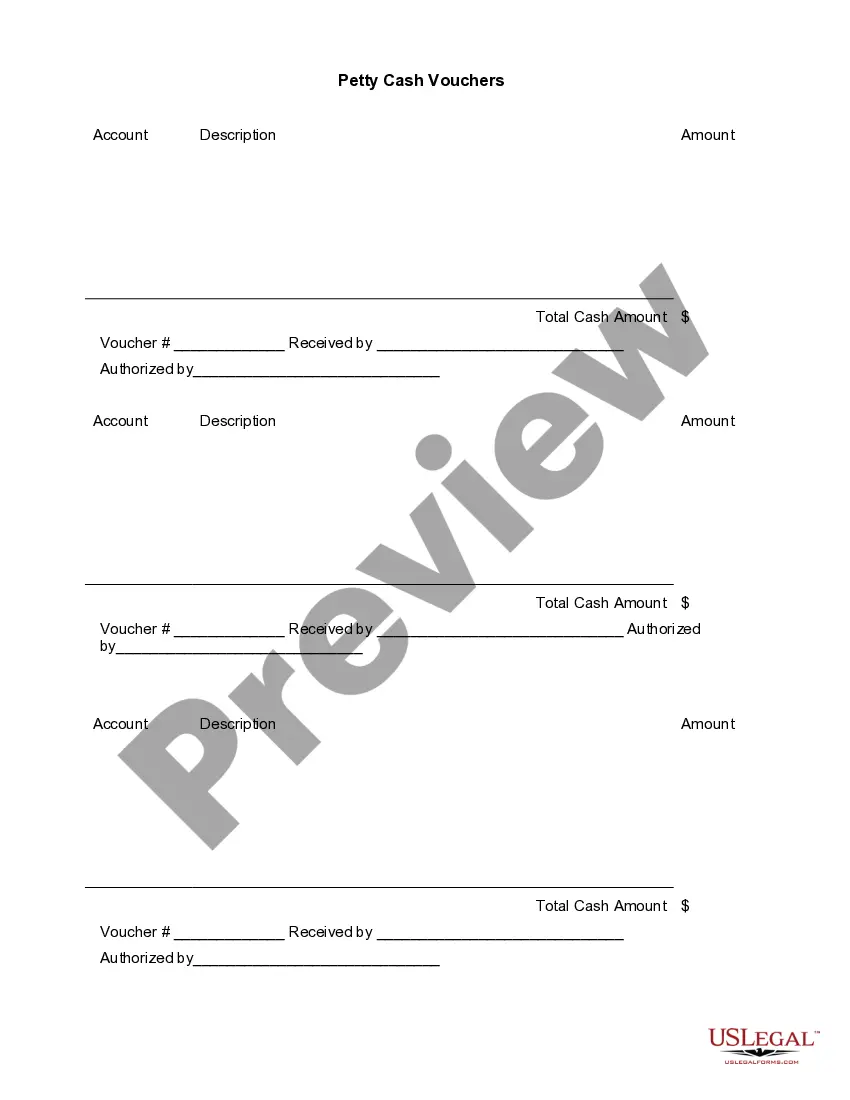

Vermont Petty Cash Journal

Description

How to fill out Petty Cash Journal?

Are you in a situation where you require documents for organizational or personal reasons almost every day.

There are numerous legal document templates available online, but finding reliable ones is challenging.

US Legal Forms offers a vast array of template options, such as the Vermont Petty Cash Journal, designed to comply with federal and state regulations.

Avoid altering or deleting any HTML tags. Only synonymize plain text outside of the HTML tags.

- If you are already acquainted with the US Legal Forms website and possess an account, simply Log In.

- Subsequently, you can download the Vermont Petty Cash Journal template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Locate the template you need and ensure it is relevant to your location/region.

- Utilize the Preview feature to review the document.

- Examine the description to confirm that you have selected the right template.

- If the template does not meet your needs, use the Search field to find one that does.

- Once you find the correct template, click on Purchase now.

- Select the pricing plan you prefer, enter the required information to create your account, and complete your transaction using PayPal or a credit card.

- Choose a convenient file format and download your copy.

- Find all the document templates you have purchased in the My documents section. You can acquire another copy of the Vermont Petty Cash Journal anytime, if needed. Just click the desired template to download or print the document.

