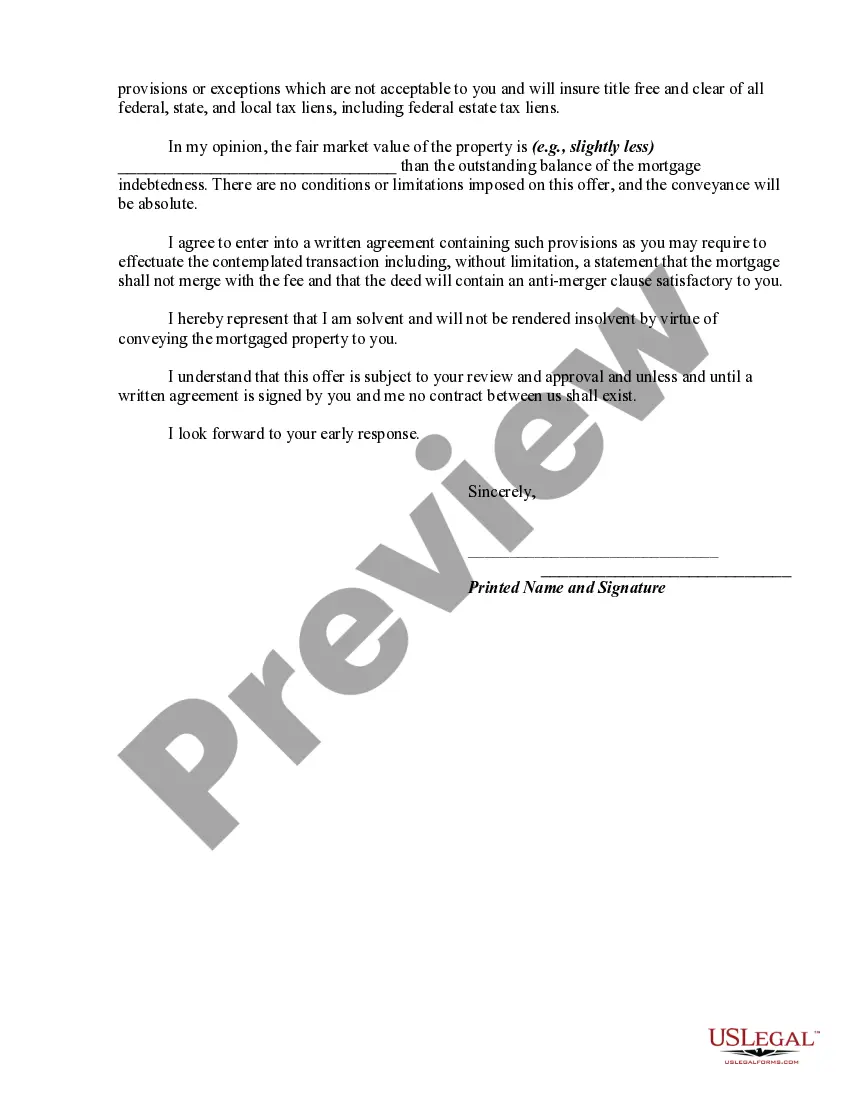

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Vermont Offer by Borrower of Deed in Lieu of Foreclosure is a process where a homeowner in Vermont facing financial difficulties voluntarily transfers their property deed back to the lender in order to avoid foreclosure. This alternative option allows the borrower to avoid the lengthy and potentially damaging foreclosure process and may provide a more favorable outcome for both parties involved. The Vermont Offer by Borrower of Deed in Lieu of Foreclosure is a legal agreement between the borrower and the lender that should be executed with the help of an attorney or a real estate professional. It is crucial for borrowers to fully understand the implications and potential consequences of opting for this solution before proceeding. One of the key benefits of the Vermont Offer by Borrower of Deed in Lieu of Foreclosure is that it allows the borrower to minimize the negative impact on their credit score compared to a foreclosure. By proactively working with the lender, borrowers can negotiate favorable terms such as the release of any remaining mortgage debt, exemption from deficiency judgments, and possible relocation assistance. Different types of Vermont Offer by Borrower of Deed in Lieu of Foreclosure may include: 1. Standard Vermont Offer by Borrower of Deed in Lieu of Foreclosure: This is the typical and most commonly used type. It involves the borrower willingly transferring the property title to the lender to satisfy the loan obligation. 2. Conditional Vermont Offer by Borrower of Deed in Lieu of Foreclosure: In certain cases, the lender may impose conditions on the borrower before accepting the deed in lieu. These conditions may include providing evidence of attempts to sell the property through a short sale, maintaining the property in good condition until transfer, or paying off certain outstanding liens. 3. Partial Release Vermont Offer by Borrower of Deed in Lieu of Foreclosure: In some instances, the lender may accept a partial deed transfer instead of the entire property. This can be negotiated when the borrower possesses multiple properties subject to foreclosure, allowing them to retain ownership of a portion of their real estate assets. 4. Cooperative Vermont Offer by Borrower of Deed in Lieu of Foreclosure: This type involves a collaborative effort between the borrower and the lender to complete the process smoothly. Both parties work together closely to ensure a favorable outcome for both the borrower and the lender. It is crucial for borrowers in Vermont to fully understand the terms and implications of the Offer by Borrower of Deed in Lieu of Foreclosure before proceeding with this option. Seeking guidance from legal or real estate professionals can help homeowners make informed decisions about their financial situation, protect their rights, and