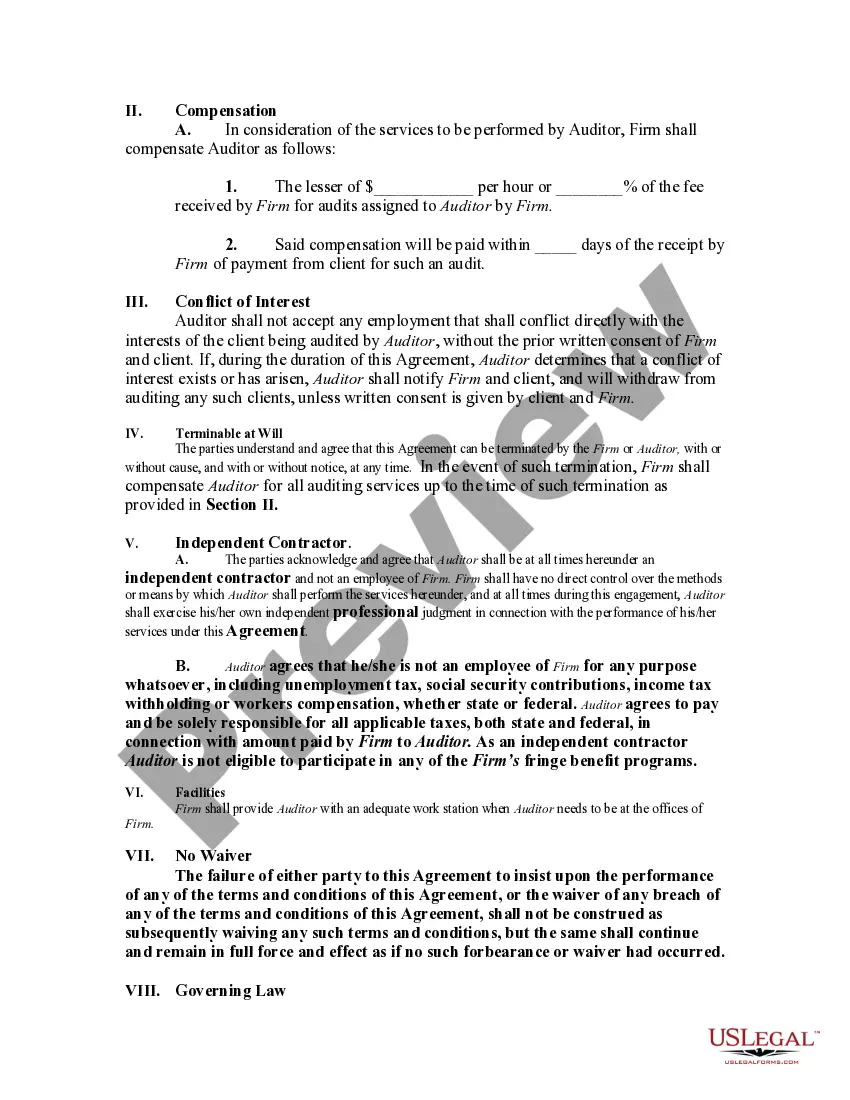

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

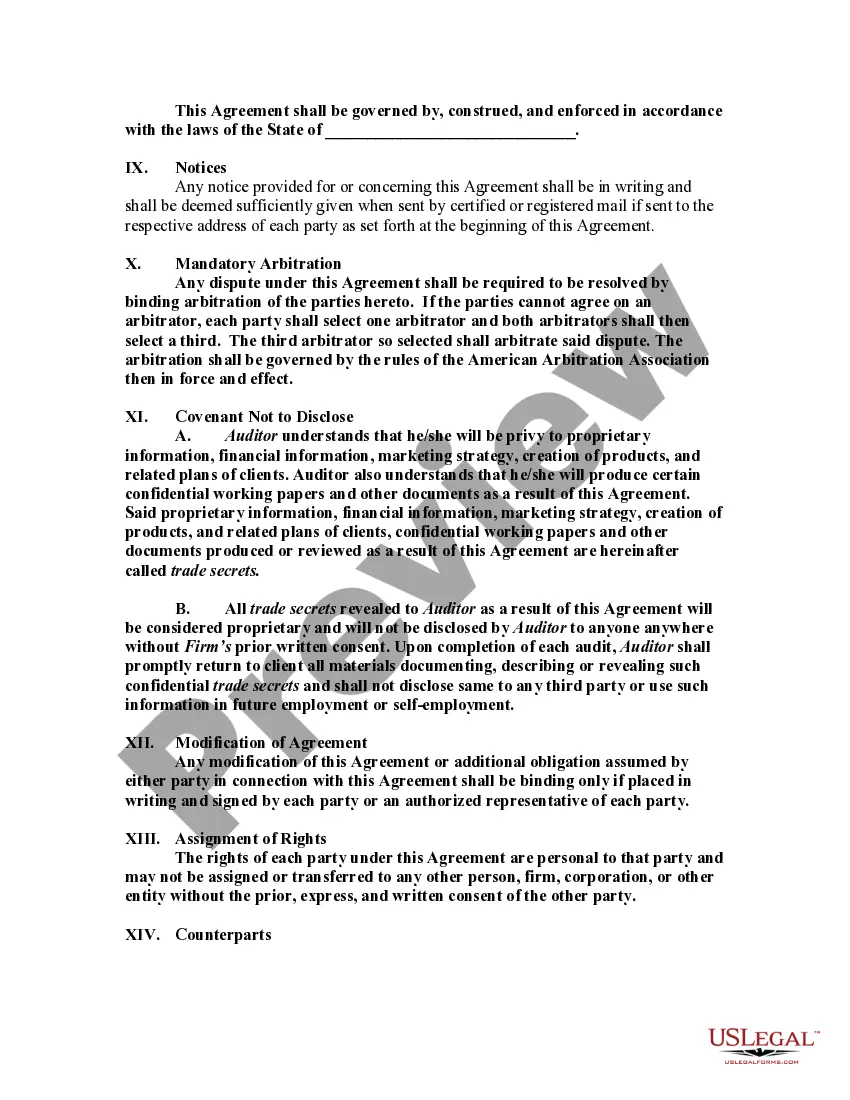

Title: Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: A Comprehensive Guide Introduction: In Vermont, accounting firms often engage auditors as self-employed independent contractors to provide specialized services. The Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor ensures a mutually beneficial working relationship between the firm and the auditor while adhering to Vermont labor laws. This comprehensive guide will provide a detailed description of this agreement, including its key components, benefits, important considerations, and any sub-types that may exist. Key Components of a Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Identification of Parties: Clearly define the accounting firm (employer) and the auditor (self-employed independent contractor) involved in the agreement, including their legal names and contact information. 2. Scope of Services: Enumerate the specific services the auditor will be providing, such as financial statement audits, internal controls assessments, or tax compliance reviews. Be specific about project timelines, objectives, and the expected deliverables. 3. Compensation and Payment Terms: Discuss the remuneration structure, whether it is a fixed fee, hourly rate, or a combination of both. Specify the payment schedule and any applicable terms for reimbursement of reasonable expenses incurred during the engagement. 4. Independent Contractor Status: Outline the terms that establish the auditor's status as a self-employed independent contractor, emphasizing that the auditor is not an employee of the accounting firm. Mention Vermont labor law compliance requirements, including tax obligations, insurance coverage, and worker classification regulations. 5. Confidentiality and Non-Disclosure: Detail the confidentiality obligations the auditor must observe regarding sensitive company and client information. Include provisions addressing the handling of data, intellectual property, and privacy concerns, affirming the auditor's responsibility to maintain confidentiality even after the engagement terminates. 6. Intellectual Property and Ownership: Disclose the ownership rights to work products generated during the engagement, establishing whether the accounting firm will retain ownership or if any IP rights will belong to the auditor. 