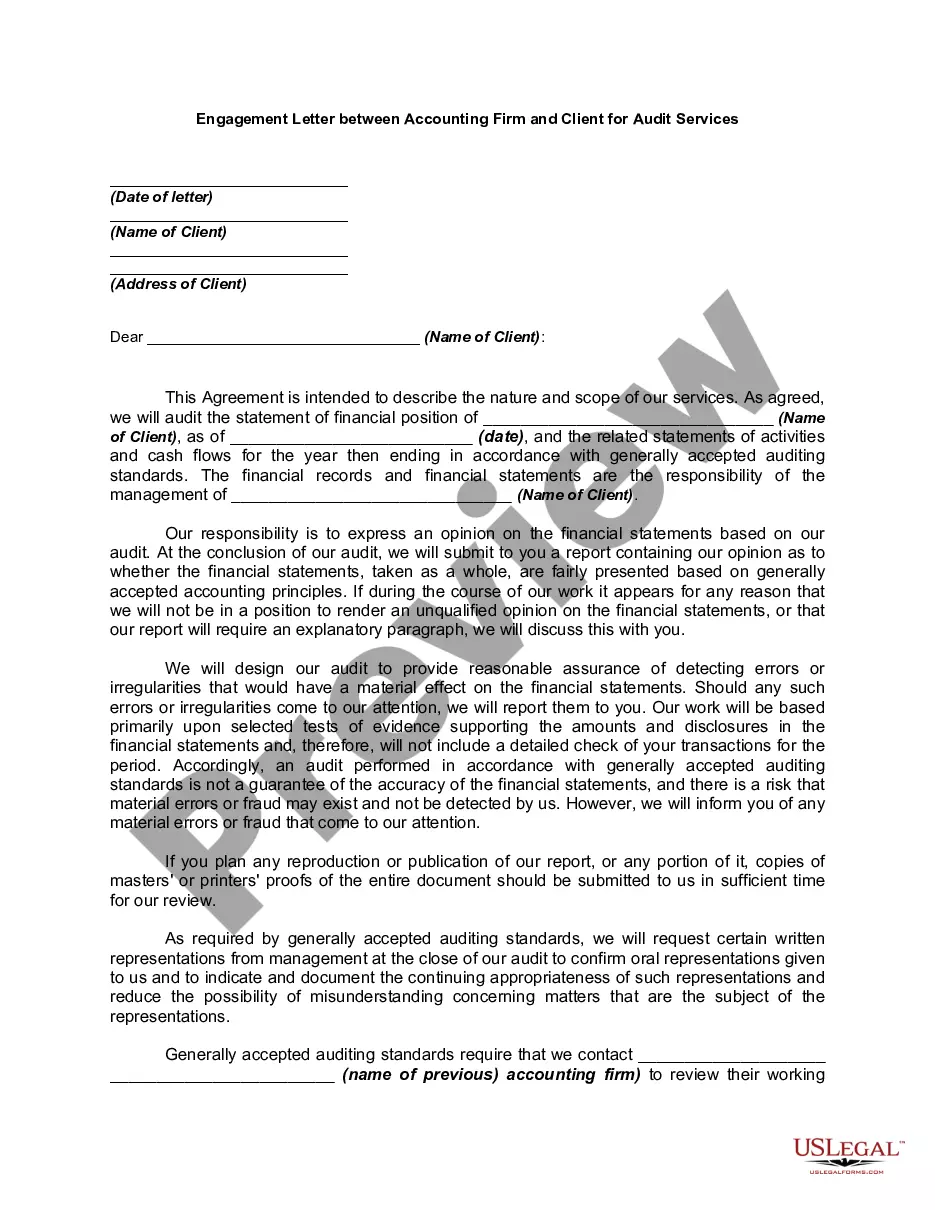

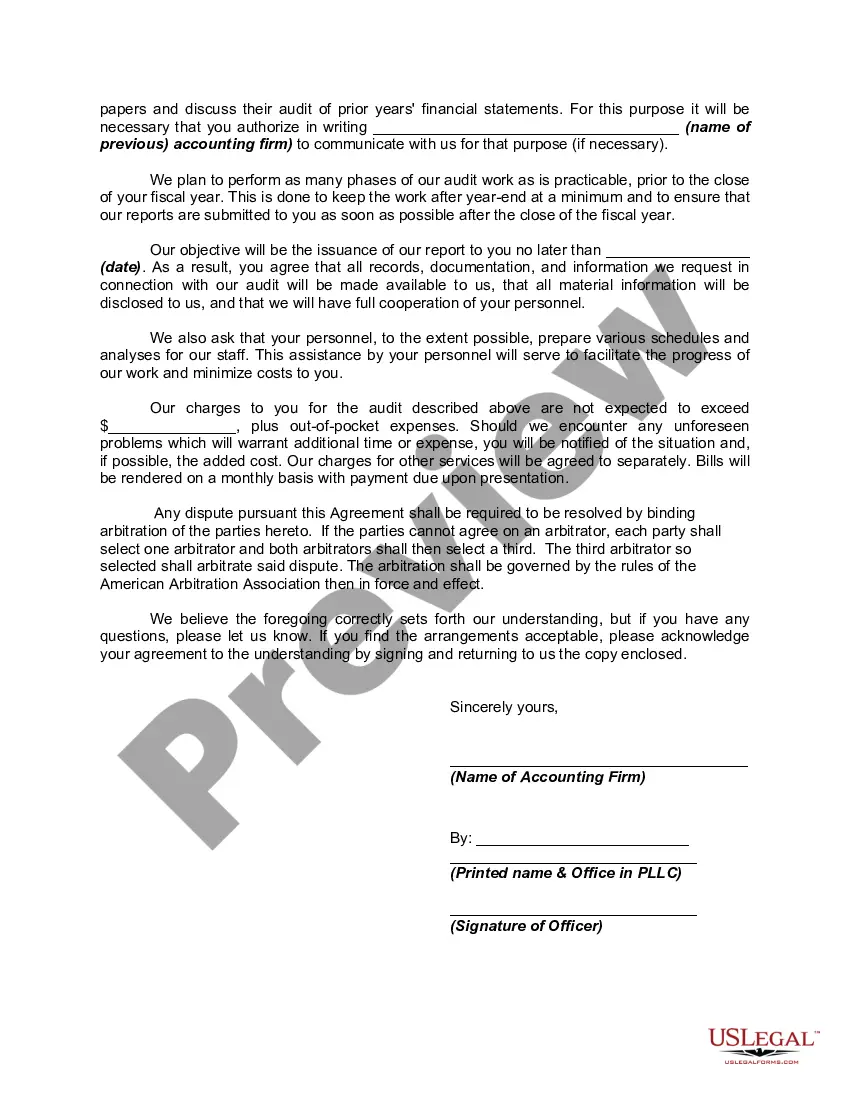

Generally, a contract to employ a certified public accountant need not be in writing.

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Vermont Engagement Letter Between Accounting Firm and Client For Audit Services An engagement letter is a crucial document that lays out the terms and conditions of an agreement between an accounting firm and its client for audit services. In Vermont, these engagement letters primarily serve as a legally binding contract outlining the responsibilities, expectations, and limitations of both parties involved in the audit process. Let's take a closer look at what a typical Vermont engagement letter consists of and explore different types of engagement letters commonly used for audit services. 1. General Engagement Letter: The general engagement letter is the most common type of engagement letter used in Vermont for audit services. It covers the essential framework of the audit agreement, including the purpose of the engagement, the period to be audited, the responsibilities of both the accounting firm and the client, fee arrangements, and the scope of the audit. 2. Limited Scope Engagement Letter: A limited scope engagement letter is issued when the accounting firm is only required to audit specific areas or financial statements of the client's business. This type of engagement letter clearly defines the restricted scope of the audit, highlighting the areas that the accounting firm will not cover. 3. Internal Control Evaluation Engagement Letter: An internal control evaluation engagement letter occurs when the accounting firm is engaged specifically to assess and evaluate the client's internal control system and provide recommendations for improvement. The letter outlines the specific goals, objectives, timeframes, and terms pertaining to the internal control evaluation engagement. 4. Compliance Engagement Letter: The compliance engagement letter is applicable when the accounting firm is engaged to ensure the client's adherence to specific laws, regulations, or industry standards. This agreement usually details the compliance-related objectives, procedures to be followed, and any reporting obligations. 5. Special Investigative Engagement Letter: A special investigative engagement letter is used when the accounting firm is engaged to conduct a specialized investigation into specific financial transactions, fraud suspicions, or irregularities. This type of engagement letter will describe the specific scope, procedures, timelines, and expected deliverables related to the investigation. In conclusion, Vermont engagement letters between accounting firms and clients for audit services are essential in establishing a clear understanding of the terms and expectations involved in the auditing process. These letters play a significant role in ensuring transparency, maintaining client-accountant relationships, and avoiding misunderstandings. It is crucial for both parties to carefully review and agree upon the terms outlined in the engagement letter before commencing any audit activities.