explore potential alternatives to foreclosure.Vermont Offer by Borrower of Deed in Lieu of Foreclosure is a process where a homeowner in Vermont facing financial difficulties voluntarily transfers their property deed back to the lender in order to avoid foreclosure. This alternative option allows the borrower to avoid the lengthy and potentially damaging foreclosure process and may provide a more favorable outcome for both parties involved. The Vermont Offer by Borrower of Deed in Lieu of Foreclosure is a legal agreement between the borrower and the lender that should be executed with the help of an attorney or a real estate professional. It is crucial for borrowers to fully understand the implications and potential consequences of opting for this solution before proceeding. One of the key benefits of the Vermont Offer by Borrower of Deed in Lieu of Foreclosure is that it allows the borrower to minimize the negative impact on their credit score compared to a foreclosure. By proactively working with the lender, borrowers can negotiate favorable terms such as the release of any remaining mortgage debt, exemption from deficiency judgments, and possible relocation assistance. Different types of Vermont Offer by Borrower of Deed in Lieu of Foreclosure may include: 1. Standard Vermont Offer by Borrower of Deed in Lieu of Foreclosure: This is the typical and most commonly used type. It involves the borrower willingly transferring the property title to the lender to satisfy the loan obligation. 2. Conditional Vermont Offer by Borrower of Deed in Lieu of Foreclosure: In certain cases, the lender may impose conditions on the borrower before accepting the deed in lieu. These conditions may include providing evidence of attempts to sell the property through a short sale, maintaining the property in good condition until transfer, or paying off certain outstanding liens. 3. Partial Release Vermont Offer by Borrower of Deed in Lieu of Foreclosure: In some instances, the lender may accept a partial deed transfer instead of the entire property. This can be negotiated when the borrower possesses multiple properties subject to foreclosure, allowing them to retain ownership of a portion of their real estate assets. 4. Cooperative Vermont Offer by Borrower of Deed in Lieu of Foreclosure: This type involves a collaborative effort between the borrower and the lender to complete the process smoothly. Both parties work together closely to ensure a favorable outcome for both the borrower and the lender. It is crucial for borrowers in Vermont to fully understand the terms and implications of the Offer by Borrower of Deed in Lieu of Foreclosure before proceeding with this option. Seeking guidance from legal or real estate professionals can help homeowners make informed decisions about their financial situation, protect their rights, and explore potential alternatives to foreclosure.