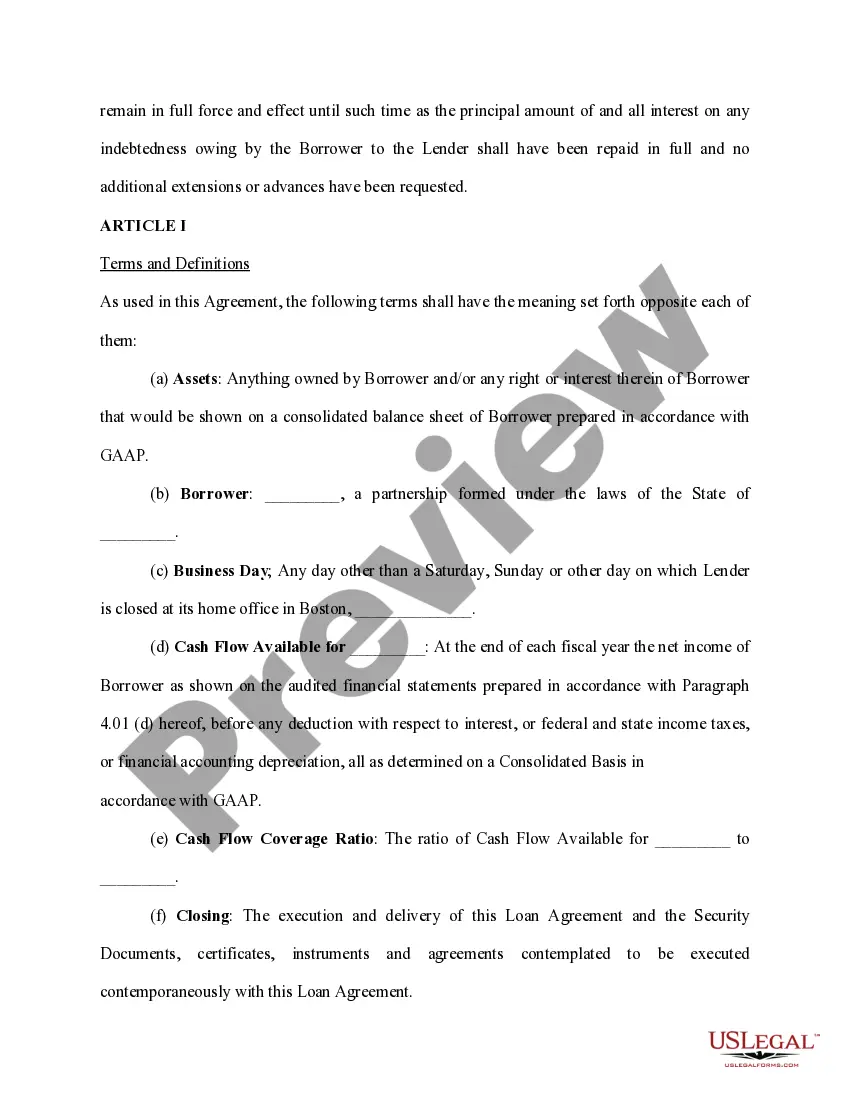

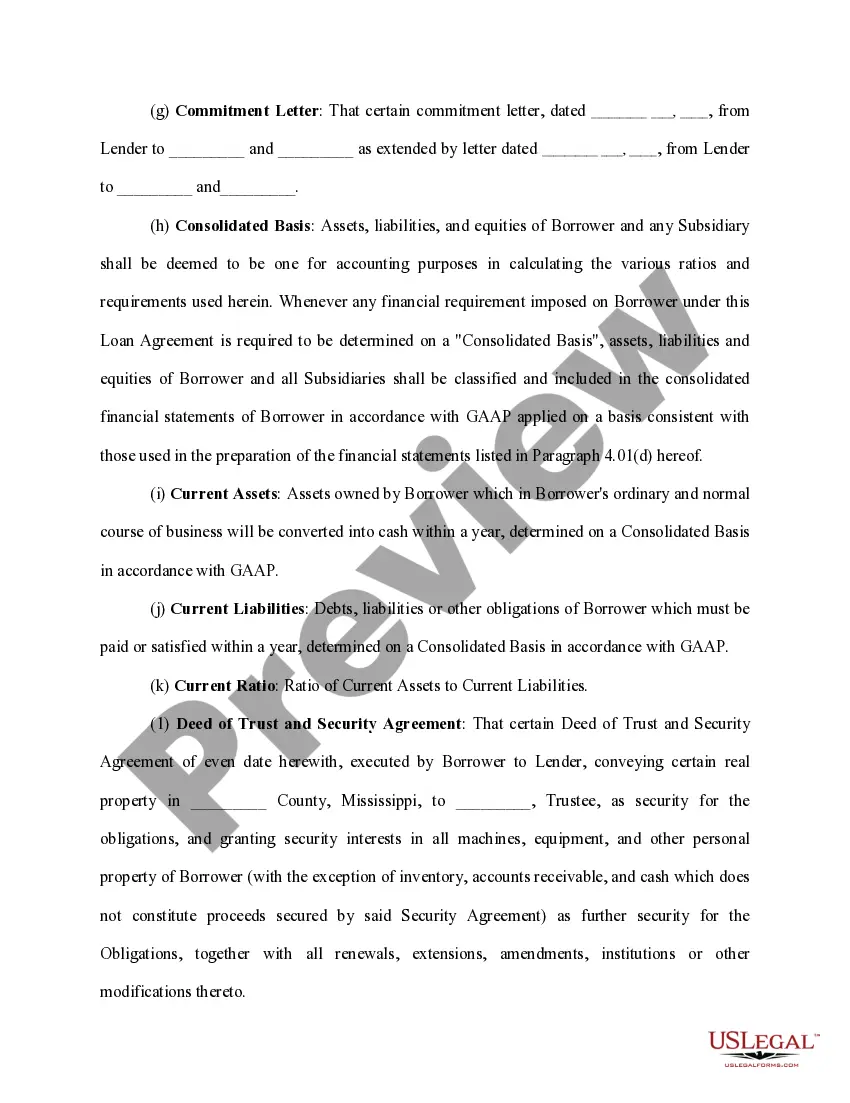

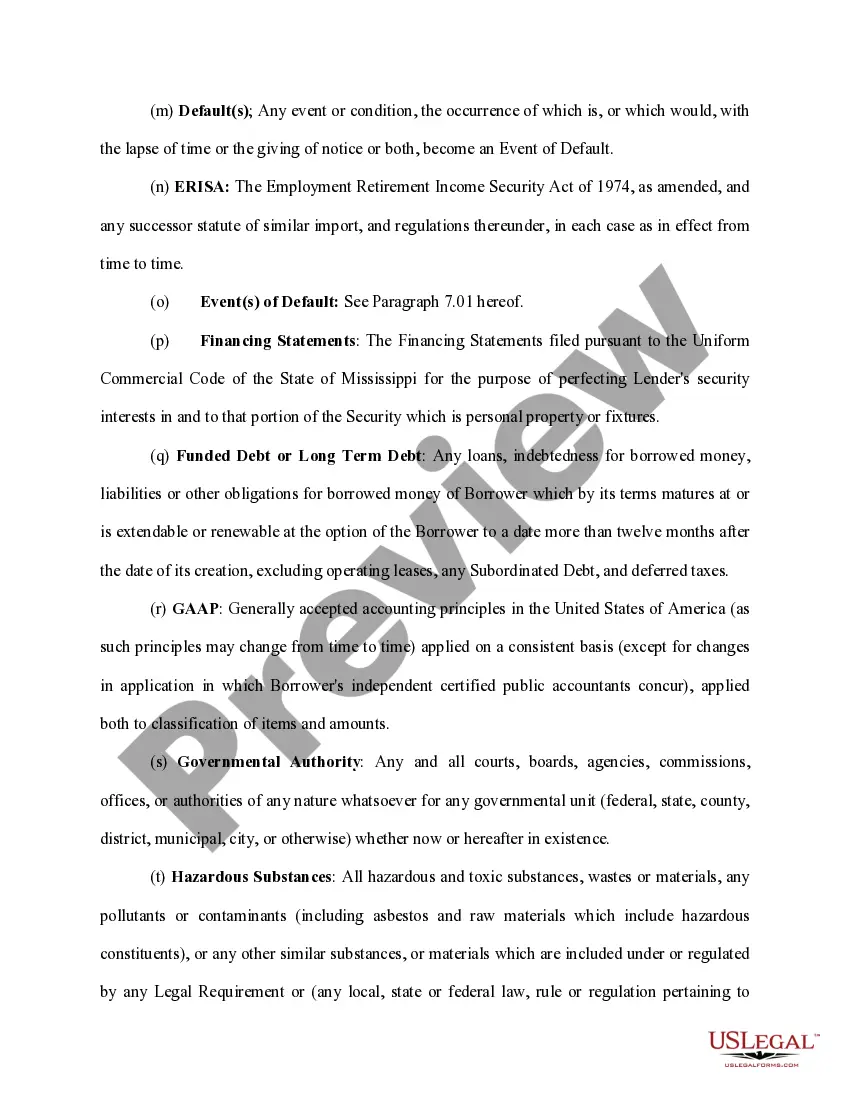

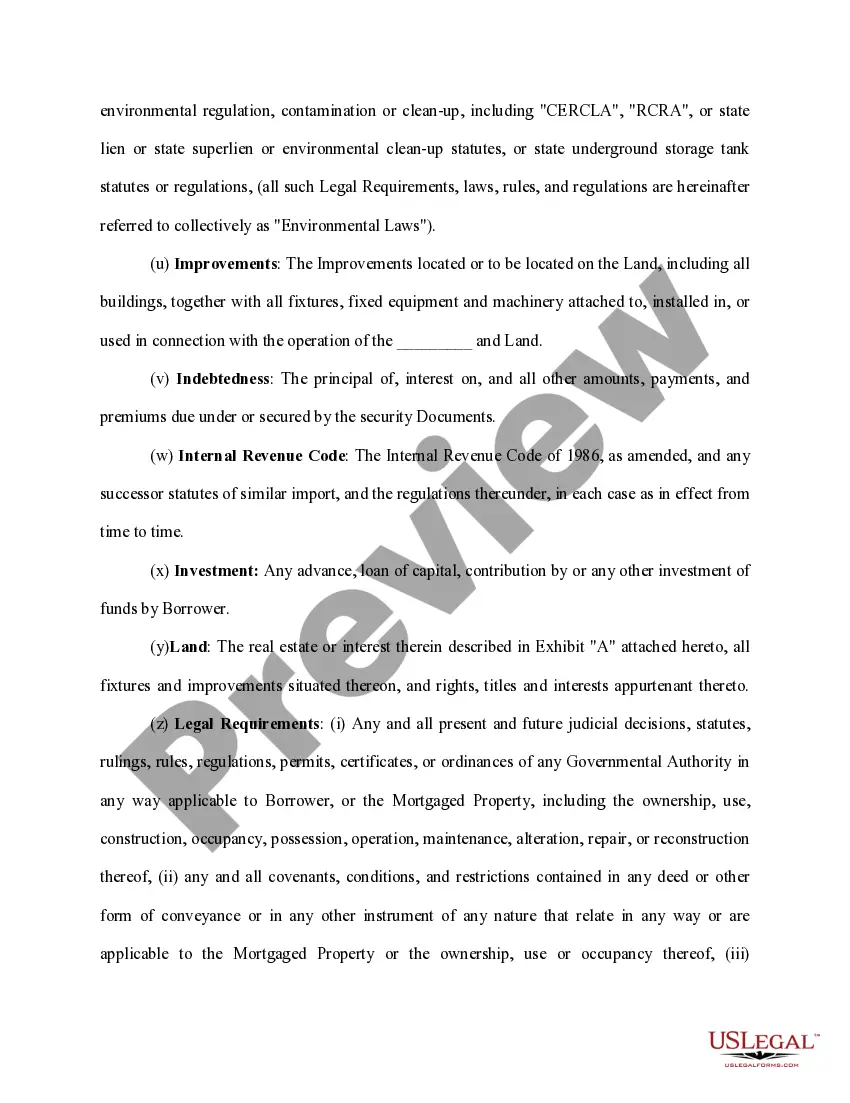

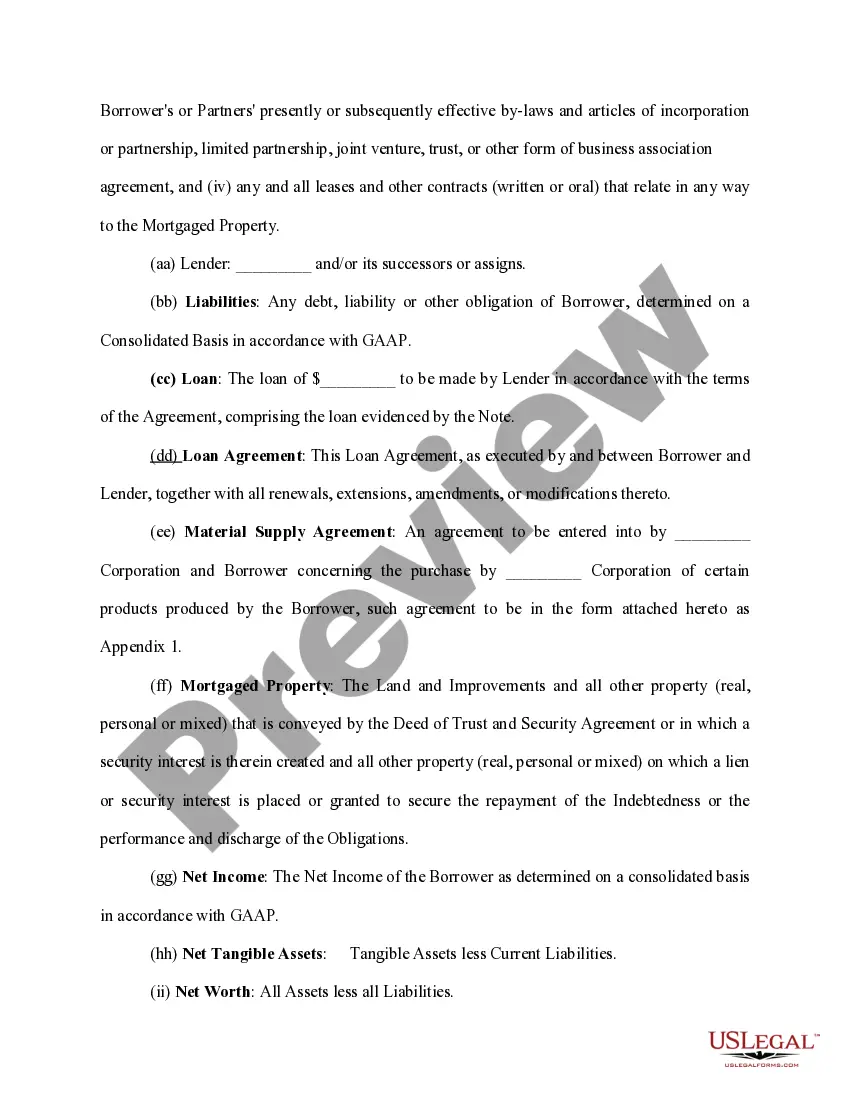

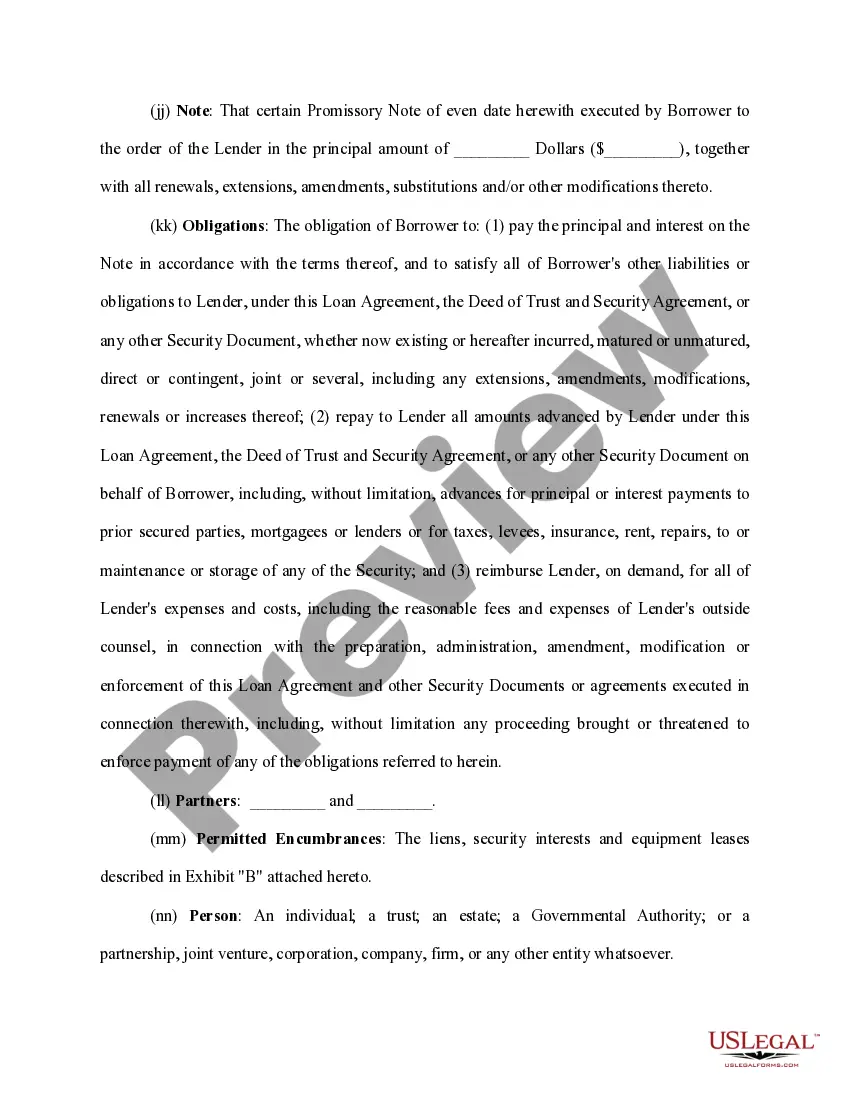

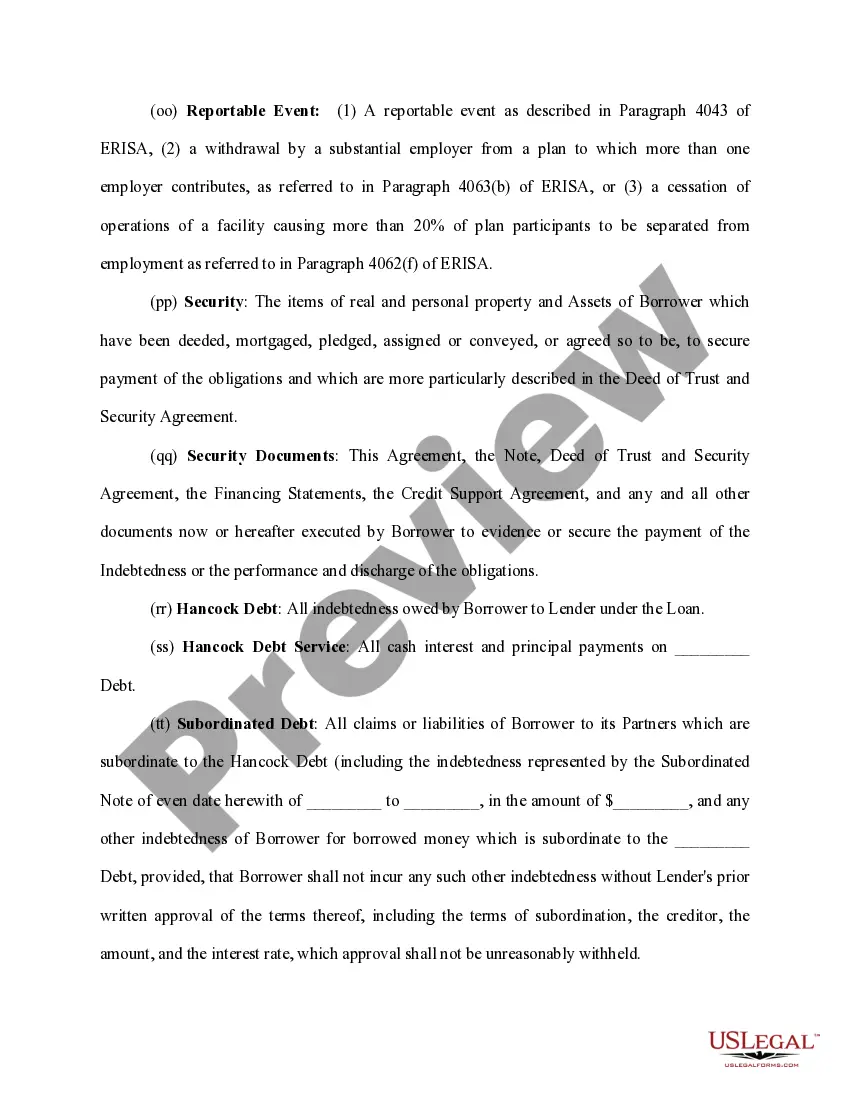

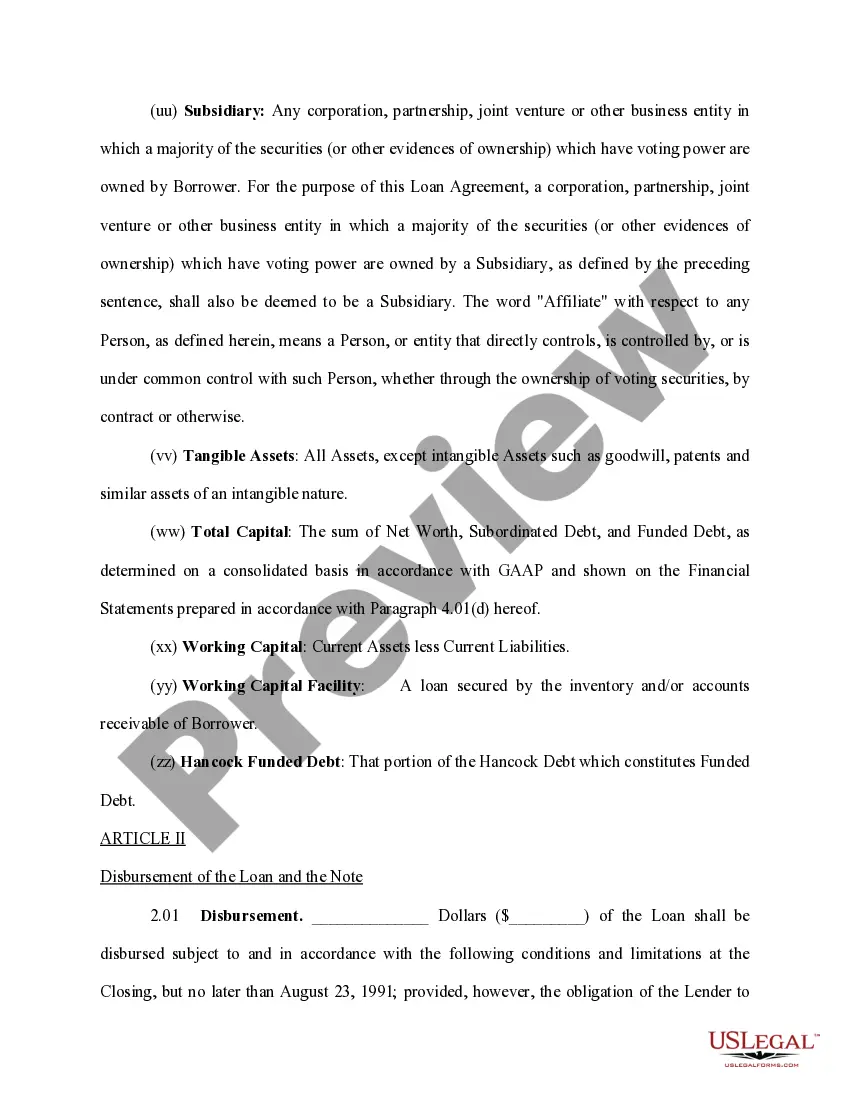

A Vermont Loan Agreement for Business is a legally binding contract that outlines the terms and conditions under which a borrower receives a loan from a lender in the state of Vermont. This agreement serves as a protection for both parties involved in the loan transaction. Keywords: Vermont, Loan Agreement, Business, terms and conditions, borrower, lender, protection, transaction