- Utilize US Legal Forms, the most extensive collection of legal documents, to save time and avoid errors.

- This service provides well-crafted legal document templates that can be utilized for a variety of purposes.

- Create an account on US Legal Forms and start simplifying your life.

Form popularity

FAQ

Petty cash funds may not be deposited into personal bank accounts or commingled with other funds.Departments may not establish bank accounts for petty cash funds.Purchases of goods and services for more than $100 should not be made with petty cash.Petty cash funds may not be expended for:

The journal entry that needs to be recorded is a debit (increase) to the petty cash fund and a credit (decrease) to the business checking account. Withdrawals made to the petty cash fund will be recorded as expenses.

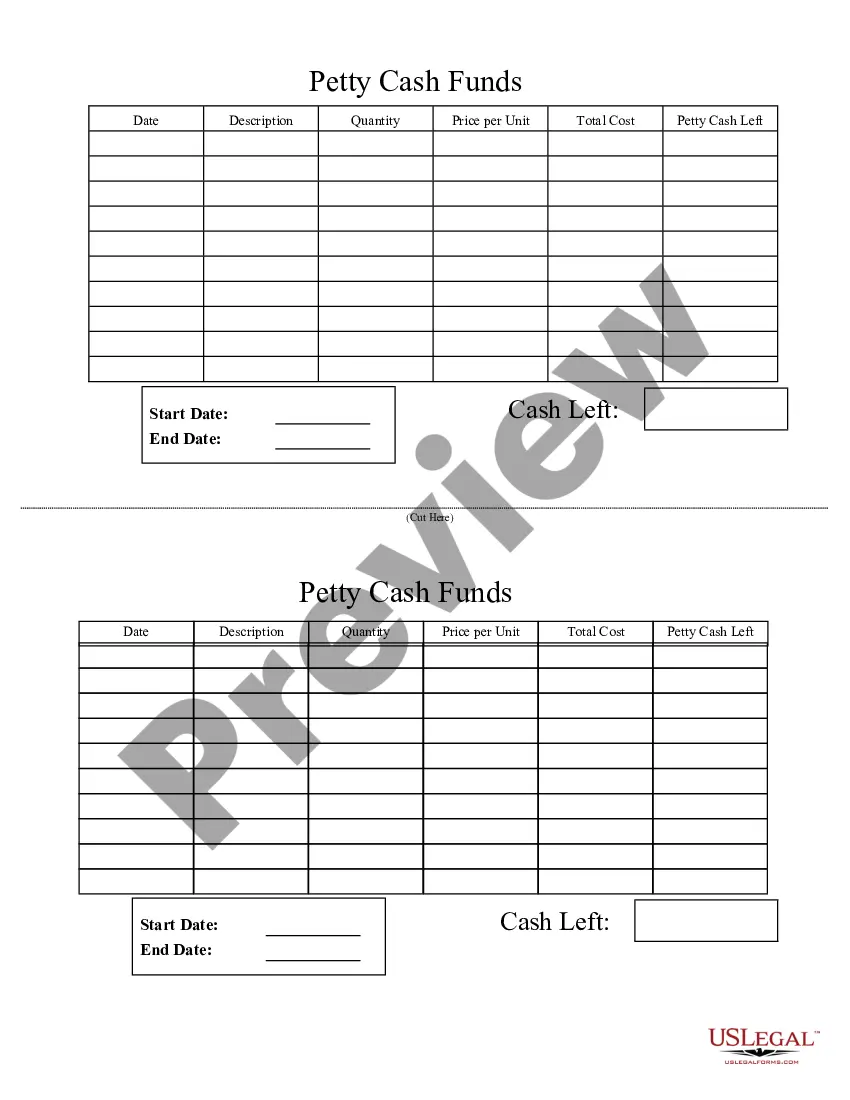

The procedure for petty cash funding is outlined below:Complete reconciliation form. Complete a petty cash reconciliation form, in which the petty cash custodian lists the remaining cash on hand, vouchers issued, and any overage or underage.Obtain cash.Add cash to petty cash fund.Record vouchers in general ledger.

The journal entry that needs to be recorded is a debit (increase) to the petty cash fund and a credit (decrease) to the business checking account. Withdrawals made to the petty cash fund will be recorded as expenses.

