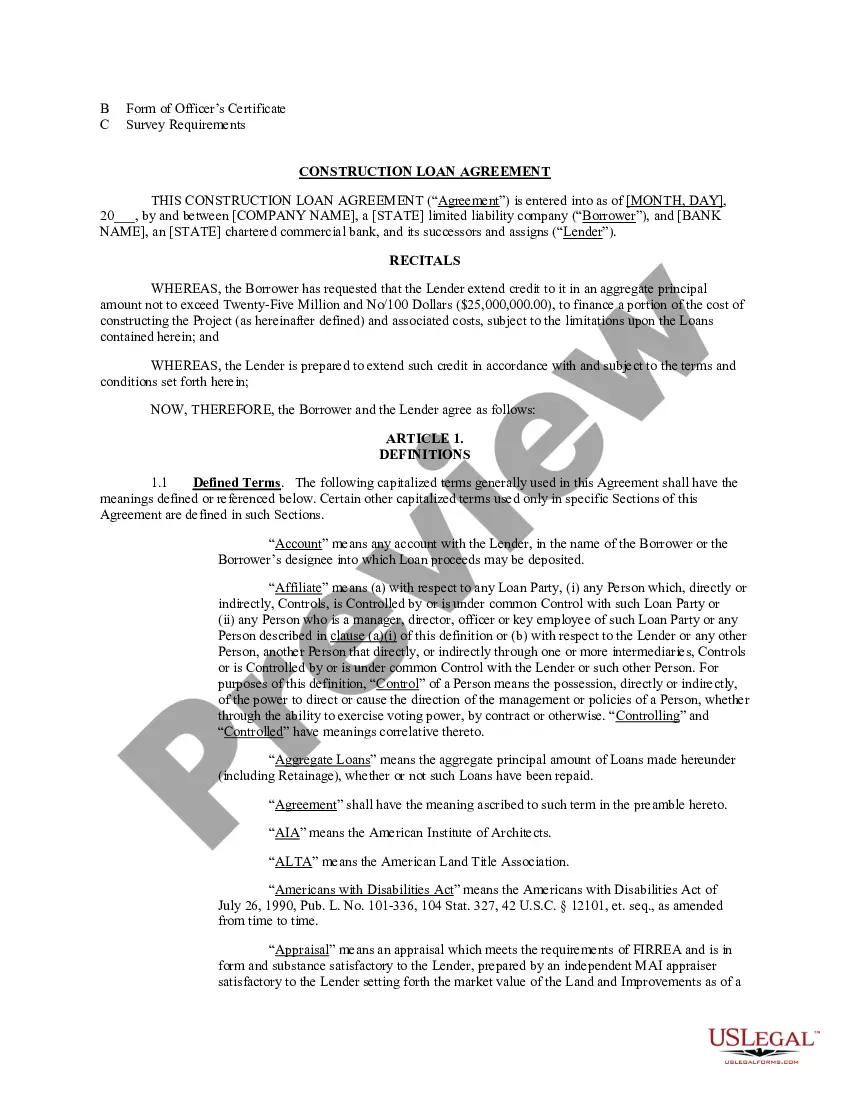

The Vermont Construction Loan Agreement is a legally binding contract between a borrower and a lender, commonly used for financing construction projects in the state of Vermont. This agreement outlines the terms and conditions under which the lender agrees to provide funds to the borrower for the purpose of constructing or renovating a property. Keywords: Vermont, Construction Loan Agreement, financing, construction projects, borrower, lender, funds, constructing, renovating, property. There are different types of Vermont Construction Loan Agreements, including: 1. Single-Close Construction Loan Agreement: This type of agreement combines the construction loan and the permanent mortgage into a single loan, eliminating the need for two separate agreements. It allows borrowers to obtain long-term financing without going through the application process again after the construction is completed. 2. Two-Close Construction Loan Agreement: In this type of agreement, the borrower first obtains a construction loan from the lender to finance the building phase of the project. Once the construction is completed, the borrower must secure a separate permanent mortgage loan to repay the construction loan. This approach involves separate closing processes and sets of fees. 3. Construction to Permanent Loan Agreement: This agreement is similar to the two-close construction loan agreement, but it allows the borrower to convert the construction loan into a permanent mortgage loan without going through a separate closing process. This streamlines the financing process and reduces the costs associated with multiple closings. 4. Owner-Builder Construction Loan Agreement: This type of agreement is specifically designed for borrowers who plan to act as their own general contractors or perform a significant portion of the construction work themselves. It may require additional documentation, such as plans, budgets, and proof of experience in construction, to ensure the borrower's ability to successfully complete the project. In conclusion, the Vermont Construction Loan Agreement is a crucial legal document that outlines the terms and conditions of financing for construction projects in Vermont. With various types of agreements available, borrowers have flexibility in choosing the option that best suits their needs.

Vermont Construction Loan Agreement

Description

How to fill out Vermont Construction Loan Agreement?

Choosing the best authorized document web template might be a have a problem. Naturally, there are a lot of layouts available online, but how would you get the authorized kind you want? Make use of the US Legal Forms internet site. The assistance delivers thousands of layouts, such as the Vermont Construction Loan Agreement, that you can use for company and personal needs. All the varieties are checked out by specialists and satisfy federal and state needs.

If you are previously signed up, log in in your bank account and then click the Obtain option to obtain the Vermont Construction Loan Agreement. Make use of your bank account to look throughout the authorized varieties you possess acquired in the past. Visit the My Forms tab of your bank account and get one more backup of the document you want.

If you are a fresh end user of US Legal Forms, listed below are basic recommendations so that you can adhere to:

- First, be sure you have selected the correct kind for your metropolis/area. You are able to examine the form utilizing the Review option and look at the form information to guarantee it will be the right one for you.

- If the kind will not satisfy your needs, use the Seach discipline to find the proper kind.

- Once you are sure that the form is proper, click on the Get now option to obtain the kind.

- Select the pricing plan you want and enter the needed details. Make your bank account and pay money for an order using your PayPal bank account or credit card.

- Select the file structure and down load the authorized document web template in your device.

- Full, modify and print and signal the attained Vermont Construction Loan Agreement.

US Legal Forms will be the most significant collection of authorized varieties for which you can discover a variety of document layouts. Make use of the service to down load professionally-made paperwork that adhere to condition needs.