An assignment is a transfer of rights that a party has under a contract to another person, called an assignee. The assigning party is called the assignor. An assignee of a contract may generally sue directly on the contract rather than suing in the name of the assignor. The obligor is the person responsible to make payments to the assignee.

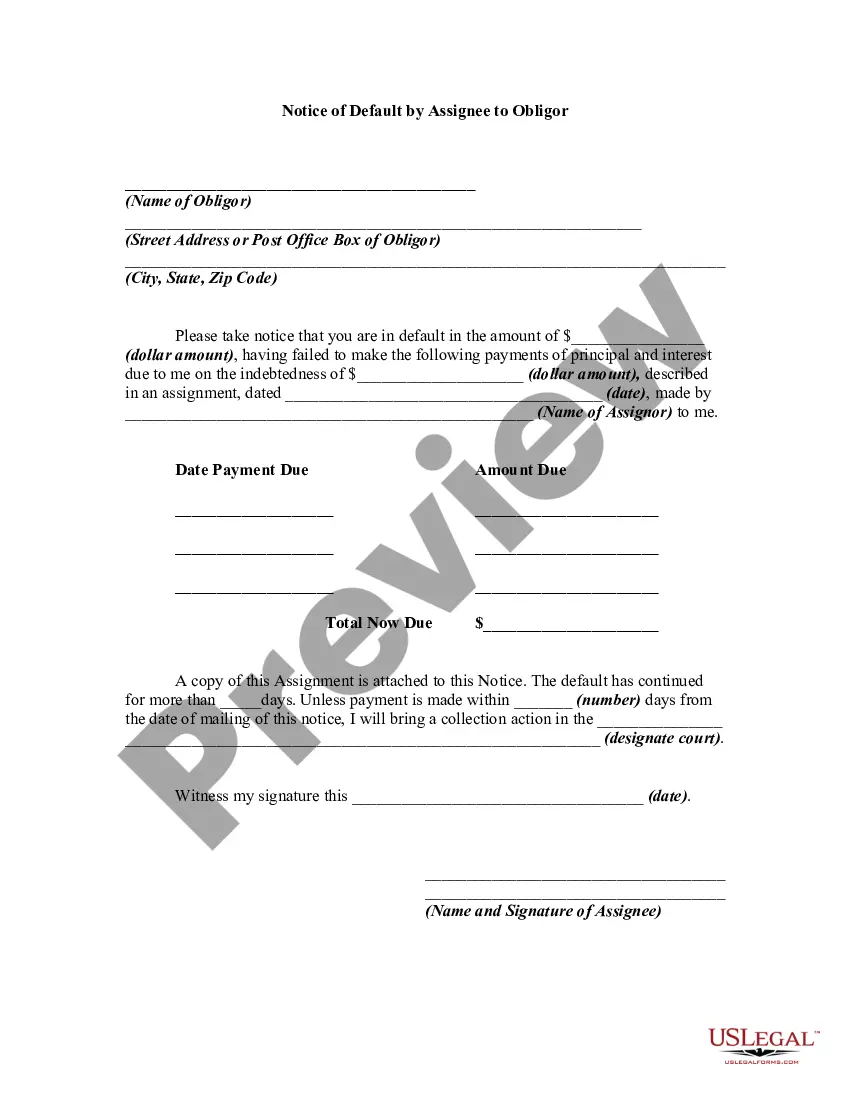

Vermont Notice of Default by Assignee to Obliged Keywords: Vermont, Notice of Default, Assignee, Obliged A Vermont Notice of Default by Assignee to Obliged is a legal document that marks the initiation of a foreclosure process in the state of Vermont. It is a notification sent by the assignee of a mortgage or loan (typically a bank or lender) to the obliged (the borrower) when the obliged fails to fulfill their payment obligations as agreed upon in the loan agreement. This document informs the obliged that they are in default and provides specific details regarding the default, along with the actions required to cure the default. There are various types of Vermont Notice of Default by Assignee to Obliged, each serving specific purposes. These can include: 1. Mortgage Default Notice: This type of notice is issued by the assignee (usually a mortgage lender) to the obliged when the borrower fails to make the required mortgage payments within the specified timeframe. It states the amount due, the date of default, and provides instructions on how to remedy the default. 2. Loan Default Notice: A Loan Default Notice serves a similar purpose to the Mortgage Default Notice but is typically used for non-mortgage loans such as personal loans, auto loans, or business loans. It notifies the obliged of their default and provides details about the outstanding balance, payment due date, and steps to cure the default. 3. Notice of Default Cure: This type of notice is issued by the assignee to the obliged when the borrower has expressed an intention to cure their default. It outlines the specific actions required to rectify the default within a given timeframe, such as making overdue payments or entering into a repayment plan. 4. Notice of Acceleration: In situations where the borrower fails to cure the default within the specified timeframe, the assignee may issue a Notice of Acceleration. This notice informs the obliged that the entire loan amount has become due and payable immediately, accelerating the payment schedule. 5. Notice of Foreclosure Sale: If the obliged fails to cure the default or meet the obligations outlined in the Notice of Acceleration, the assignee may proceed to initiate foreclosure proceedings. A Notice of Foreclosure Sale is then issued, which provides detailed information about the upcoming auction or sale of the property securing the loan. It is essential for both the assignee and the obliged to be familiar with the terms and conditions outlined in the Vermont Notice of Default by Assignee to Oblige. It is recommended that the obliged seek legal advice and explore all available options to resolve the default and prevent further legal action.Vermont Notice of Default by Assignee to Obliged Keywords: Vermont, Notice of Default, Assignee, Obliged A Vermont Notice of Default by Assignee to Obliged is a legal document that marks the initiation of a foreclosure process in the state of Vermont. It is a notification sent by the assignee of a mortgage or loan (typically a bank or lender) to the obliged (the borrower) when the obliged fails to fulfill their payment obligations as agreed upon in the loan agreement. This document informs the obliged that they are in default and provides specific details regarding the default, along with the actions required to cure the default. There are various types of Vermont Notice of Default by Assignee to Obliged, each serving specific purposes. These can include: 1. Mortgage Default Notice: This type of notice is issued by the assignee (usually a mortgage lender) to the obliged when the borrower fails to make the required mortgage payments within the specified timeframe. It states the amount due, the date of default, and provides instructions on how to remedy the default. 2. Loan Default Notice: A Loan Default Notice serves a similar purpose to the Mortgage Default Notice but is typically used for non-mortgage loans such as personal loans, auto loans, or business loans. It notifies the obliged of their default and provides details about the outstanding balance, payment due date, and steps to cure the default. 3. Notice of Default Cure: This type of notice is issued by the assignee to the obliged when the borrower has expressed an intention to cure their default. It outlines the specific actions required to rectify the default within a given timeframe, such as making overdue payments or entering into a repayment plan. 4. Notice of Acceleration: In situations where the borrower fails to cure the default within the specified timeframe, the assignee may issue a Notice of Acceleration. This notice informs the obliged that the entire loan amount has become due and payable immediately, accelerating the payment schedule. 5. Notice of Foreclosure Sale: If the obliged fails to cure the default or meet the obligations outlined in the Notice of Acceleration, the assignee may proceed to initiate foreclosure proceedings. A Notice of Foreclosure Sale is then issued, which provides detailed information about the upcoming auction or sale of the property securing the loan. It is essential for both the assignee and the obliged to be familiar with the terms and conditions outlined in the Vermont Notice of Default by Assignee to Oblige. It is recommended that the obliged seek legal advice and explore all available options to resolve the default and prevent further legal action.