Vermont Loan Guaranty Agreement

Description

How to fill out Loan Guaranty Agreement?

Are you presently within a place that you need papers for either business or personal uses just about every time? There are tons of legal file themes available on the net, but getting kinds you can rely isn`t straightforward. US Legal Forms gives thousands of form themes, much like the Vermont Loan Guaranty Agreement, which can be composed to fulfill state and federal demands.

In case you are currently knowledgeable about US Legal Forms site and get an account, basically log in. Afterward, you may obtain the Vermont Loan Guaranty Agreement format.

Should you not come with an account and would like to begin using US Legal Forms, follow these steps:

- Discover the form you will need and make sure it is for that appropriate metropolis/region.

- Use the Review option to examine the form.

- Look at the description to ensure that you have selected the proper form.

- If the form isn`t what you are seeking, utilize the Lookup field to discover the form that meets your needs and demands.

- If you discover the appropriate form, simply click Buy now.

- Pick the prices program you need, fill in the desired info to make your bank account, and buy the transaction utilizing your PayPal or Visa or Mastercard.

- Pick a hassle-free paper formatting and obtain your duplicate.

Locate all of the file themes you possess purchased in the My Forms menus. You can get a more duplicate of Vermont Loan Guaranty Agreement whenever, if necessary. Just click the needed form to obtain or produce the file format.

Use US Legal Forms, probably the most extensive collection of legal varieties, in order to save efforts and prevent faults. The services gives skillfully made legal file themes that can be used for a variety of uses. Generate an account on US Legal Forms and start producing your way of life a little easier.

Form popularity

FAQ

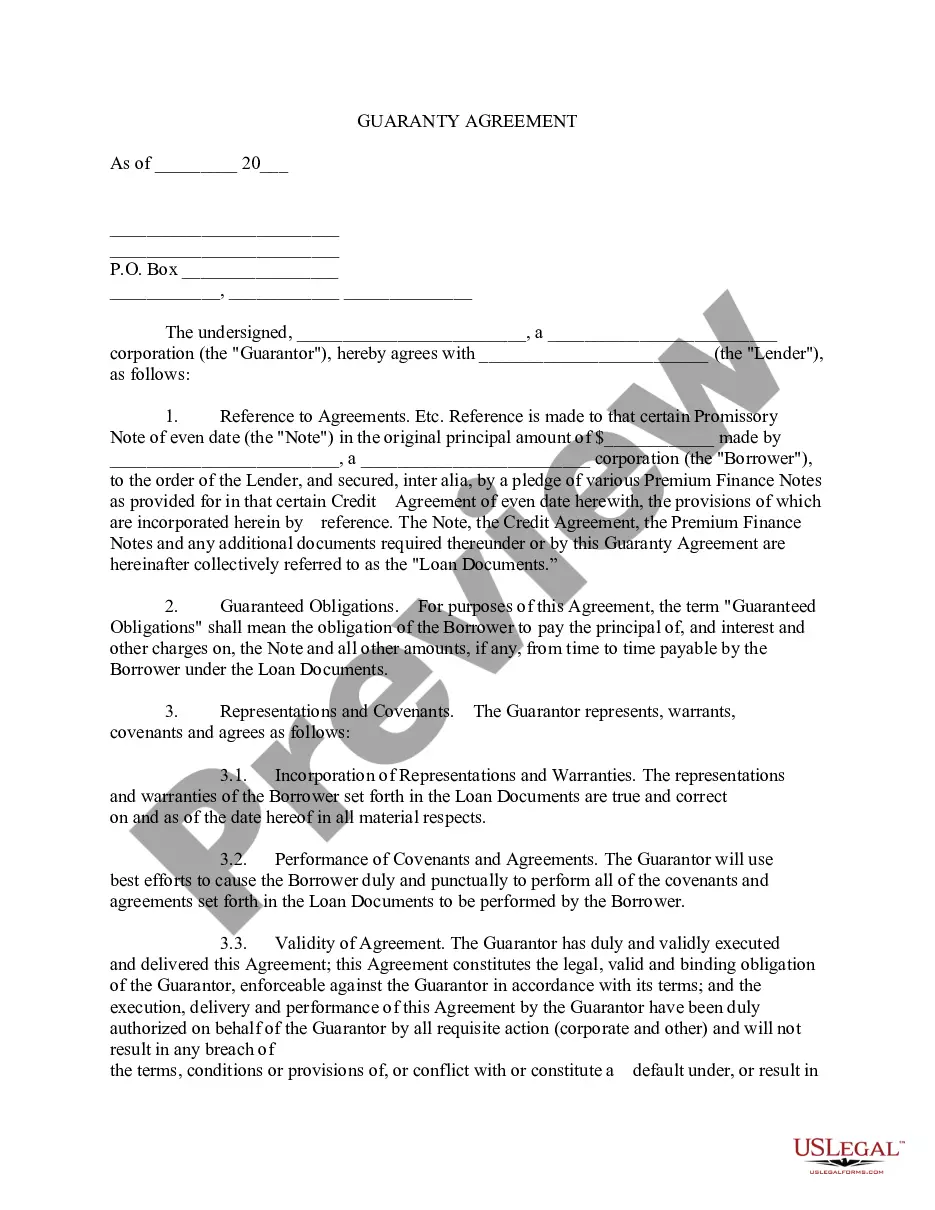

A loan guarantee, in finance, is a promise by one party (the guarantor) to assume the debt obligation of a borrower if that borrower defaults. A guarantee can be limited or unlimited, making the guarantor liable for only a portion or all of the debt.

Traditionally, a distinction is made between: Real guarantees relating to assets having an intrinsic value. Personal guarantees involving a debt obligation for one or more people. Moral guarantees that do not provide the lender with any real legal security.

The Vermont False Claims Act (the ?VFCA?) makes it unlawful for any person to: (1) knowingly present or cause to be presented a false or fraudulent claim for payment or approval; (2) knowingly make, us, or cause to be made or used a false record or statement material to a false or fraudulent claim; (3) knowingly ...

Vermont's 6-year statute of limitations period applies to bribery, embezzlement, forgery, fraud, and felony tax charges. Most other felonies and misdemeanors carry a 3-year statute of limitations. Individual crimes may have their own statute of limitations period.

Vermont's Statute of Limitations on Debt The State of Vermont has a six-to-eight-year statute of limitations on written contracts, while oral contracts and collection of debt on accounts each have a six year statute of limitations. Judgements carry an eight-year statute of limitations.

Vermont Interest Rate Laws When considering a personal loans in Vermont, the statutory interest rate for these types of unsecured, consumer loans is 12 percent. This is the maximum interest that can be charged on any personal, consumer loan in the State of Vermont.