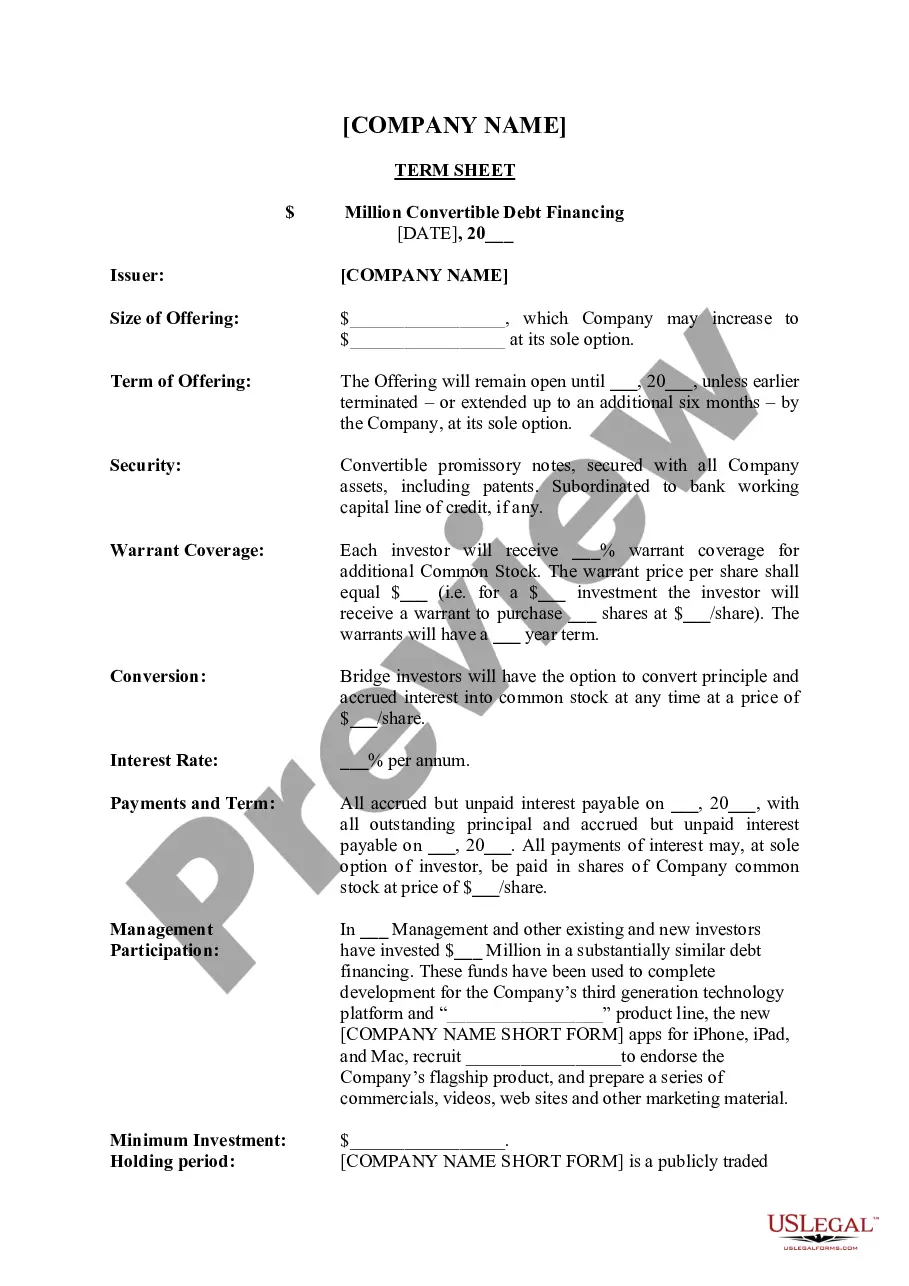

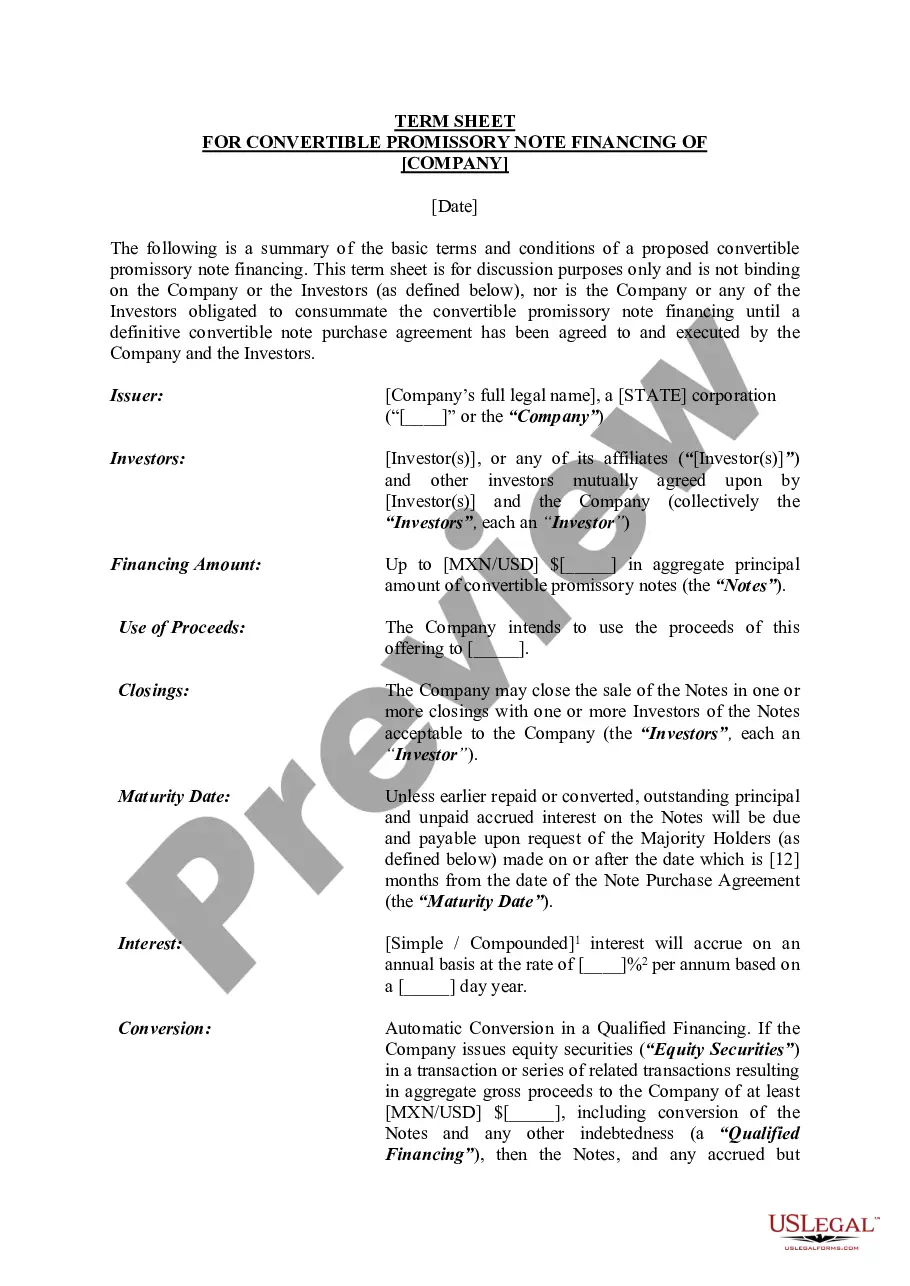

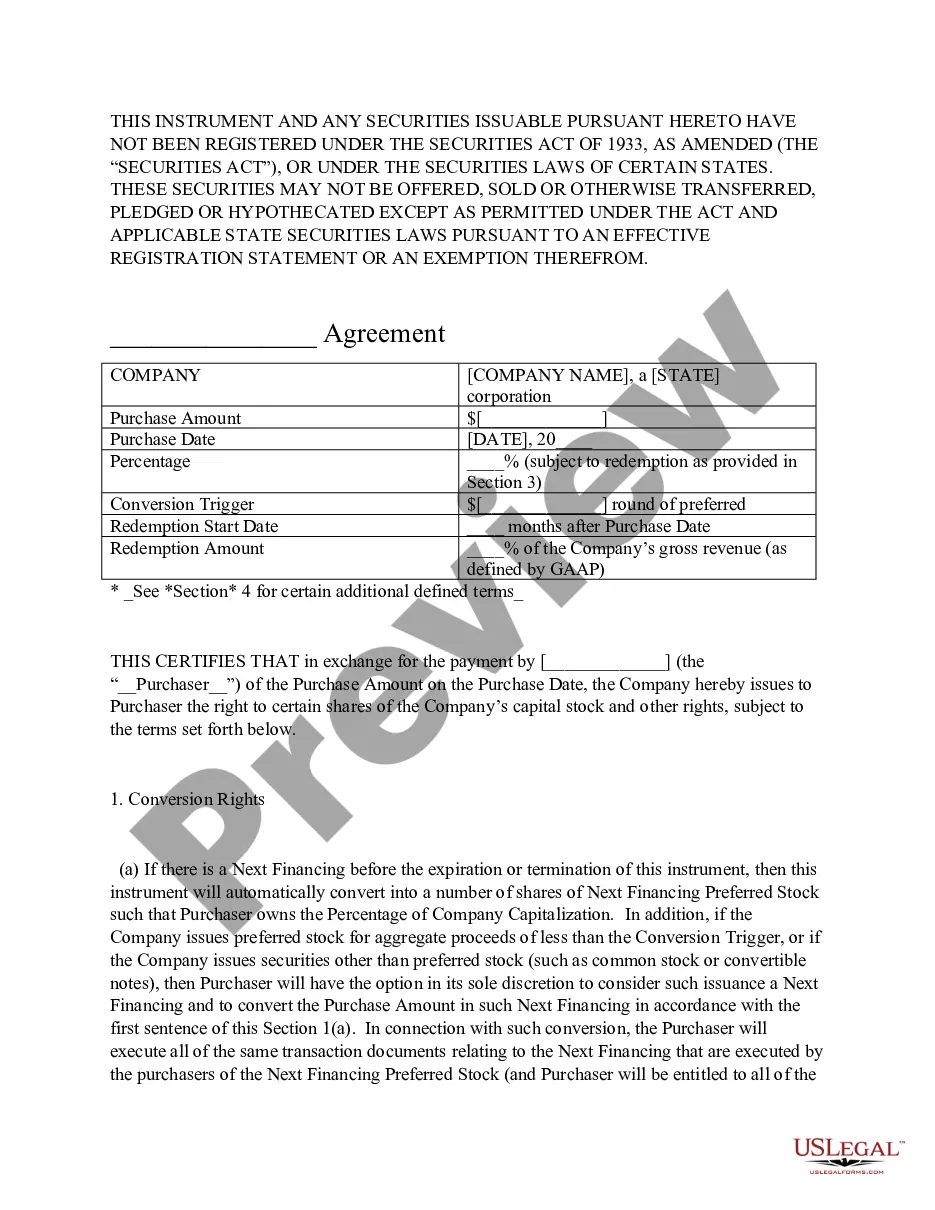

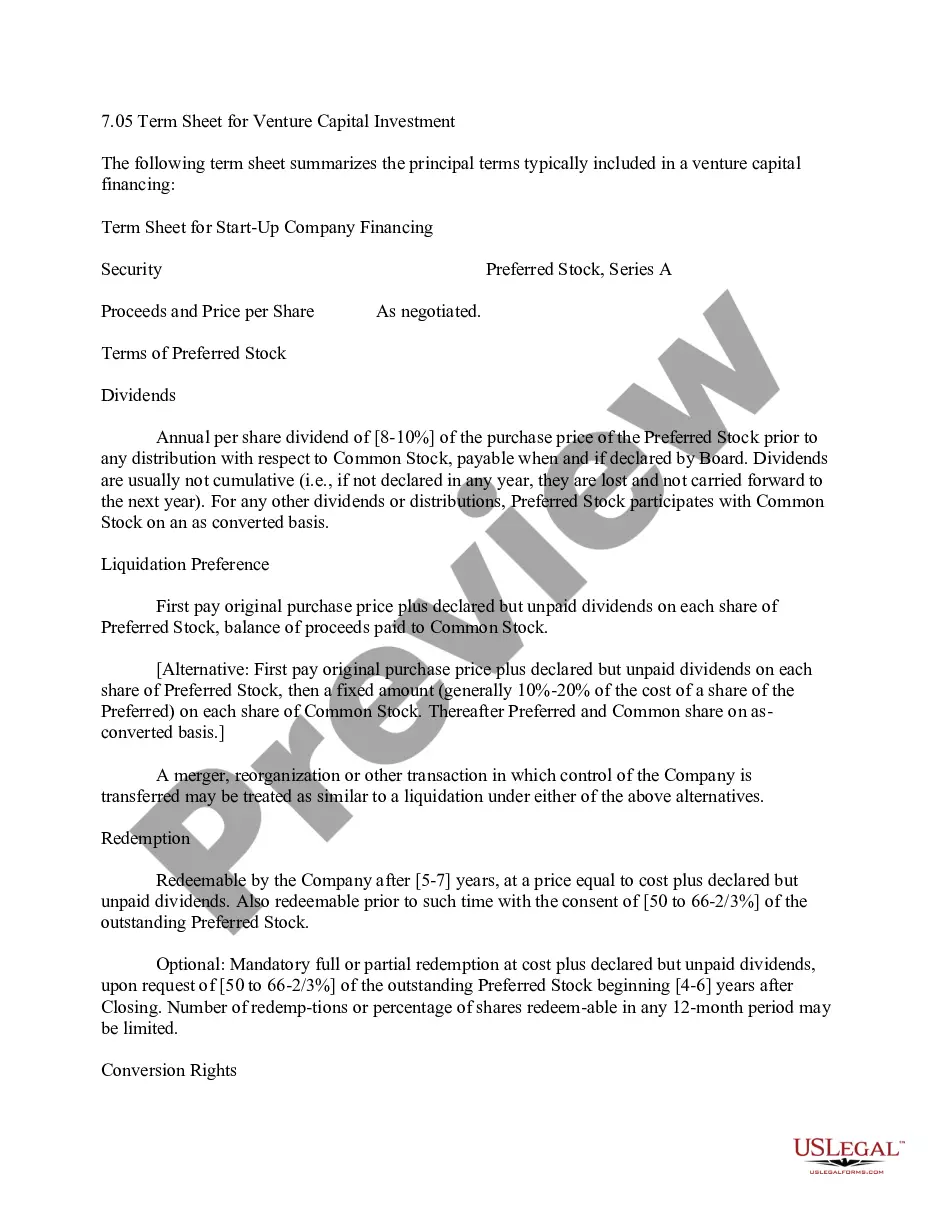

Vermont Term Sheet - Convertible Debt Financing

Description

How to fill out Term Sheet - Convertible Debt Financing?

Discovering the right legitimate file template can be a have difficulties. Needless to say, there are a variety of web templates available on the Internet, but how would you get the legitimate form you will need? Utilize the US Legal Forms web site. The assistance provides 1000s of web templates, such as the Vermont Term Sheet - Convertible Debt Financing, that can be used for company and private requires. All of the kinds are checked out by professionals and meet state and federal requirements.

In case you are presently listed, log in to your account and click on the Acquire button to get the Vermont Term Sheet - Convertible Debt Financing. Use your account to look with the legitimate kinds you may have purchased formerly. Proceed to the My Forms tab of your respective account and have an additional copy of the file you will need.

In case you are a whole new user of US Legal Forms, here are basic recommendations that you should stick to:

- Initial, be sure you have selected the correct form for the town/area. You can look over the shape while using Review button and read the shape outline to guarantee it will be the best for you.

- In case the form fails to meet your needs, use the Seach discipline to get the appropriate form.

- When you are certain the shape is proper, click on the Acquire now button to get the form.

- Pick the pricing prepare you need and enter in the needed details. Make your account and purchase your order making use of your PayPal account or Visa or Mastercard.

- Opt for the submit formatting and down load the legitimate file template to your gadget.

- Full, edit and printing and sign the obtained Vermont Term Sheet - Convertible Debt Financing.

US Legal Forms is the most significant local library of legitimate kinds that you can see different file web templates. Utilize the company to down load expertly-made papers that stick to condition requirements.

Form popularity

FAQ

A company lists its long-term debt on its balance sheet under liabilities, usually under a subheading for long-term liabilities. On Which Financial Statements Do Companies Report Long-Term Debt? investopedia.com ? ask ? answers ? which-fi... investopedia.com ? ask ? answers ? which-fi...

Convertible debt may become current Generally, if a liability has any conversion options that involve a transfer of the company's own equity instruments, these would affect its classification as current or non-current. Classifying liabilities as current or non-current kpmg.com ? dam ? kpmg ? pdf ? 2020/07 kpmg.com ? dam ? kpmg ? pdf ? 2020/07

Convertible bonds are basically debt instruments but they also contain an option to convert into equity shares and this means that a convertible bond contains both debt and equity elements. The option to convert into equity is strictly a derivative that is embedded into the host contract. What is a financial instrument? ? part 2 - ACCA Global accaglobal.com ? student ? technical-articles accaglobal.com ? student ? technical-articles

Convertible debt is a debt hybrid product with an embedded option that allows the holder to convert the debt into equity in the future. The ratio is calculated by dividing the convertible security's par value by the conversion price of equity.

Repayment Method With most convertible debt, you will repay the investment by converting the entire value to stock. Some investors, though, may also include language that obligates you to pay back a certain percentage of the original investment as cash and the remainder as stock. Convertible Debt For Startups: The Complete Guide - Bond Collective bondcollective.com ? blog ? convertible-debt bondcollective.com ? blog ? convertible-debt

Convertible Notes are loans ? so they are recorded on the Balance Sheet of a company as a liability when they are made. Depending on the debt's maturity date, they can either be shown as a current liability (loans maturing within 12 months) or as a Long-term liability (loans maturing over 12 months).

Although it is customary to forego a term sheet, in some cases it may be required if the parties need to negotiate certain terms. It can be advantageous to use a term sheet for the company to easily summarize the terms of the notes for potential other investors purchasing a convertible note.

For tax purposes, the tax basis of the convertible debt is the entire proceeds received at issuance of the debt. Thus, the book and tax bases of the convertible debt are different. ASC 740-10-55-51 addresses whether a deferred tax liability should be recognized for that basis difference.