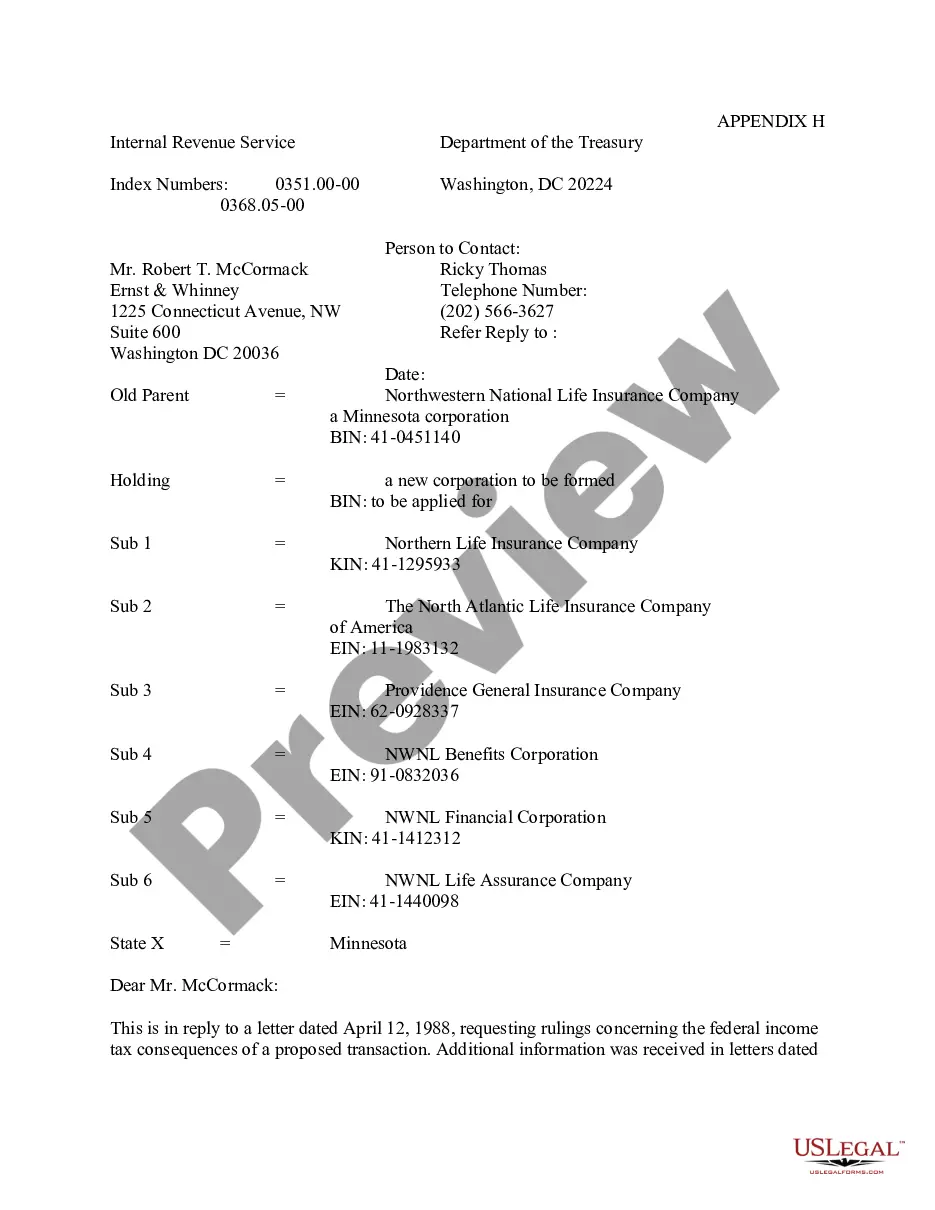

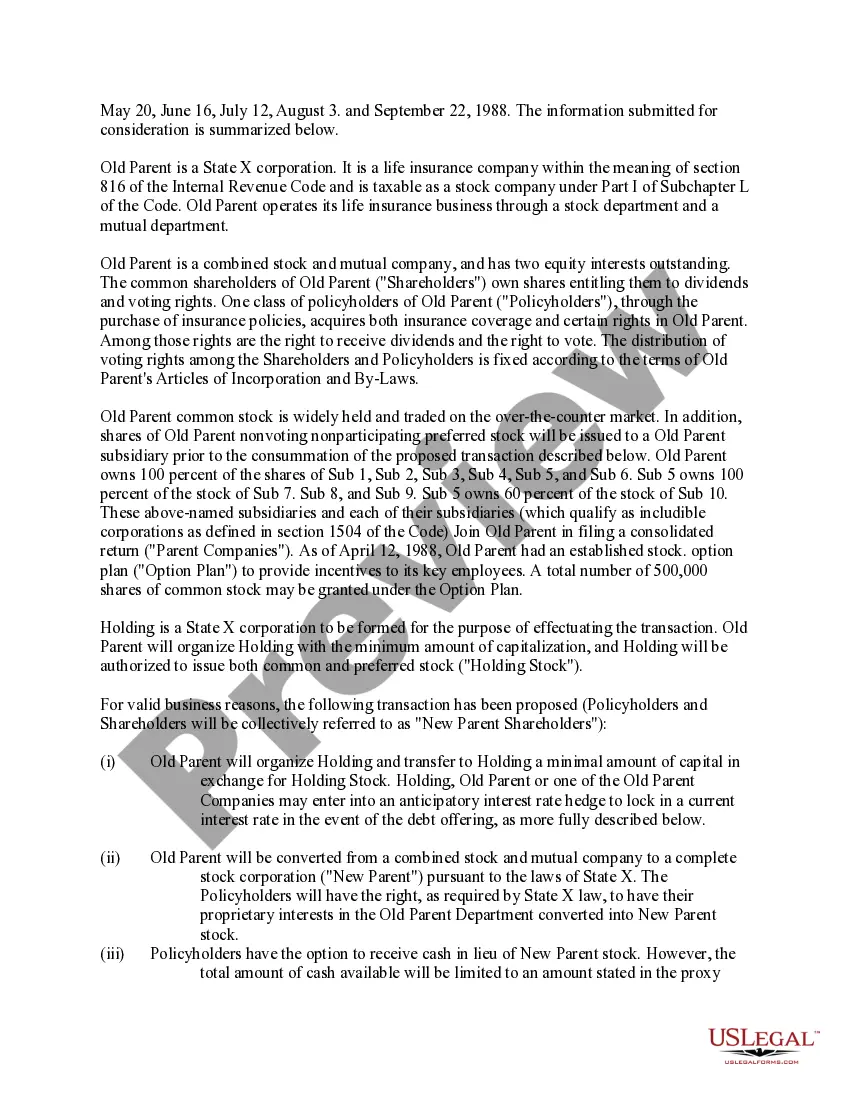

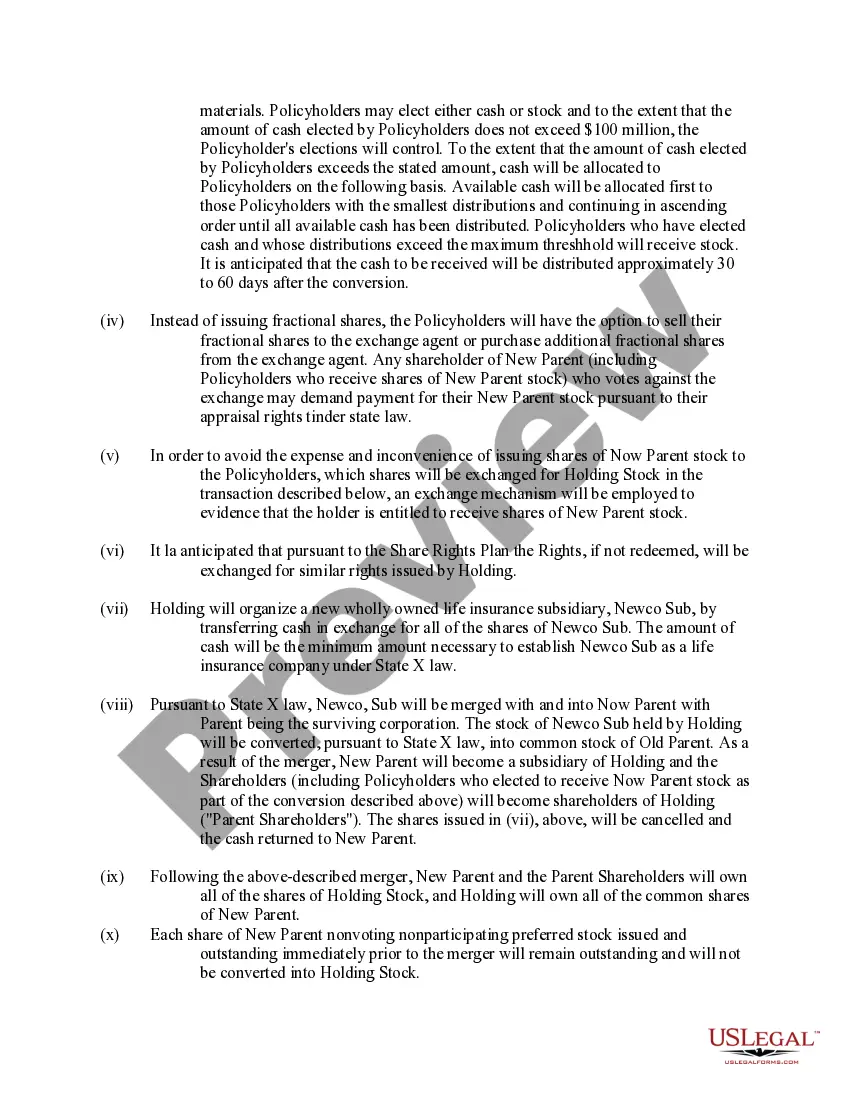

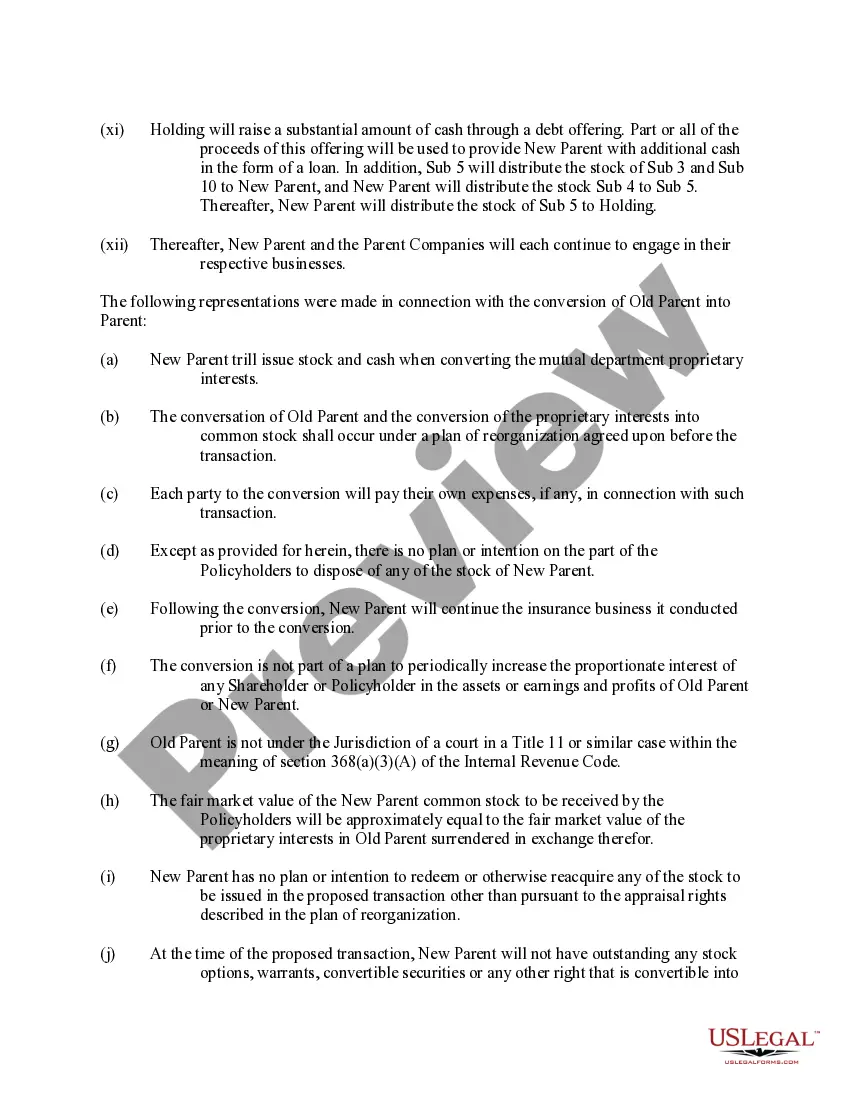

The Vermont Internal Revenue Service (IRS) Ruling Letter is an official document that provides guidance on tax-related matters to individuals, businesses, and organizations operating in the state of Vermont. It is issued by the IRS, which is the federal agency responsible for enforcing tax laws in the United States. The ruling letter serves as an authoritative interpretation of the tax laws and regulations applicable in Vermont. This ruling letter plays a crucial role in clarifying complex tax issues, providing taxpayers with a better understanding of their tax obligations, rights, and available deductions. It addresses specific tax questions or scenarios presented by taxpayers and provides