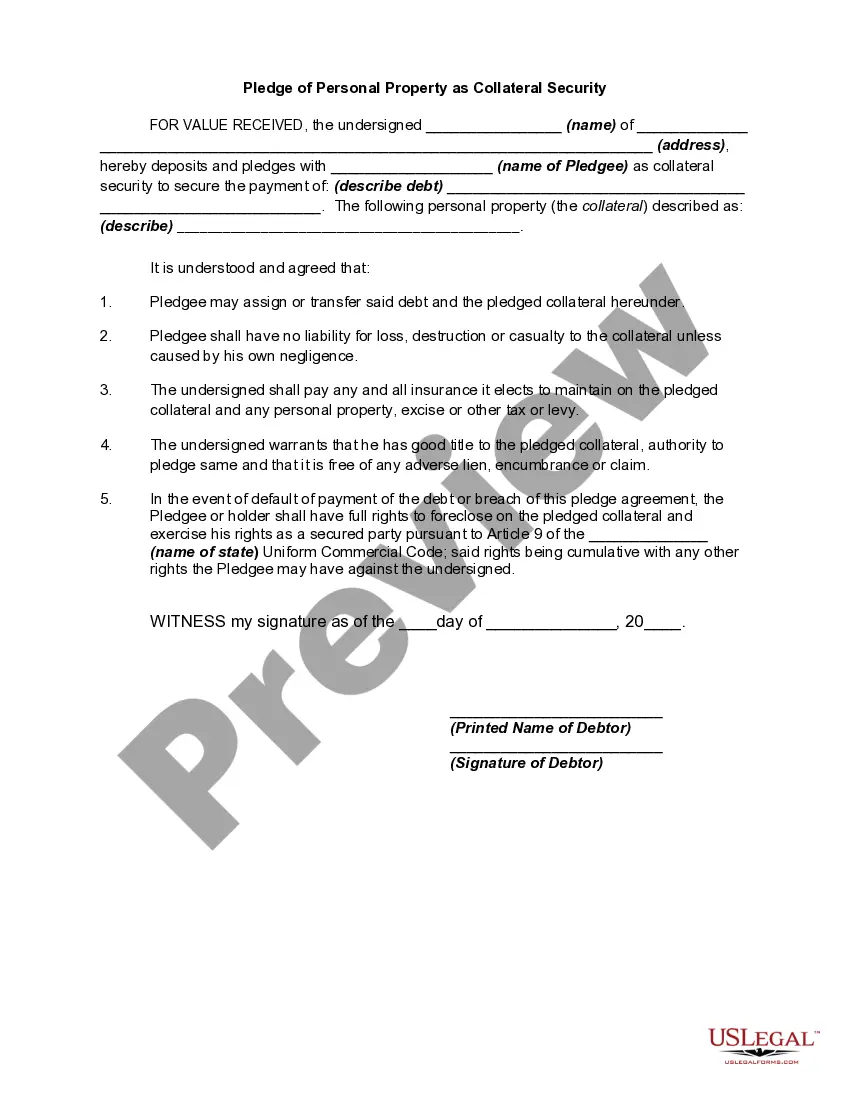

The Vermont Pledge of Personal Property as Collateral Security is a legal mechanism that allows individuals or businesses in Vermont to use their personal property as collateral for a loan or debt. This pledge is a way of securing a creditor's interest in the borrower's personal assets, providing assurance and protection in case the borrower defaults on their obligations. Under Vermont law, the pledge of personal property as collateral security is regulated by the Vermont Uniform Commercial Code (UCC) Article 9. This code establishes the rules and procedures for creating, perfecting, and enforcing the pledge. The Vermont Pledge of Personal Property can be used for various types of personal property assets, including but not limited to vehicles, equipment, inventory, accounts receivable, intellectual property, and investment securities. By pledging these assets, borrowers can obtain loans or credit facilities with more favorable terms, lower interest rates, and higher borrowing limits compared to unsecured loans. There are different types of Vermont Pledge of Personal Property as Collateral Security, depending on the nature of the assets being pledged. Some common types include: 1. Inventory Pledge: This type of pledge allows borrowers to use their inventory as collateral. It is commonly used by businesses that rely heavily on stock or goods for their operations. 2. Equipment Pledge: Borrowers can pledge their equipment, machinery, or other tangible assets used for business purposes as collateral security. This type of pledge is particularly relevant to construction companies, manufacturers, and other equipment-intensive industries. 3. Accounts Receivable Pledge: Businesses with substantial accounts receivable can pledge these assets as collateral. Accounts receivable represent money owed to the borrower by their customers, which can be used as security for a loan. 4. Intellectual Property Pledge: Borrowers may pledge their intellectual property, such as trademarks, copyrights, or patents, as collateral security. This type of pledge is relevant for individuals or businesses that hold valuable intellectual assets. 5. Securities Pledge: Investors or borrowers who possess investment securities, such as stocks, bonds, or mutual funds, may pledge these assets as collateral. This type of pledge can be useful when seeking financing for investment activities or borrowing against the value of these securities. It is important for borrowers to understand the legal implications and obligations associated with the Vermont Pledge of Personal Property as Collateral Security. It is advised to consult legal professionals or financial advisors to ensure compliance with the requirements of the Vermont Uniform Commercial Code and to safeguard their rights and interests.

Vermont Pledge of Personal Property as Collateral Security

Description

How to fill out Vermont Pledge Of Personal Property As Collateral Security?

If you need to full, obtain, or produce legal file web templates, use US Legal Forms, the most important assortment of legal varieties, which can be found on-line. Utilize the site`s simple and hassle-free search to obtain the paperwork you want. Different web templates for organization and individual uses are sorted by groups and says, or keywords and phrases. Use US Legal Forms to obtain the Vermont Pledge of Personal Property as Collateral Security within a couple of clicks.

If you are previously a US Legal Forms client, log in to your account and then click the Down load key to get the Vermont Pledge of Personal Property as Collateral Security. You may also accessibility varieties you previously delivered electronically within the My Forms tab of your account.

If you are using US Legal Forms the very first time, refer to the instructions under:

- Step 1. Make sure you have selected the form for your correct metropolis/region.

- Step 2. Utilize the Review solution to look through the form`s content. Don`t forget about to learn the explanation.

- Step 3. If you are not satisfied with the kind, take advantage of the Search industry near the top of the display to find other types in the legal kind design.

- Step 4. When you have identified the form you want, select the Get now key. Pick the rates plan you prefer and add your accreditations to register for the account.

- Step 5. Process the transaction. You can use your Мisa or Ьastercard or PayPal account to accomplish the transaction.

- Step 6. Choose the file format in the legal kind and obtain it on the system.

- Step 7. Comprehensive, change and produce or indicator the Vermont Pledge of Personal Property as Collateral Security.

Every single legal file design you purchase is your own forever. You might have acces to every kind you delivered electronically inside your acccount. Select the My Forms section and decide on a kind to produce or obtain once more.

Compete and obtain, and produce the Vermont Pledge of Personal Property as Collateral Security with US Legal Forms. There are many professional and condition-certain varieties you may use to your organization or individual requirements.