7. Termination Clause: Specify the conditions under which either party can terminate the agreement, including any notice periods and procedures to be followed. Address situations such as breach of contract, bankruptcy, or changes in circumstances that may lead to termination. Different Types of Vermont Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: While the core elements of the agreement remain largely consistent, certain sub-types may arise based on specific circumstances or the nature of the engagement. These may include: 1. Temporary Engagement Agreement: A short-term agreement where the accounting firm hires an auditor as a self-employed independent contractor for a specific project or a defined period, typically to address a one-time audit requirement or a seasonal spike in workload. 2. Long-term Engagement Agreement: A comprehensive agreement with an extended duration where the accounting firm engages an auditor as a self-employed independent contractor for ongoing audit and financial examination services, establishing a continuous working relationship. 3. Specialty Services Agreement: This agreement focuses on engaging auditors with specialized expertise or niche skills required for specific audit areas, such as forensic accounting, internal controls design, or IT auditing. Conclusion: The Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital tool for establishing a legally compliant working relationship between accounting firms and auditors. By delineating key components, it ensures transparency, mutual understanding, and compliance with Vermont labor laws. It is crucial to tailor the agreement to suit the specific needs of the engagement, whether it is a temporary, long-term, or specialty services arrangement.Title: Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: A Comprehensive Guide Introduction: In Vermont, accounting firms often engage auditors as self-employed independent contractors to provide specialized services. The Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor ensures a mutually beneficial working relationship between the firm and the auditor while adhering to Vermont labor laws. This comprehensive guide will provide a detailed description of this agreement, including its key components, benefits, important considerations, and any sub-types that may exist. Key Components of a Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Identification of Parties: Clearly define the accounting firm (employer) and the auditor (self-employed independent contractor) involved in the agreement, including their legal names and contact information. 2. Scope of Services: Enumerate the specific services the auditor will be providing, such as financial statement audits, internal controls assessments, or tax compliance reviews. Be specific about project timelines, objectives, and the expected deliverables. 3. Compensation and Payment Terms: Discuss the remuneration structure, whether it is a fixed fee, hourly rate, or a combination of both. Specify the payment schedule and any applicable terms for reimbursement of reasonable expenses incurred during the engagement. 