a definitive ruling or interpretation for their specific situation. These letters are generally applicable to both individual and corporate taxpayers and cover various aspects of tax laws, including income tax, sales tax, property tax, and employment tax, among others. There are different types of Vermont Internal Revenue Service Ruling Letters, each addressing specific tax matters. Some key types include: 1. Income Tax Ruling Letter: This type of ruling letter focuses on income tax-related issues, such as the classification of income, deductions, exemptions, and credits. It provides taxpayers with guidance on how to report income accurately and claim eligible deductions within the framework of Vermont tax laws. 2. Sales Tax Ruling Letter: Sales tax is a significant revenue source for the state of Vermont, and this letter provides guidance on the application of sales tax regulations. It clarifies when and how sales tax should be collected, exemptions that may apply, and reporting requirements for businesses engaged in selling taxable goods or services. 3. Property Tax Ruling Letter: Property tax is another crucial aspect of the tax system, and this letter addresses matters such as the assessment of property, exemptions for certain properties, and procedures for appealing property tax assessments. 4. Employment Tax Ruling Letter: Employment tax encompasses payroll taxes, such as Social Security and Medicare taxes, as well as federal and state income tax withholding. This ruling letter provides guidance on how employers should calculate and withhold these taxes correctly, report them to the appropriate tax agencies, and fulfill associated compliance requirements. It is important to note that the content and availability of ruling letters may vary over time as tax laws and regulations change. Therefore, taxpayers are advised to consult the most recent guidance provided by the Vermont Internal Revenue Service through their official website or by contacting authorized tax professionals.

Vermont Internal Revenue Service Ruling Letter

Description

How to fill out Vermont Internal Revenue Service Ruling Letter?

If you wish to complete, acquire, or produce legitimate file layouts, use US Legal Forms, the largest selection of legitimate forms, which can be found on the web. Utilize the site`s simple and easy hassle-free search to get the files you require. Various layouts for enterprise and personal purposes are categorized by types and says, or key phrases. Use US Legal Forms to get the Vermont Internal Revenue Service Ruling Letter in a few click throughs.

