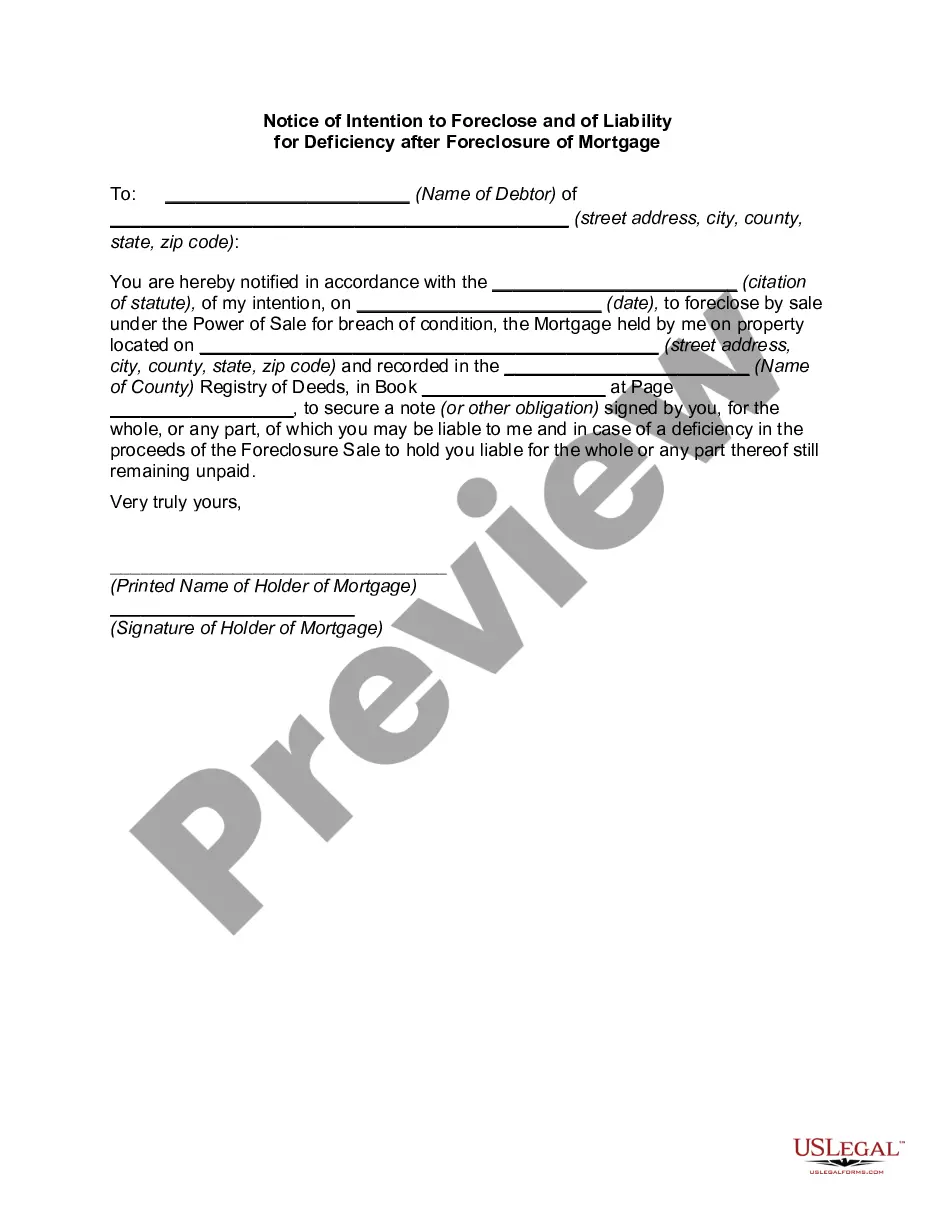

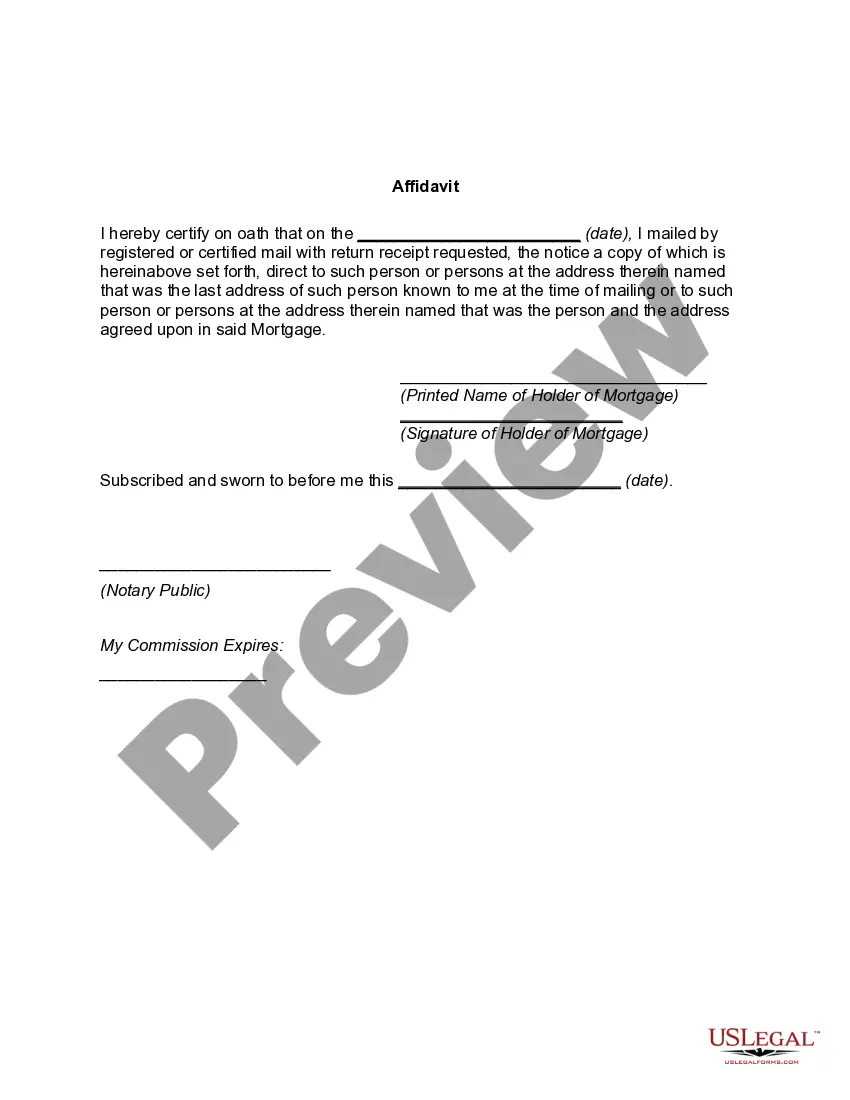

The Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is an important legal document that plays a crucial role in the foreclosure process. It outlines the intentions of the lender to initiate foreclosure proceedings on a property and informs the borrower of the potential liability for any deficiency after the foreclosure sale. In Vermont, there are several types of Notice of Intention to Foreclose, each serving a specific purpose. These include: 1. Notice of Intention to Foreclose: This notice is typically sent by the lender to the borrower when the borrower is in default on their mortgage payments. It informs the borrower of the lender's intention to foreclose on the property if the outstanding payments are not brought up to date within a certain timeframe. 2. Notice of Acceleration and Intention to Foreclose: This notice is sent when the lender decides to accelerate the due date of the entire mortgage debt. It informs the borrower that the entire outstanding balance of the mortgage is due immediately and that failure to pay within the specified period will result in foreclosure proceedings. 3. Notice of Intention to Foreclose and of Liability for Deficiency: This notice serves the purpose of informing the borrower not only about the intention to foreclose but also about the potential liability for any deficiency after the foreclosure sale. In Vermont, if the foreclosure sale does not generate enough funds to cover the outstanding mortgage debt, the lender can pursue the borrower for the deficiency amount. Liability for deficiency after foreclosure refers to the borrower's responsibility for the difference between the outstanding mortgage debt and the amount obtained through the foreclosure sale. It is crucial for borrowers in Vermont to understand the potential liability for deficiency as it may have significant financial implications. The Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage should include key information such as the borrower's name, property address, the outstanding mortgage balance, the date of default, the lender's contact information, and the action required by the borrower to avoid foreclosure, if applicable. In conclusion, the Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage serves as an official communication between the lender and the borrower regarding the foreclosure process and the potential liability for deficiency. It is crucial for borrowers to carefully review and understand the implications of these notices to effectively navigate the foreclosure process and protect their interests.

Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Vermont Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

You can invest hrs online looking for the legal record template that meets the state and federal needs you require. US Legal Forms supplies 1000s of legal types that happen to be examined by specialists. You can actually obtain or produce the Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage from my support.

If you have a US Legal Forms bank account, you can log in and click on the Obtain switch. Next, you can comprehensive, revise, produce, or sign the Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. Every single legal record template you purchase is the one you have for a long time. To acquire yet another copy associated with a obtained develop, check out the My Forms tab and click on the related switch.

Should you use the US Legal Forms site initially, adhere to the straightforward guidelines listed below:

- Very first, make certain you have selected the best record template for that state/metropolis of your choice. See the develop explanation to make sure you have picked out the correct develop. If accessible, utilize the Preview switch to look through the record template as well.

- If you want to find yet another version of your develop, utilize the Research field to get the template that meets your needs and needs.

- When you have discovered the template you desire, click on Acquire now to carry on.

- Pick the prices strategy you desire, key in your qualifications, and sign up for a merchant account on US Legal Forms.

- Total the purchase. You can utilize your credit card or PayPal bank account to cover the legal develop.

- Pick the structure of your record and obtain it for your device.

- Make changes for your record if required. You can comprehensive, revise and sign and produce Vermont Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

Obtain and produce 1000s of record themes making use of the US Legal Forms site, that provides the most important assortment of legal types. Use professional and status-particular themes to handle your organization or specific requires.

Form popularity

FAQ

The right of redemption allows individuals who have defaulted on their mortgages the ability to reclaim their property by paying the amount due (plus interest and penalties) before the foreclosure process begins, or, in some states, even after a foreclosure sale (for the foreclosure price, plus interest and penalties).

During the initial ninety days of foreclosure of a deed of trust, the Trustor can either pay back the loan entirely or renegotiate with the Beneficiary. This will stop the entire foreclosure process. After ninety days, however, the right to force the sale to stop is limited.

In Vermont, lenders can use a judicial or strict foreclosure process to foreclose on Vermont-based property. Either way, the lender has to file a lawsuit in state court. Vermont law allows strict foreclosures if the value of the property is less than the debt amount.

Redemption Period In most cases, it is about six months. If the property being foreclosed is not your primary residence, the court may give you less than six months. To redeem your property, you can pay the full amount that you owe the bank and avoid a foreclosure sale.

21 days later, the property can be sold If no one else bids, your home goes to the lender. The successful bidder gets a trustee's deed once the sale is complete. You have up until 5 days before the foreclosure sale to stop the process. This is called ?reinstatement? of the loan.

Vermont's 6-year statute of limitations period applies to bribery, embezzlement, forgery, fraud, and felony tax charges. Most other felonies and misdemeanors carry a 3-year statute of limitations. Individual crimes may have their own statute of limitations period.

Although the statute of limitations for property damage under Vermont law is three years after the cause of action accrues, no Vermont court has found a two-year suit limitation provision in an insurance contract offering coverage for property damage unreasonable or contrary to public policy?.