vermont Limited Liability Partnership Agreement is a legally binding document that provides a framework for the operations, responsibilities, and liabilities of partners in an LLP. It allows professionals to form a partnership while enjoying the benefits of limited liability protection.

Vermont Limited Liability Partnership Agreement

Description

How to fill out Vermont Limited Liability Partnership Agreement?

Choosing the right authorized record template can be a have a problem. Needless to say, there are a variety of layouts accessible on the Internet, but how would you discover the authorized form you require? Take advantage of the US Legal Forms web site. The support provides a large number of layouts, for example the Vermont Limited Liability Partnership Agreement, which can be used for organization and private requires. Every one of the forms are examined by experts and fulfill state and federal demands.

If you are previously listed, log in for your accounts and then click the Obtain key to obtain the Vermont Limited Liability Partnership Agreement. Use your accounts to appear with the authorized forms you might have acquired formerly. Proceed to the My Forms tab of the accounts and acquire one more backup of the record you require.

If you are a whole new consumer of US Legal Forms, here are simple directions so that you can adhere to:

- Very first, make sure you have selected the appropriate form to your town/area. You can look over the form utilizing the Review key and read the form explanation to guarantee it is the right one for you.

- If the form fails to fulfill your requirements, use the Seach field to find the appropriate form.

- Once you are positive that the form is suitable, click the Purchase now key to obtain the form.

- Select the pricing prepare you would like and enter the necessary information. Make your accounts and purchase the transaction utilizing your PayPal accounts or bank card.

- Select the submit structure and down load the authorized record template for your product.

- Total, modify and produce and indication the attained Vermont Limited Liability Partnership Agreement.

US Legal Forms is definitely the greatest collection of authorized forms in which you will find numerous record layouts. Take advantage of the service to down load professionally-manufactured documents that adhere to express demands.