Vermont Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Vermont Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

You are able to invest time on the Internet searching for the lawful record design that fits the state and federal demands you will need. US Legal Forms gives a large number of lawful varieties which are analyzed by pros. You can easily download or printing the Vermont Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself from my support.

If you already possess a US Legal Forms accounts, you are able to log in and click on the Acquire option. Next, you are able to full, edit, printing, or signal the Vermont Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. Every single lawful record design you get is your own property for a long time. To acquire yet another duplicate for any bought type, check out the My Forms tab and click on the corresponding option.

If you work with the US Legal Forms web site the first time, adhere to the straightforward instructions below:

- Initially, make certain you have selected the proper record design for the area/town that you pick. Look at the type description to ensure you have picked the proper type. If accessible, take advantage of the Review option to appear from the record design as well.

- In order to find yet another model of the type, take advantage of the Research area to discover the design that suits you and demands.

- After you have identified the design you want, simply click Purchase now to proceed.

- Select the prices plan you want, key in your references, and sign up for a free account on US Legal Forms.

- Total the transaction. You can utilize your credit card or PayPal accounts to fund the lawful type.

- Select the formatting of the record and download it in your device.

- Make changes in your record if possible. You are able to full, edit and signal and printing Vermont Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself.

Acquire and printing a large number of record layouts using the US Legal Forms web site, that provides the largest assortment of lawful varieties. Use specialist and express-particular layouts to handle your small business or individual needs.