Petty cash provides convenience for small transactions for which issuing a check or a corporate credit card is unreasonable or unacceptable. The small amount of cash that a company considers petty will vary, with many companies keeping between $100 and $500 as a petty cash fund.

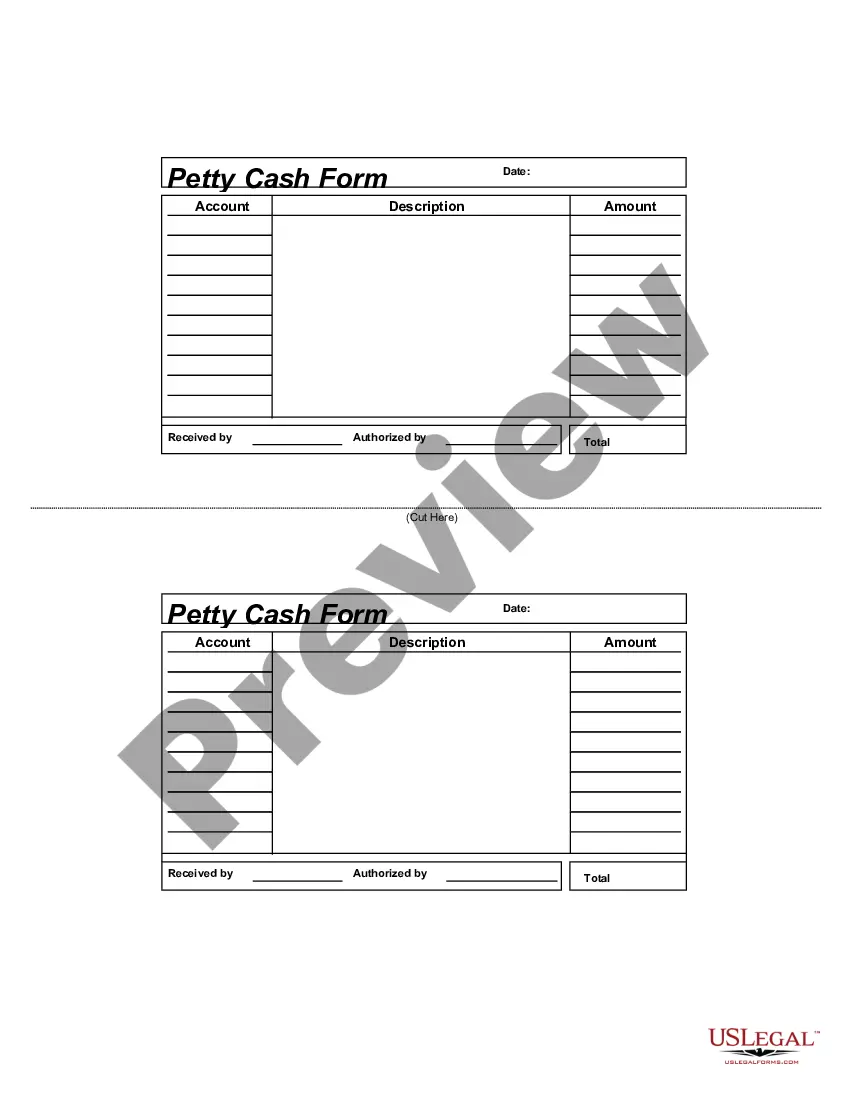

The petty cash journal entry is a debit to the petty cash account and a credit to the cash account. The petty cash custodian refills the petty cash drawer or box, which should now contain the original amount of cash that was designated for the fund. The cashier creates a journal entry to record the petty cash receipts.

Petty cash appears within the current assets section of the balance sheet. This is because line items in the balance sheet are sorted in their order of liquidity. Since petty cash is highly liquid, it appears near the top of the balance sheet.

When a petty cash fund is in use, petty cash transactions are still recorded on financial statements. No accounting journal entries are made when purchases are made using petty cash, it's only when the custodian needs more cashand in exchange for the receipts, receives new fundsthat the journal entries are recorded.

A petty cash account is an imprest account, so it is only debited when the fund is initially established or increased in amount. Transactions to replenish the account involve a debit to the expenses and a credit to the cash account (e.g., bank account).

The petty cash journal contains a summarization of the payments from a petty cash fund. The totals in the journal are then used as the basis for a journal entry into a company's general ledger. This journal entry lists petty cash expenditures by expense type.