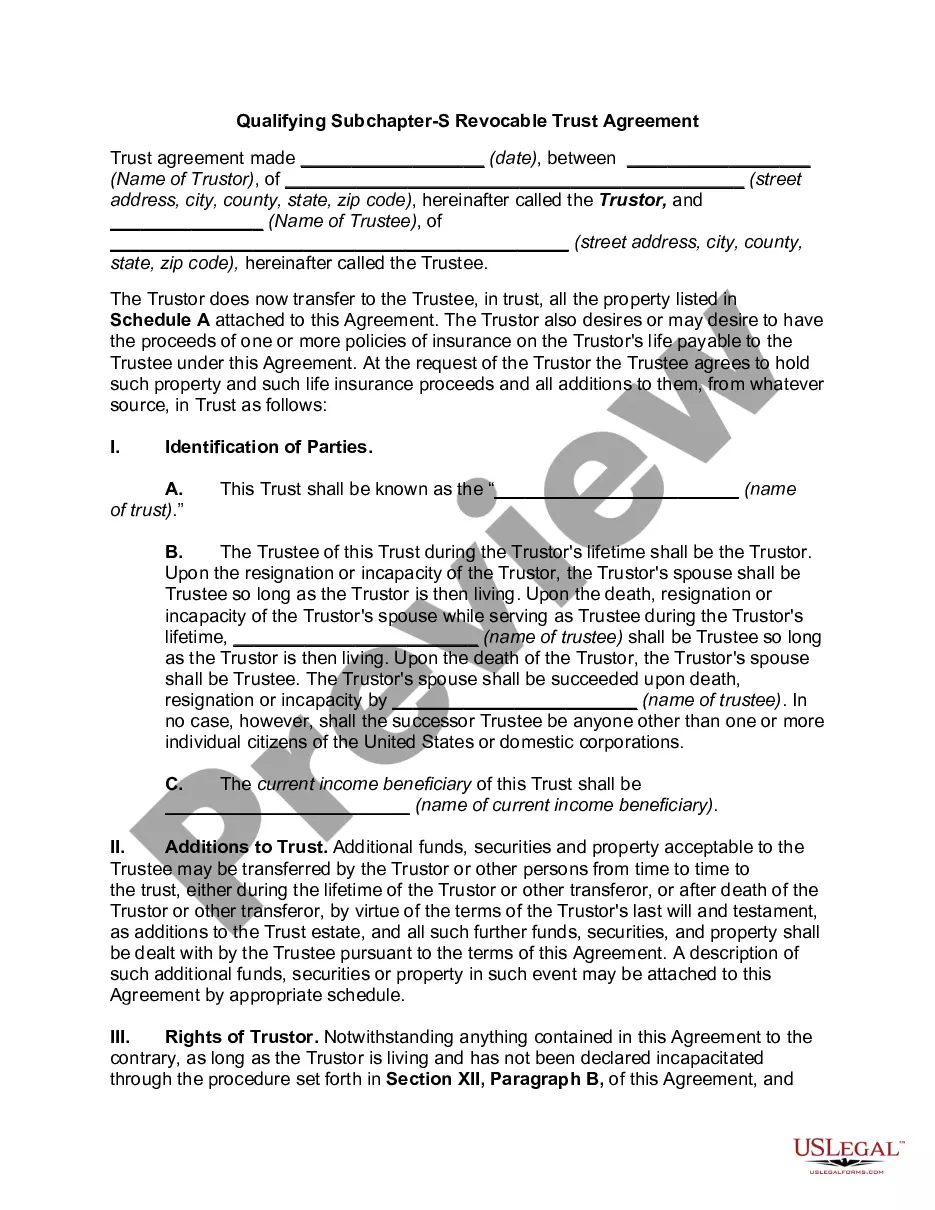

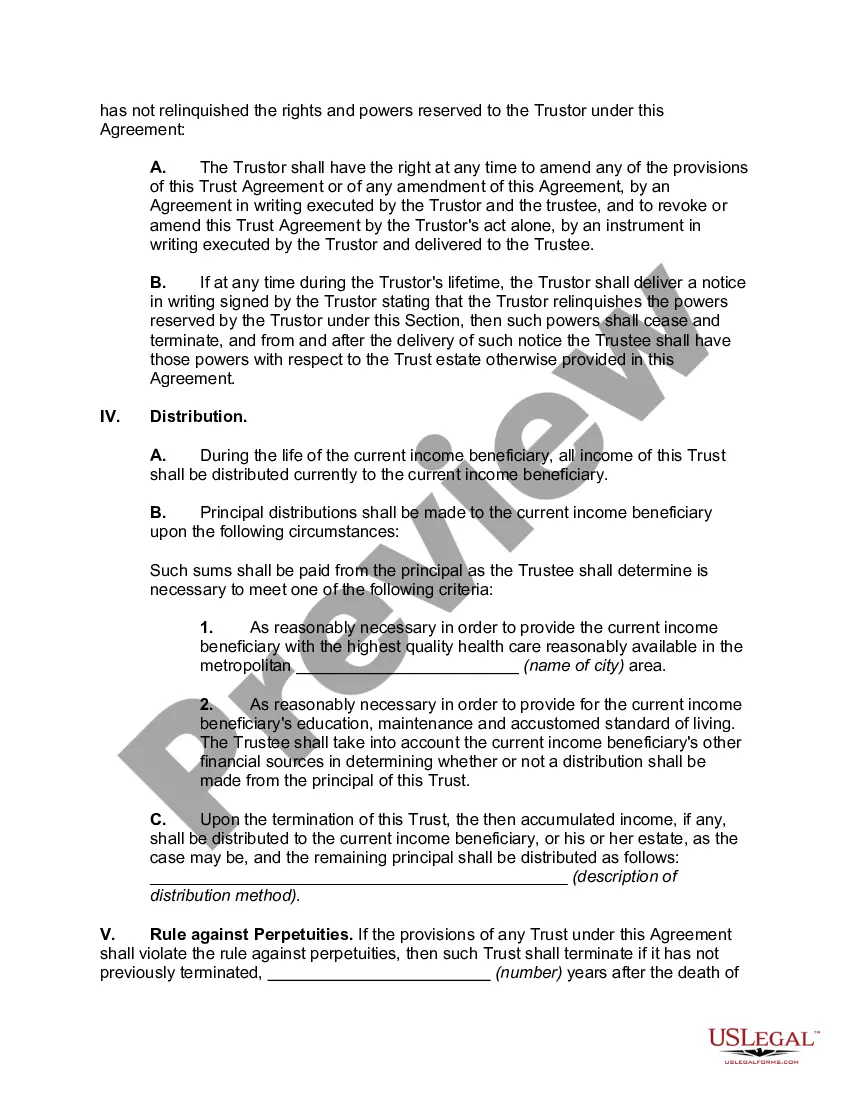

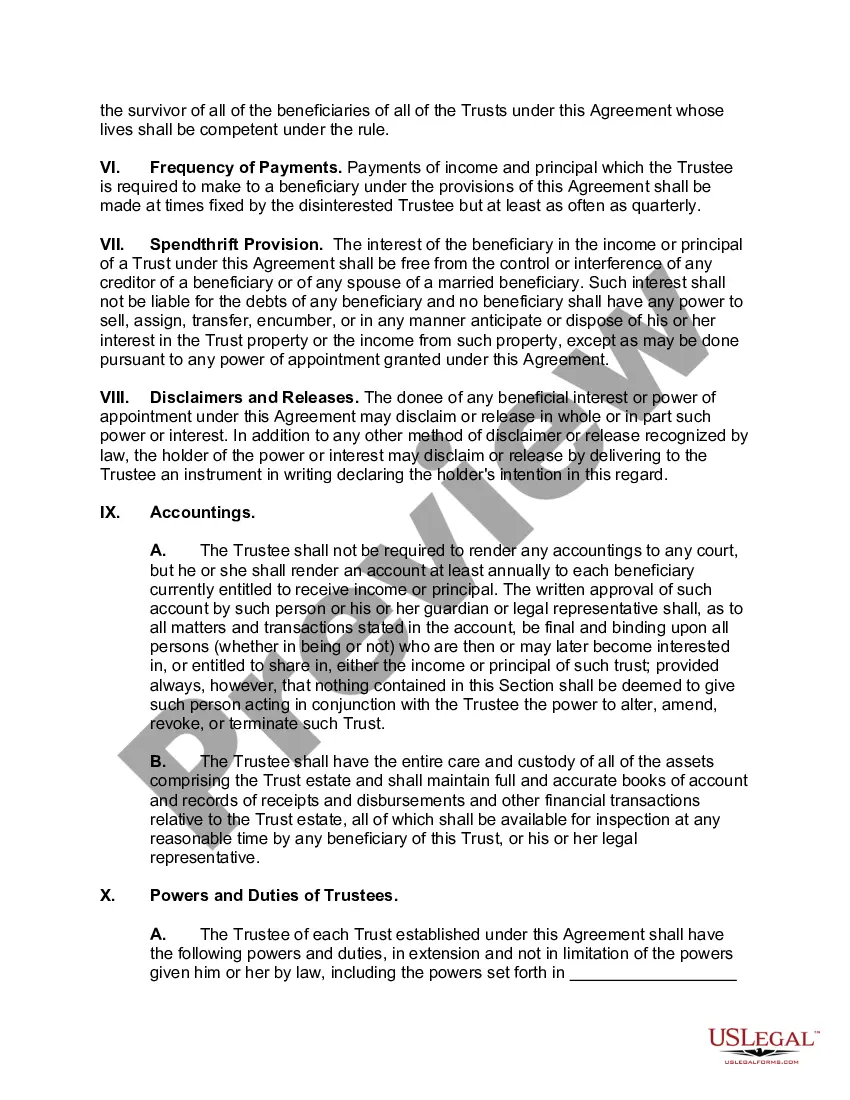

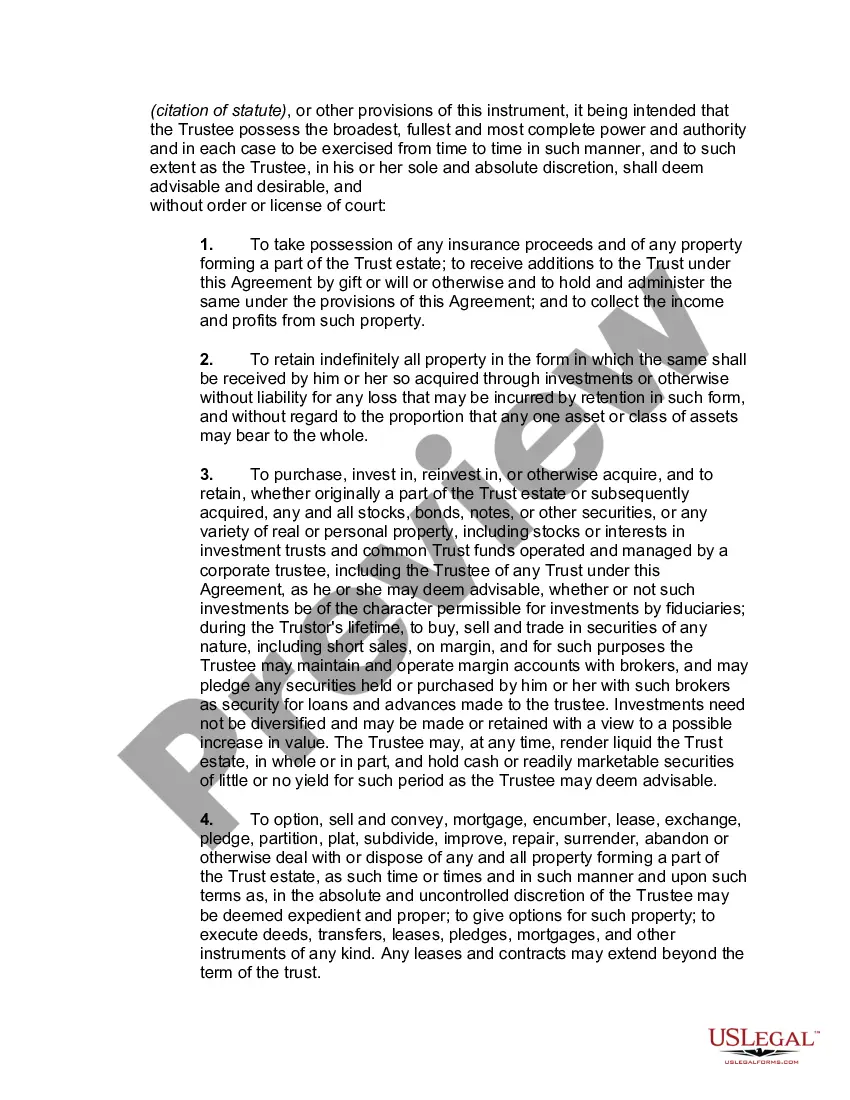

The Vermont Qualifying Subchapter-S Revocable Trust Agreement is a legal document that outlines the terms and conditions governing the creation and management of a revocable trust in the state of Vermont. This agreement is designed specifically to meet the requirements of a Subchapter-S corporation, which is a specific type of small business entity that offers certain tax advantages. A Revocable Trust, also known as a Living Trust, is a legal arrangement whereby an individual (referred to as the granter or settler) transfers their assets and property into a trust during their lifetime. The granter can then act as the trustee of the trust and maintain control over the assets while also designating beneficiaries who will receive the trust assets upon the granter's death. The Vermont Qualifying Subchapter-S Revocable Trust Agreement is structured in a way that allows the trust to qualify for the tax benefits of a Subchapter-S corporation, which include pass-through taxation and limited liability protection. This type of trust agreement is particularly useful for small business owners who wish to protect their personal assets while maintaining control and flexibility over their business interests. There are several types of Vermont