Form popularity

FAQ

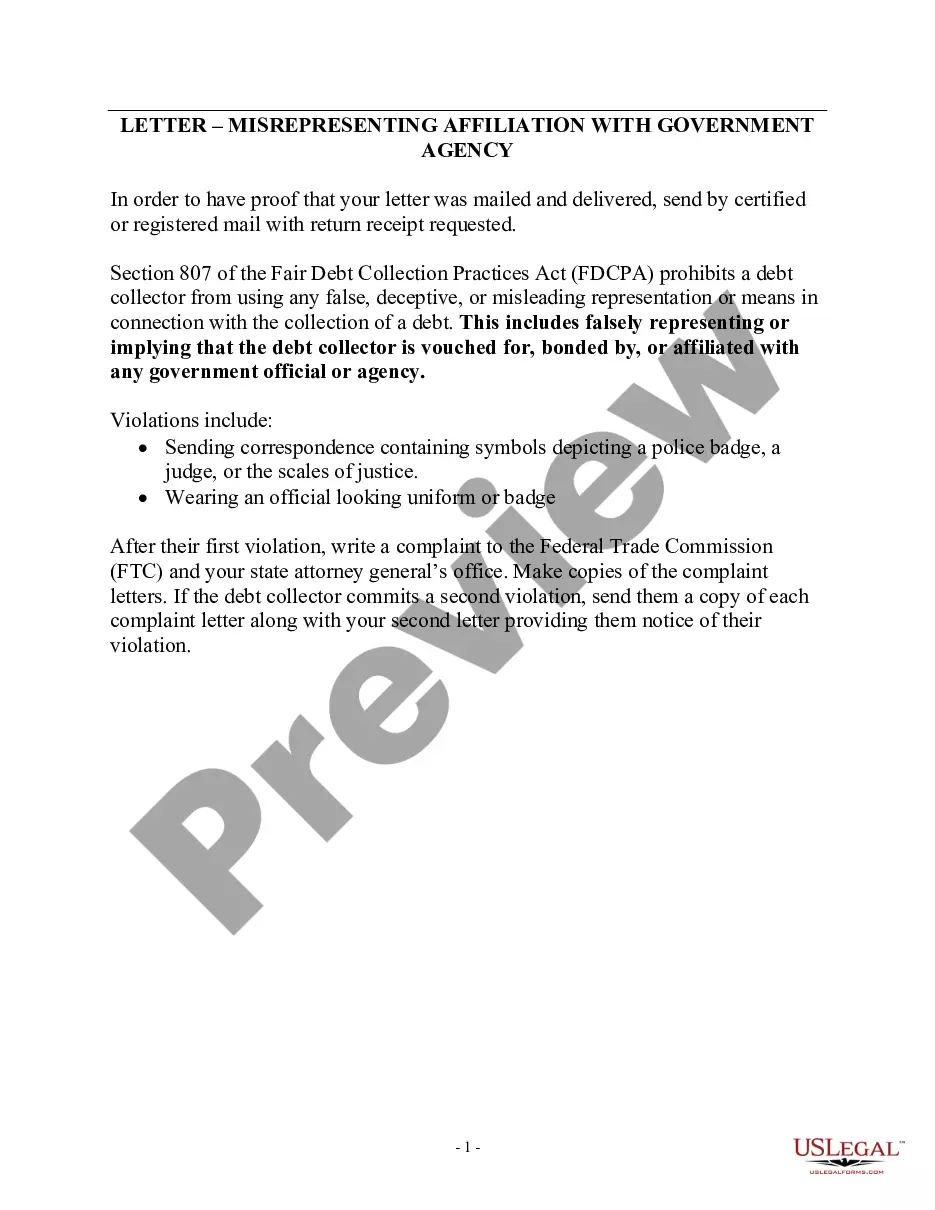

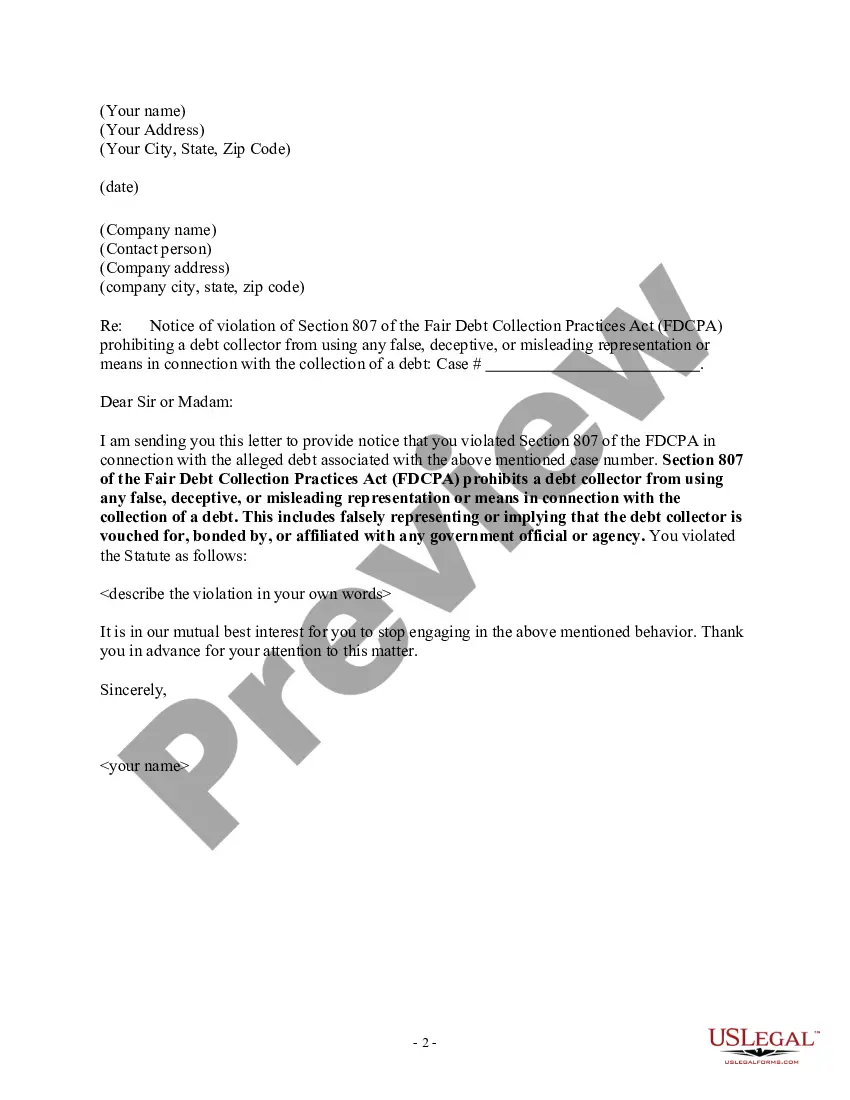

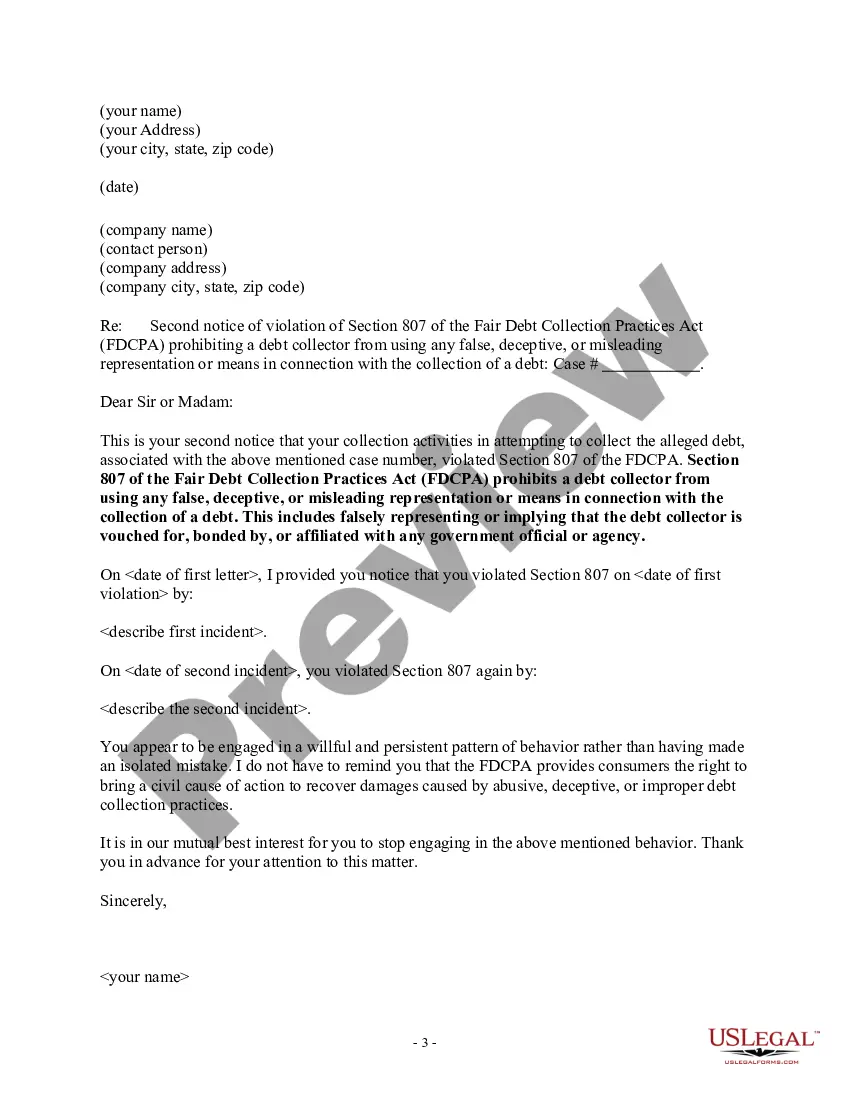

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

Yes, but the collector must first sue you to get a court order called a garnishment that says it can take money from your paycheck to pay your debts. A collector also can seek a court order to take money from your bank account.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

If the FDCPA is violated, the debtor can sue the debt collection company as well as the individual debt collector for damages and attorney fees.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

One is to report them to the Financial Consumer Protection Department of the BSP (i.e. email consumeraffairs@bsp.gov.ph or call 632-708-7087). Be sure to document all communications with your debt collectors including text messages and e-mails. If you can, record your conversation with their consent.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.16-Sept-2020