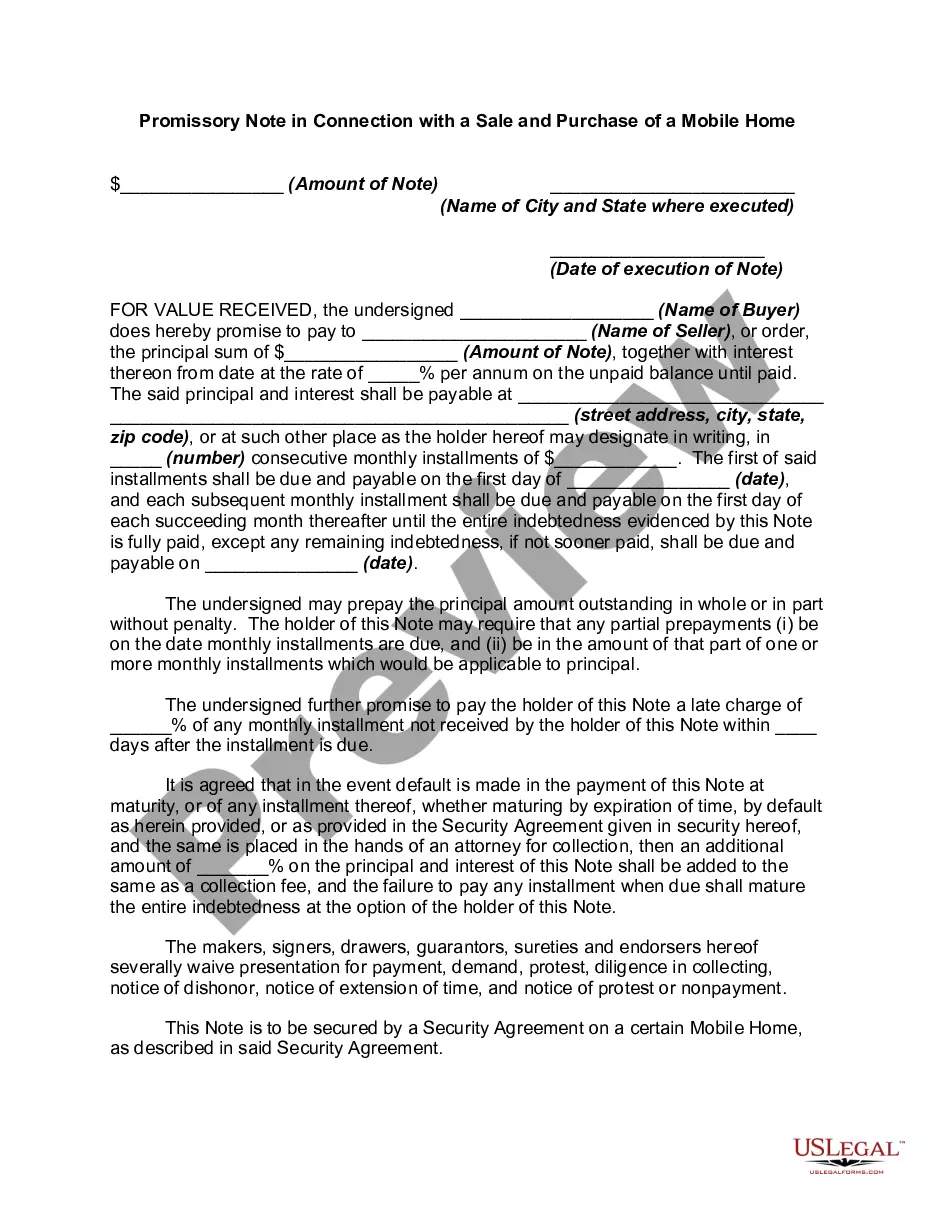

A Vermont Promissory Note in connection with a sale and purchase of a mobile home is a legal document that outlines the terms and conditions of a loan agreement between a buyer and seller. This agreement signifies the buyer's promise to repay the seller a specific amount of money borrowed to complete the purchase of a mobile home. It serves as evidence of the debt and establishes the repayment plan, including interest rates, installment amounts, and any additional provisions. There are different types of Vermont Promissory Notes that can be used in connection with the sale and purchase of a mobile home, such as: 1. Fixed-rate Promissory Note: This type of note establishes a fixed interest rate throughout the loan term, ensuring that the borrower's monthly payments remain consistent. 2. Variable-rate Promissory Note: Unlike a fixed-rate note, this type of note allows for fluctuating interest rates over time, usually tied to an agreed-upon index or market benchmark. Monthly payments may change as the interest rate fluctuates. 3. Secured Promissory Note: This note includes collateral, such as the mobile home itself, which serves as security for the loan. In case of default, the seller has the right to seize the collateral to recover their investment. 4. Unsecured Promissory Note: In contrast to the secured note, this type does not require collateral. The buyer's promise to repay the loan is solely based on their creditworthiness and trustworthiness. 5. Balloon Promissory Note: This note structure allows for smaller monthly payments during the loan term, with a larger "balloon" payment due at the end. This type is suitable for buyers who anticipate a significant increase in their income or intend to refinance the loan at the end of the term. When drafting a Vermont Promissory Note for the sale and purchase of a mobile home, it is important to include key details, such as the names and contact information of the buyer and seller, the mobile home's description, the loan amount, interest rates, repayment terms, and any late payment penalties or prepayment clauses, if applicable. It's crucial to consult with a legal professional or use a trusted template when creating a Vermont Promissory Note to ensure compliance with state laws and protect both parties' interests.

Vermont Promissory Note in Connection with a Sale and Purchase of a Mobile Home

Description

How to fill out Vermont Promissory Note In Connection With A Sale And Purchase Of A Mobile Home?

Choosing the right legitimate record format could be a struggle. Obviously, there are a lot of layouts available on the net, but how will you get the legitimate develop you need? Use the US Legal Forms site. The service provides a large number of layouts, like the Vermont Promissory Note in Connection with a Sale and Purchase of a Mobile Home, which can be used for enterprise and personal needs. All the kinds are inspected by experts and satisfy state and federal needs.

When you are presently listed, log in in your account and click the Acquire switch to have the Vermont Promissory Note in Connection with a Sale and Purchase of a Mobile Home. Utilize your account to appear with the legitimate kinds you possess ordered in the past. Check out the My Forms tab of your account and acquire an additional copy from the record you need.

When you are a fresh consumer of US Legal Forms, allow me to share easy instructions that you can comply with:

- Very first, make certain you have selected the appropriate develop for your area/area. You may check out the shape while using Preview switch and study the shape description to ensure it is the best for you.

- In the event the develop fails to satisfy your requirements, use the Seach area to discover the right develop.

- When you are positive that the shape is suitable, go through the Acquire now switch to have the develop.

- Pick the pricing program you need and enter in the needed information and facts. Make your account and pay for your order with your PayPal account or charge card.

- Choose the submit formatting and download the legitimate record format in your device.

- Complete, change and print out and sign the attained Vermont Promissory Note in Connection with a Sale and Purchase of a Mobile Home.

US Legal Forms is the largest catalogue of legitimate kinds for which you can discover various record layouts. Use the company to download expertly-created paperwork that comply with express needs.