There are several types of loan agreements that can be utilized in Vermont for various business purposes: 1. General Business Loan Agreement: This type of agreement is the most common and is used for general business financing needs. It outlines the loan amount, interest rate, repayment terms, and any collateral provided by the borrower to secure the loan. 2. Equipment Loan Agreement: In this agreement, the lender provides a loan specifically for purchasing or leasing equipment required for the borrower's business operations. The agreement specifies the equipment details, loan amount, repayment schedule, and any warranties or maintenance responsibilities. 3. Commercial Real Estate Loan Agreement: When businesses need funds for purchasing or refinancing commercial properties, this agreement comes into play. It details the loan amount, interest rate, repayment terms, and the property's title and deed information. 4. Working Capital Loan Agreement: This type of agreement is suitable for businesses requiring funds to cover day-to-day operations and expenses. It lays out the loan amount, repayment terms, interest rate, and how the funds will be used. 5. Line of Credit Agreement: A line of credit provides businesses with access to a certain amount of funds that they can borrow as needed. This agreement establishes the maximum credit limit, interest rate, draw period, and repayment schedule. Regardless of the type of Vermont Loan Agreement for Business, it is crucial for both parties to thoroughly review and understand all terms and conditions before signing. This document sets the expectations and obligations of both the borrower and the lender, ensuring a transparent and legally compliant loan transaction. In conclusion, a Vermont Loan Agreement for Business is an essential document when borrowing funds for various business purposes. From general business loans to equipment financing and commercial real estate, these agreements define the terms and conditions to protect the interests of both the borrower and the lender.

Vermont Loan Agreement for Business