Qualifying Subchapter-S Revocable Trust Agreements, depending on the specific needs and circumstances of the granter. These may include: 1. Individual Revocable Trust: This is the most common type of revocable trust agreement, wherein a single individual transfers their assets into the trust and designates beneficiaries to receive those assets upon their death. 2. Joint Revocable Trust: This type of trust agreement is created by a married couple or partners who jointly transfer their assets into the trust. Upon the death of one spouse or partner, the trust assets pass to the surviving spouse/partner, and upon the death of the second spouse/partner, the trust assets are distributed to the designated beneficiaries. 3. Charitable Remainder Trust: This type of trust agreement allows the granter to transfer assets into a trust while retaining an income stream from those assets for a specified period or until their death. Afterward, the remaining trust assets are distributed to a designated charity. 4. Marital Deduction Trust: This trust agreement is commonly used by married couples to take advantage of the marital deduction for estate tax purposes. The assets transferred into the trust are generally not subject to estate taxes upon the death of the first spouse, and the surviving spouse has the right to income from the trust assets during their lifetime. In summary, the Vermont Qualifying Subchapter-S Revocable Trust Agreement is a versatile legal document designed to meet the specific needs of individuals or couples who wish to create a revocable trust while also enjoying the tax benefits associated with a Subchapter-S corporation. By carefully crafting this trust agreement, individuals can protect their personal assets, maintain control over their business interests, and provide for the seamless transfer of assets to their chosen beneficiaries.

Vermont Qualifying Subchapter-S Revocable Trust Agreement

Description

How to fill out Vermont Qualifying Subchapter-S Revocable Trust Agreement?

US Legal Forms - one of several biggest libraries of legitimate forms in America - gives an array of legitimate file themes it is possible to download or print out. Utilizing the internet site, you may get a huge number of forms for organization and person functions, categorized by groups, states, or keywords and phrases.You will discover the latest variations of forms such as the Vermont Qualifying Subchapter-S Revocable Trust Agreement within minutes.

If you have a membership, log in and download Vermont Qualifying Subchapter-S Revocable Trust Agreement from your US Legal Forms catalogue. The Download option will show up on each and every kind you see. You gain access to all previously downloaded forms within the My Forms tab of your account.

If you would like use US Legal Forms the very first time, here are simple recommendations to help you started:

- Make sure you have chosen the proper kind for your personal city/state. Click on the Review option to analyze the form`s articles. Look at the kind outline to actually have chosen the appropriate kind.

- In case the kind does not match your demands, use the Search field on top of the screen to get the the one that does.

- In case you are content with the form, affirm your choice by simply clicking the Purchase now option. Then, select the rates program you like and supply your credentials to sign up to have an account.

- Method the transaction. Utilize your charge card or PayPal account to complete the transaction.

- Choose the structure and download the form on your own device.

- Make modifications. Fill out, edit and print out and indicator the downloaded Vermont Qualifying Subchapter-S Revocable Trust Agreement.

Each web template you included with your account lacks an expiry time and is your own eternally. So, if you want to download or print out an additional copy, just proceed to the My Forms section and click on on the kind you require.

Get access to the Vermont Qualifying Subchapter-S Revocable Trust Agreement with US Legal Forms, probably the most extensive catalogue of legitimate file themes. Use a huge number of skilled and express-certain themes that satisfy your company or person demands and demands.