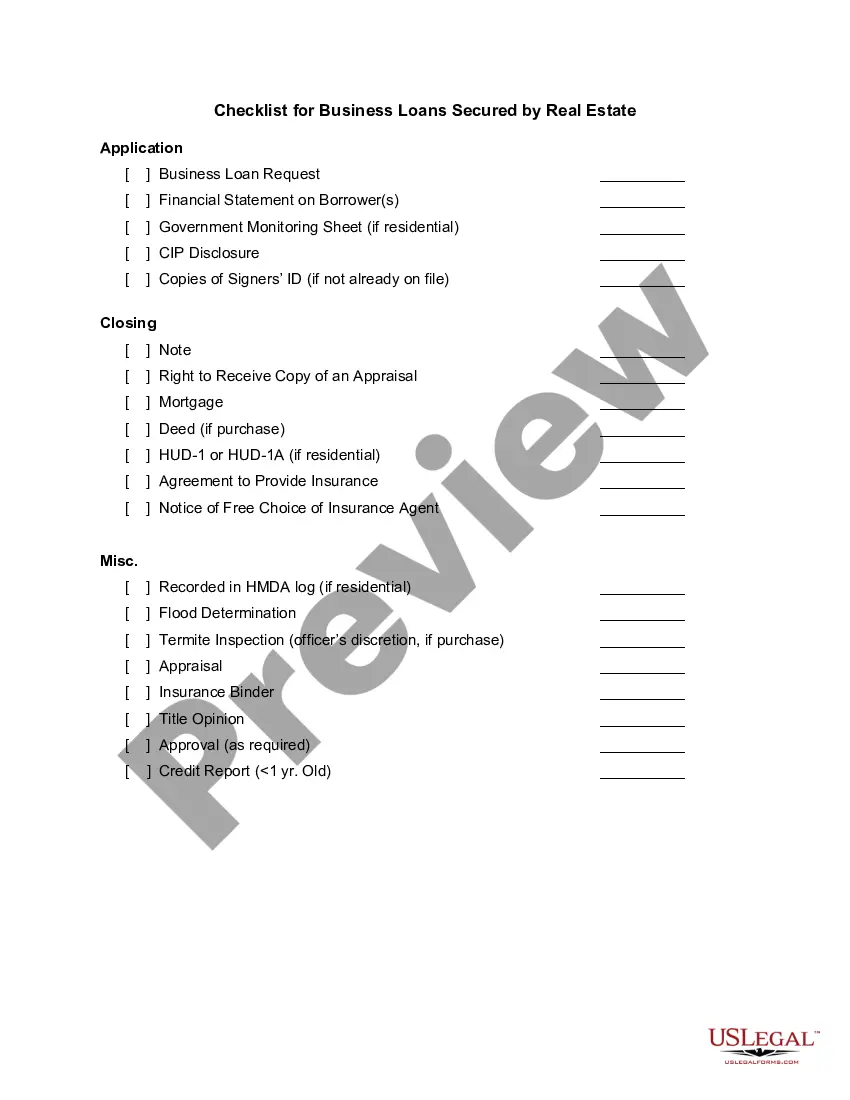

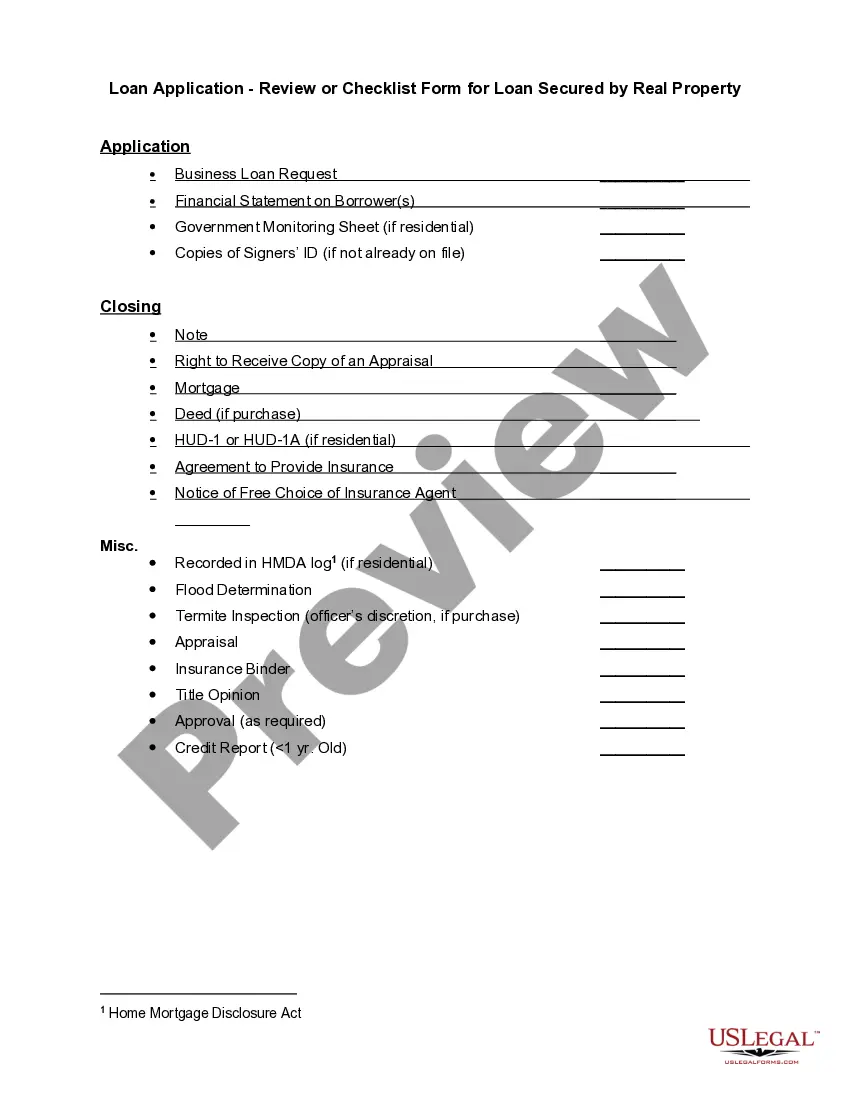

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Vermont Checklist for Real Estate Loans

State:

Multi-State

Control #:

US-CRE897

Format:

Word;

PDF;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Checklist For Real Estate Loans?

US Legal Forms - one of several biggest libraries of legal kinds in the United States - delivers a wide array of legal record templates you are able to download or printing. Using the site, you can get thousands of kinds for enterprise and individual purposes, sorted by groups, claims, or keywords.You can find the most up-to-date models of kinds just like the Vermont Checklist for Real Estate Loans in seconds.

If you have a registration, log in and download Vermont Checklist for Real Estate Loans from your US Legal Forms catalogue. The Down load button will show up on each and every develop you look at. You have accessibility to all previously delivered electronically kinds from the My Forms tab of your respective bank account.

If you would like use US Legal Forms for the first time, listed here are easy guidelines to help you started out:

- Ensure you have chosen the proper develop for your personal city/state. Go through the Preview button to check the form`s information. Look at the develop explanation to actually have selected the correct develop.

- When the develop does not fit your specifications, utilize the Lookup field on top of the display screen to find the one that does.

- If you are satisfied with the shape, affirm your choice by clicking the Purchase now button. Then, pick the rates strategy you like and offer your accreditations to sign up on an bank account.

- Method the purchase. Make use of your Visa or Mastercard or PayPal bank account to complete the purchase.

- Select the structure and download the shape on your own product.

- Make adjustments. Fill up, edit and printing and signal the delivered electronically Vermont Checklist for Real Estate Loans.

Each format you included in your account lacks an expiration particular date and is also your own property eternally. So, in order to download or printing an additional backup, just proceed to the My Forms area and click on in the develop you need.

Get access to the Vermont Checklist for Real Estate Loans with US Legal Forms, the most comprehensive catalogue of legal record templates. Use thousands of specialist and condition-specific templates that fulfill your business or individual requirements and specifications.