Description

How to fill out Vermont Loan Agreement For Business?

You are able to spend hrs on the Internet trying to find the legal document web template which fits the federal and state needs you want. US Legal Forms provides a huge number of legal varieties which can be evaluated by professionals. It is simple to acquire or produce the Vermont Loan Agreement for Business from our services.

If you already possess a US Legal Forms account, it is possible to log in and click the Download button. Following that, it is possible to full, edit, produce, or sign the Vermont Loan Agreement for Business. Every legal document web template you purchase is your own forever. To have an additional duplicate of the acquired type, check out the My Forms tab and click the corresponding button.

If you use the US Legal Forms site the very first time, adhere to the simple recommendations under:

- Initially, make certain you have chosen the correct document web template to the region/town of your liking. Look at the type information to make sure you have chosen the appropriate type. If accessible, use the Review button to search through the document web template as well.

- In order to locate an additional model from the type, use the Search industry to get the web template that fits your needs and needs.

- After you have identified the web template you need, click on Acquire now to carry on.

- Choose the costs program you need, enter your accreditations, and register for a merchant account on US Legal Forms.

- Comprehensive the deal. You may use your credit card or PayPal account to cover the legal type.

- Choose the format from the document and acquire it to the device.

- Make changes to the document if possible. You are able to full, edit and sign and produce Vermont Loan Agreement for Business.

Download and produce a huge number of document web templates using the US Legal Forms web site, that provides the most important selection of legal varieties. Use professional and status-specific web templates to tackle your company or individual demands.