Should you be previously a US Legal Forms buyer, log in to your accounts and click the Down load option to have the Vermont Internal Revenue Service Ruling Letter. Also you can accessibility forms you previously saved inside the My Forms tab of your own accounts.

If you use US Legal Forms for the first time, refer to the instructions under:

- Step 1. Ensure you have selected the shape for the appropriate town/country.

- Step 2. Make use of the Preview option to check out the form`s information. Never overlook to read the description.

- Step 3. Should you be unhappy together with the form, utilize the Lookup industry on top of the display screen to get other versions in the legitimate form template.

- Step 4. When you have discovered the shape you require, go through the Buy now option. Pick the pricing prepare you like and add your qualifications to sign up for an accounts.

- Step 5. Approach the financial transaction. You can utilize your Мisa or Ьastercard or PayPal accounts to complete the financial transaction.

- Step 6. Choose the format in the legitimate form and acquire it on the device.

- Step 7. Full, modify and produce or indication the Vermont Internal Revenue Service Ruling Letter.

Every single legitimate file template you buy is your own permanently. You have acces to every form you saved in your acccount. Click the My Forms segment and pick a form to produce or acquire once more.

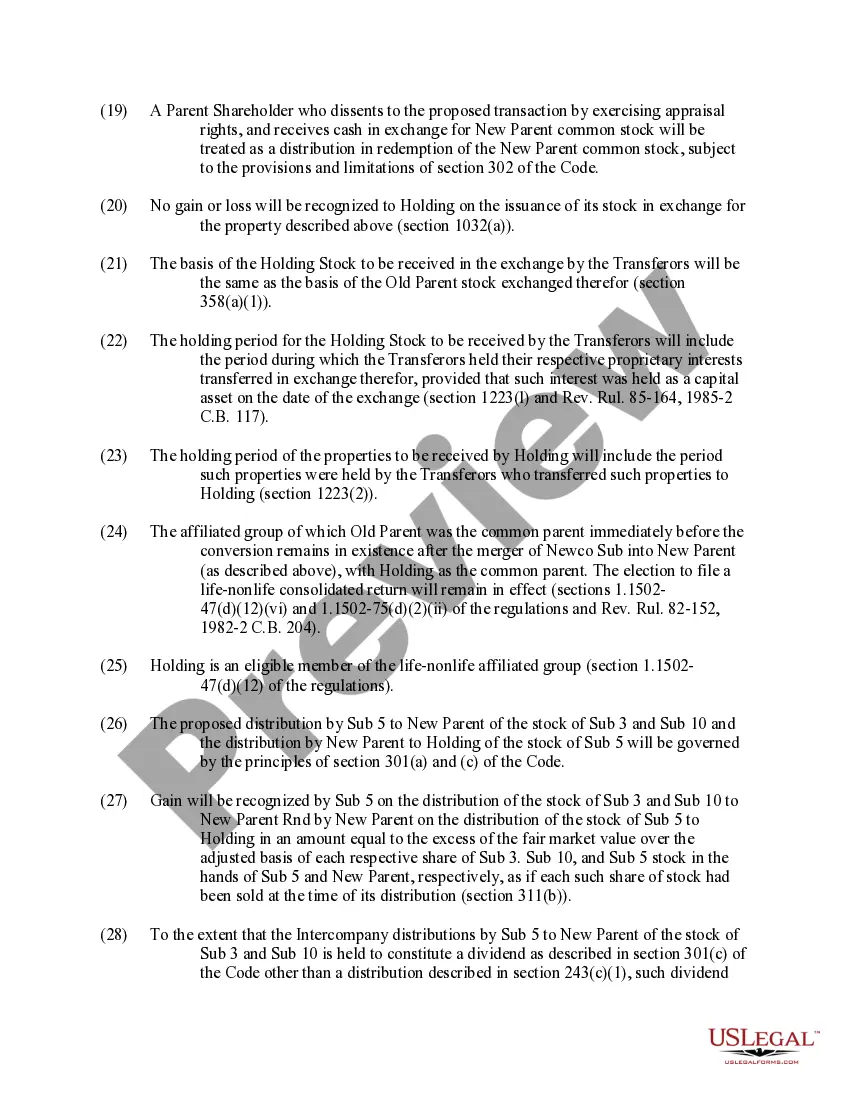

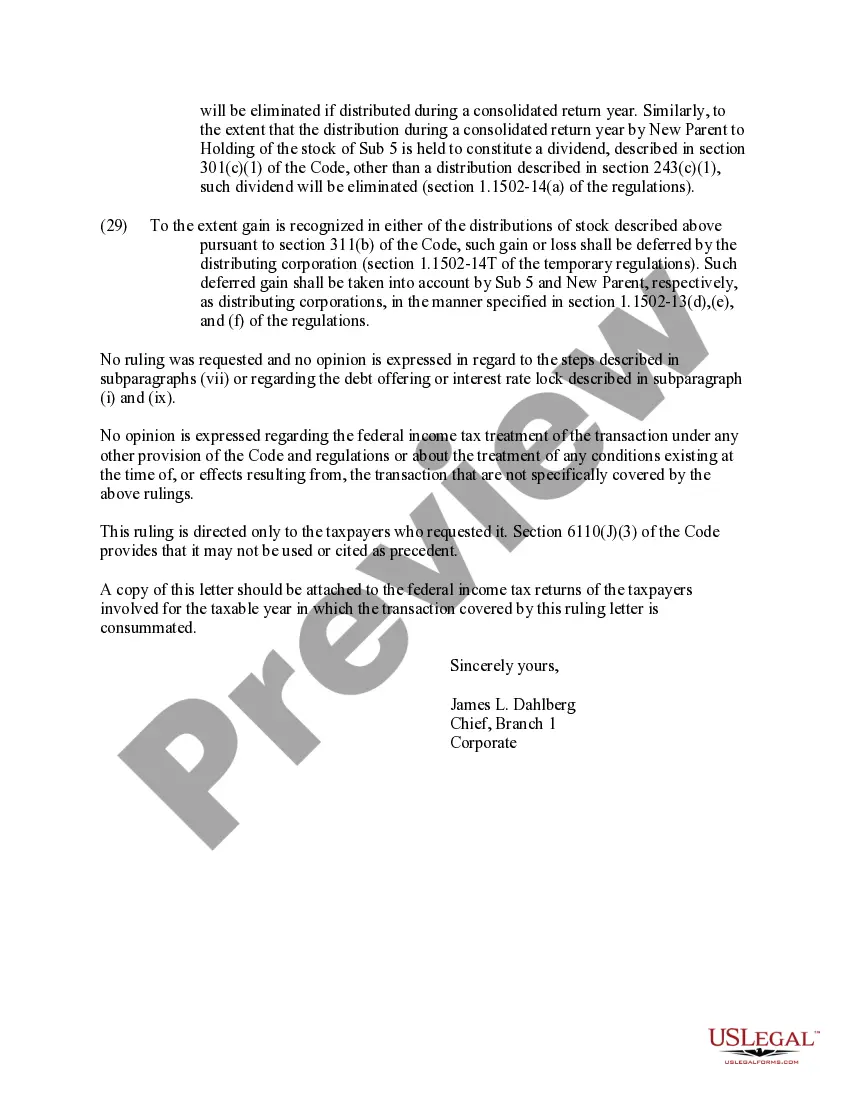

Remain competitive and acquire, and produce the Vermont Internal Revenue Service Ruling Letter with US Legal Forms. There are many specialist and condition-certain forms you can use for your personal enterprise or personal demands.