4. Independent Contractor Status: Outline the terms that establish the auditor's status as a self-employed independent contractor, emphasizing that the auditor is not an employee of the accounting firm. Mention Vermont labor law compliance requirements, including tax obligations, insurance coverage, and worker classification regulations. 5. Confidentiality and Non-Disclosure: Detail the confidentiality obligations the auditor must observe regarding sensitive company and client information. Include provisions addressing the handling of data, intellectual property, and privacy concerns, affirming the auditor's responsibility to maintain confidentiality even after the engagement terminates. 6. Intellectual Property and Ownership: Disclose the ownership rights to work products generated during the engagement, establishing whether the accounting firm will retain ownership or if any IP rights will belong to the auditor. 7. Termination Clause: Specify the conditions under which either party can terminate the agreement, including any notice periods and procedures to be followed. Address situations such as breach of contract, bankruptcy, or changes in circumstances that may lead to termination. Different Types of Vermont Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: While the core elements of the agreement remain largely consistent, certain sub-types may arise based on specific circumstances or the nature of the engagement. These may include: 1. Temporary Engagement Agreement: A short-term agreement where the accounting firm hires an auditor as a self-employed independent contractor for a specific project or a defined period, typically to address a one-time audit requirement or a seasonal spike in workload. 2. Long-term Engagement Agreement: A comprehensive agreement with an extended duration where the accounting firm engages an auditor as a self-employed independent contractor for ongoing audit and financial examination services, establishing a continuous working relationship. 3. Specialty Services Agreement: This agreement focuses on engaging auditors with specialized expertise or niche skills required for specific audit areas, such as forensic accounting, internal controls design, or IT auditing. Conclusion: The Vermont Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital tool for establishing a legally compliant working relationship between accounting firms and auditors. By delineating key components, it ensures transparency, mutual understanding, and compliance with Vermont labor laws. It is crucial to tailor the agreement to suit the specific needs of the engagement, whether it is a temporary, long-term, or specialty services arrangement.