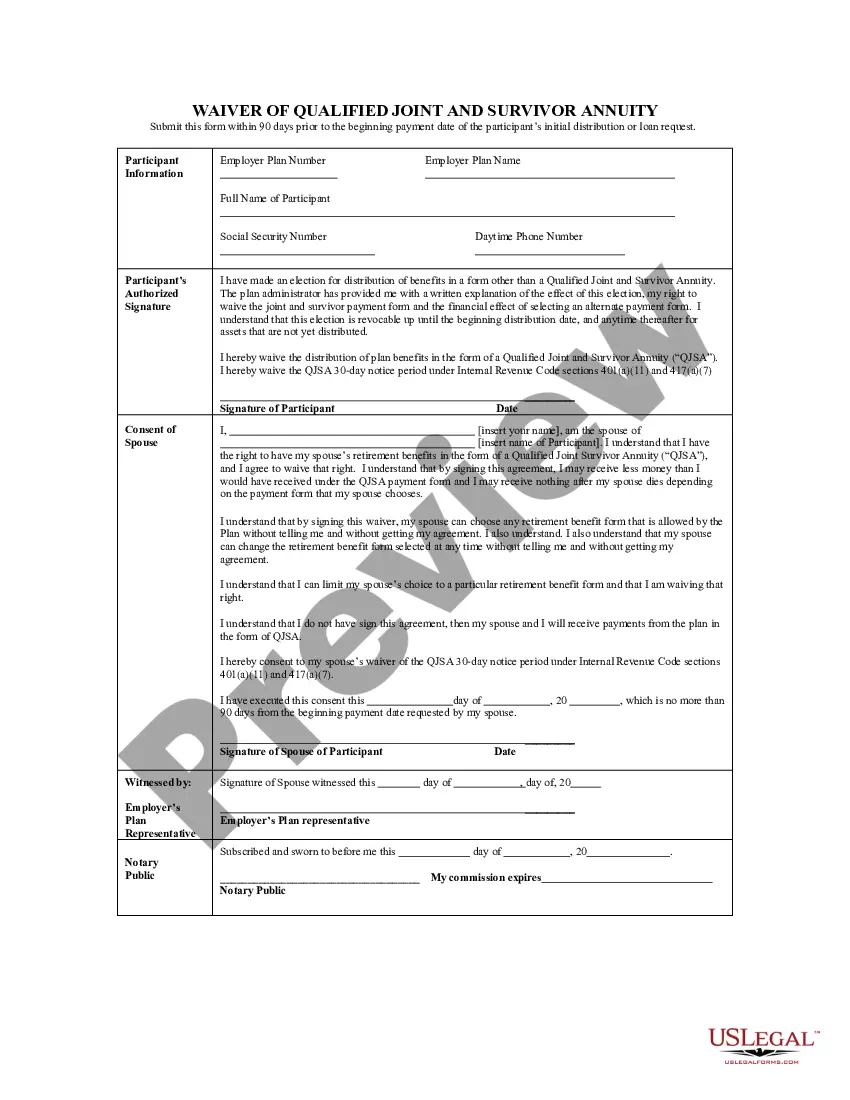

The Vermont Waiver of Qualified Joint and Survivor Annuity (JSA) is a legal provision that allows retirees to deviate from the default requirement of providing a lifetime income to their spouse upon their death. This provision ensures flexibility in retirement planning and allows individuals to make alternative arrangements for their pension benefits. In essence, the JSA requires pension plans to provide a surviving spouse with a predetermined percentage (typically 50% or 75%) of the retiree's pension income upon their death. This ensures financial security for the surviving spouse but can limit the retiree's control over the funds. However, the Vermont Waiver of Qualified Joint and Survivor Annuity offers retirees the opportunity to waive the default JSA option and choose other pension distributions that better align with their financial needs and preferences. By doing so, retirees can access their pension benefits in different ways, such as lump sum payments or higher monthly income without the requirement of a survivor benefit. This waiver is particularly beneficial for individuals who may have unique financial circumstances, such as having pre-existing financial arrangements for their spouse's support or desiring to leave a specific inheritance to their beneficiaries. By opting for the Vermont Waiver of JSA, retirees can customize their pension distribution according to their unique situation. While the Vermont Waiver of Qualified Joint and Survivor Annuity is one type of JSA waiver, it is important to note that there may be other variations or state-specific waivers available. These variations might include options like the Partial JSA, where a retiree can choose to provide their surviving spouse with a lower percentage of the pension income or for a specific limited time period. In conclusion, the Vermont Waiver of Qualified Joint and Survivor Annuity (JSA) enables retirees to deviate from the default requirement of providing a lifetime income to their spouse upon death. This provision allows retirees to tailor their pension distribution to their specific financial needs and preferences, ensuring flexibility in retirement planning. Other types of JSA waivers, like the Partial JSA, may also be available, offering retirees further customization options.

Vermont Waiver of Qualified Joint and Survivor Annuity - QJSA

Description

How to fill out Vermont Waiver Of Qualified Joint And Survivor Annuity - QJSA?

If you have to comprehensive, acquire, or print lawful file layouts, use US Legal Forms, the largest variety of lawful forms, that can be found on-line. Use the site`s basic and convenient look for to obtain the papers you need. Various layouts for organization and individual purposes are categorized by categories and states, or key phrases. Use US Legal Forms to obtain the Vermont Waiver of Qualified Joint and Survivor Annuity - QJSA in just a number of clicks.

In case you are already a US Legal Forms client, log in for your profile and click the Download button to find the Vermont Waiver of Qualified Joint and Survivor Annuity - QJSA. You can even entry forms you in the past delivered electronically in the My Forms tab of your own profile.

Should you use US Legal Forms the very first time, follow the instructions below:

- Step 1. Ensure you have chosen the form for the proper metropolis/country.

- Step 2. Utilize the Preview method to examine the form`s information. Do not overlook to learn the outline.

- Step 3. In case you are unhappy using the develop, make use of the Lookup field on top of the monitor to discover other versions of the lawful develop template.

- Step 4. Once you have located the form you need, go through the Get now button. Pick the prices strategy you like and add your credentials to register for an profile.

- Step 5. Approach the purchase. You can use your charge card or PayPal profile to accomplish the purchase.

- Step 6. Find the file format of the lawful develop and acquire it on the gadget.

- Step 7. Full, edit and print or indication the Vermont Waiver of Qualified Joint and Survivor Annuity - QJSA.

Each lawful file template you get is the one you have eternally. You have acces to every single develop you delivered electronically inside your acccount. Click on the My Forms section and select a develop to print or acquire yet again.

Contend and acquire, and print the Vermont Waiver of Qualified Joint and Survivor Annuity - QJSA with US Legal Forms. There are thousands of professional and status-specific forms you can utilize for the organization or individual requires.