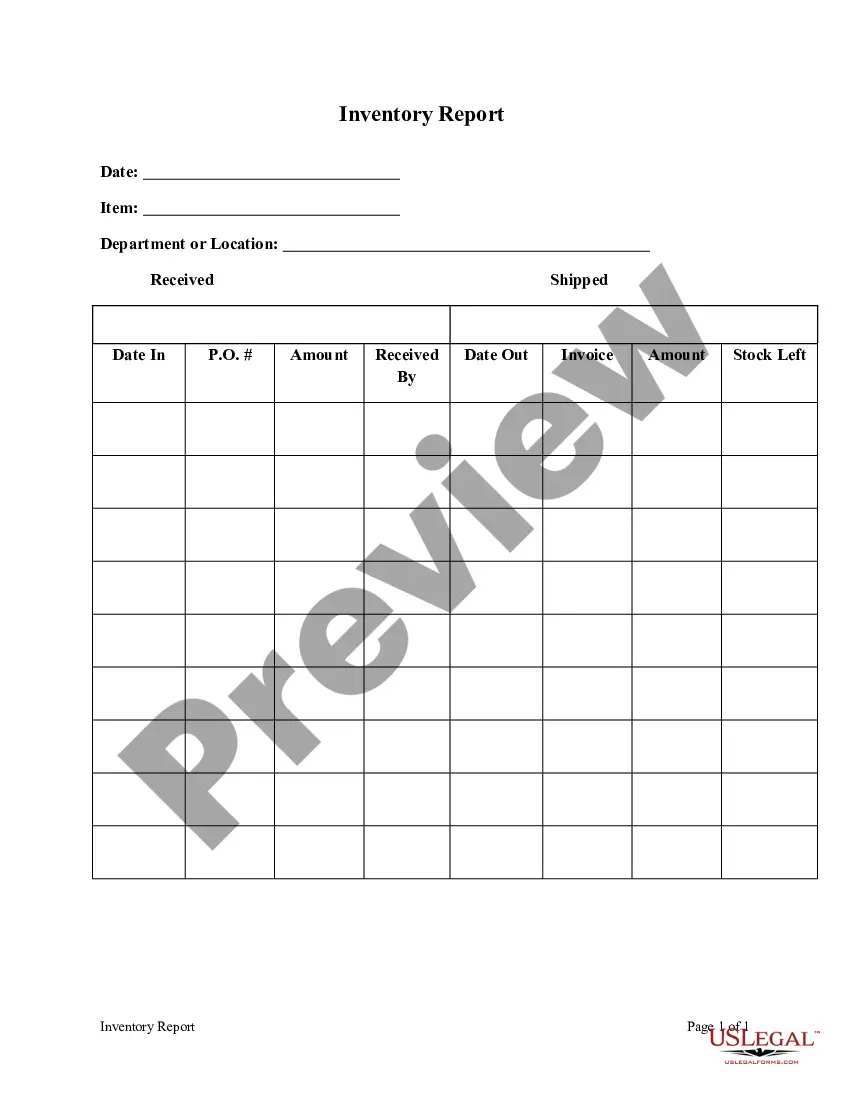

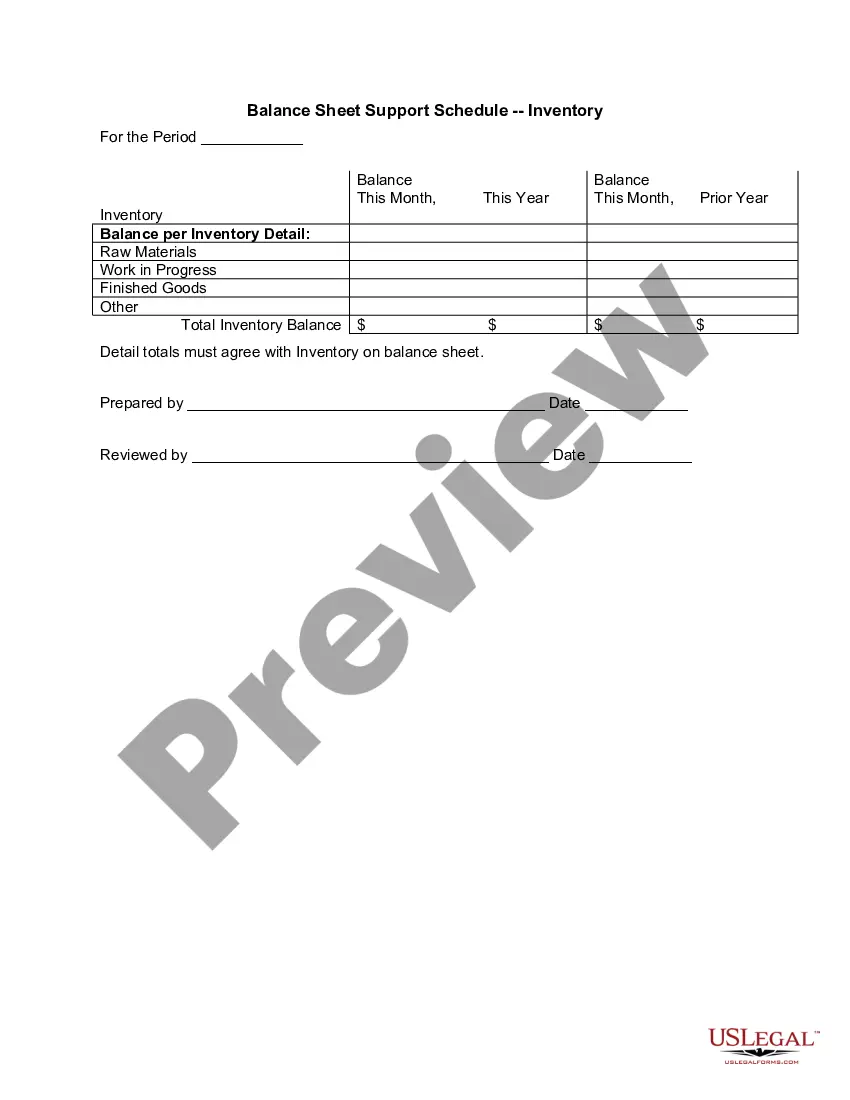

Vermont Summary of Account for Inventory of Business

Description

How to fill out Summary Of Account For Inventory Of Business?

You are able to invest hours online trying to find the legitimate record template which fits the federal and state specifications you will need. US Legal Forms provides thousands of legitimate forms which can be analyzed by experts. You can easily download or print out the Vermont Summary of Account for Inventory of Business from the assistance.

If you have a US Legal Forms accounts, you may log in and click on the Acquire key. After that, you may full, modify, print out, or signal the Vermont Summary of Account for Inventory of Business. Each legitimate record template you purchase is your own forever. To obtain another version associated with a bought type, proceed to the My Forms tab and click on the corresponding key.

If you are using the US Legal Forms internet site the first time, stick to the easy guidelines under:

- Very first, make sure that you have selected the proper record template for that state/area of your choosing. See the type explanation to make sure you have picked out the correct type. If offered, utilize the Preview key to look from the record template at the same time.

- If you want to find another edition from the type, utilize the Research field to get the template that meets your needs and specifications.

- When you have discovered the template you want, click Buy now to continue.

- Find the prices plan you want, type your credentials, and register for a free account on US Legal Forms.

- Total the deal. You can use your charge card or PayPal accounts to fund the legitimate type.

- Find the file format from the record and download it in your gadget.

- Make modifications in your record if required. You are able to full, modify and signal and print out Vermont Summary of Account for Inventory of Business.

Acquire and print out thousands of record themes utilizing the US Legal Forms Internet site, that offers the biggest variety of legitimate forms. Use specialist and status-specific themes to handle your business or individual requirements.