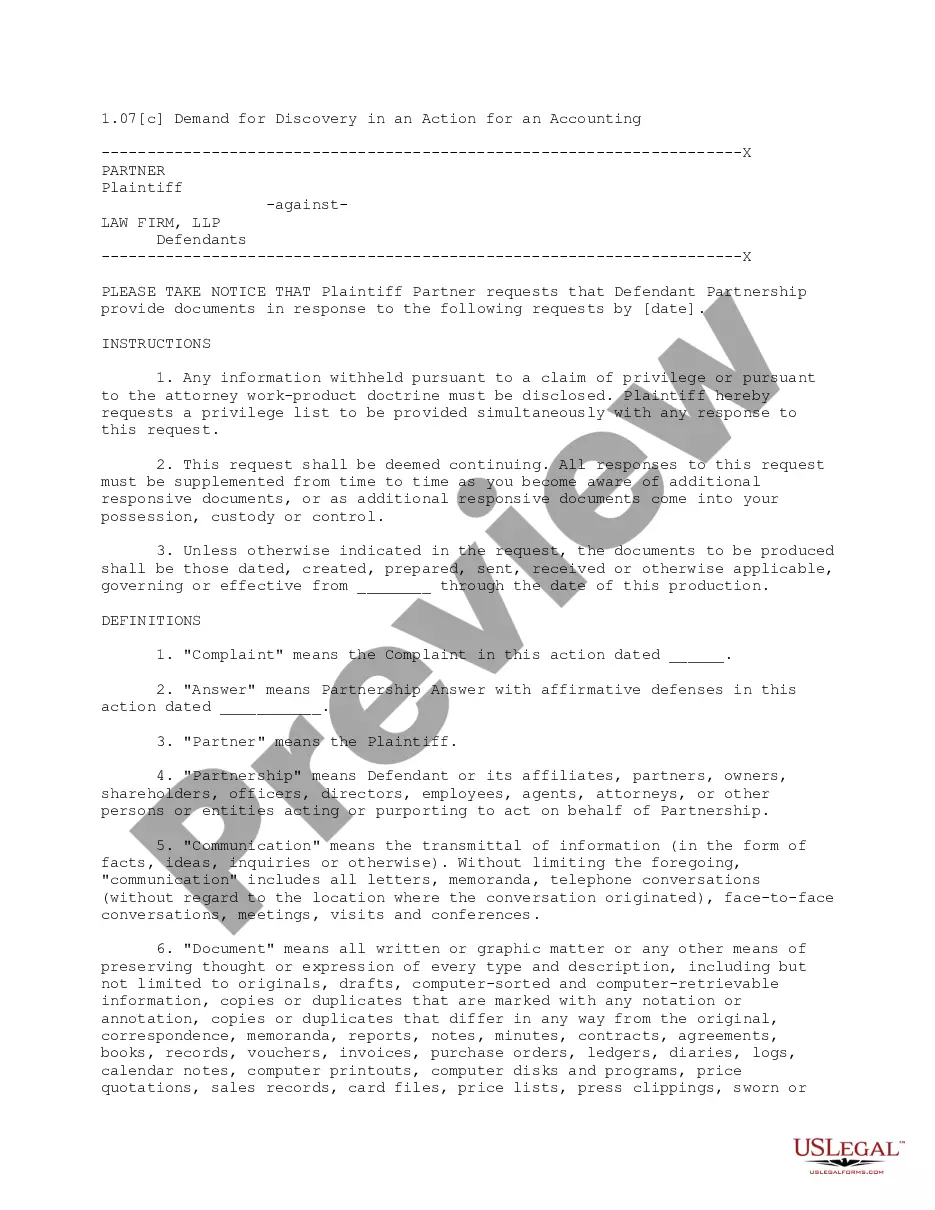

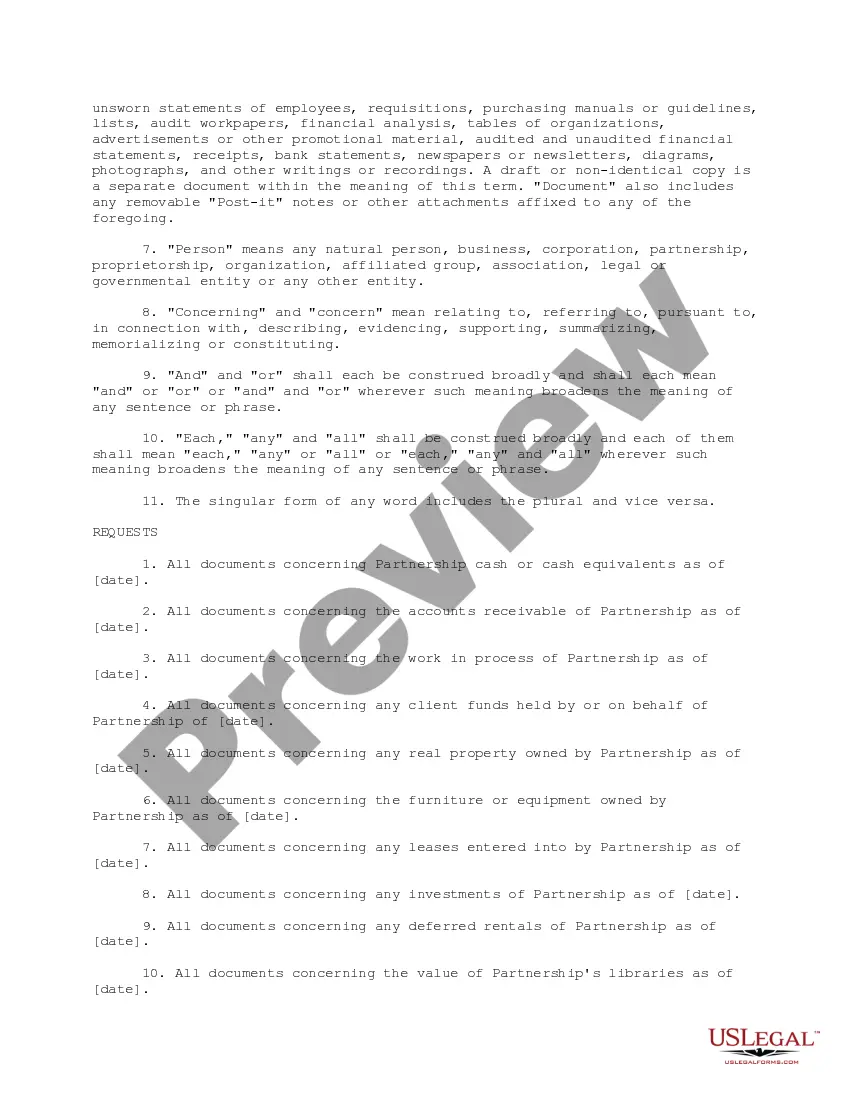

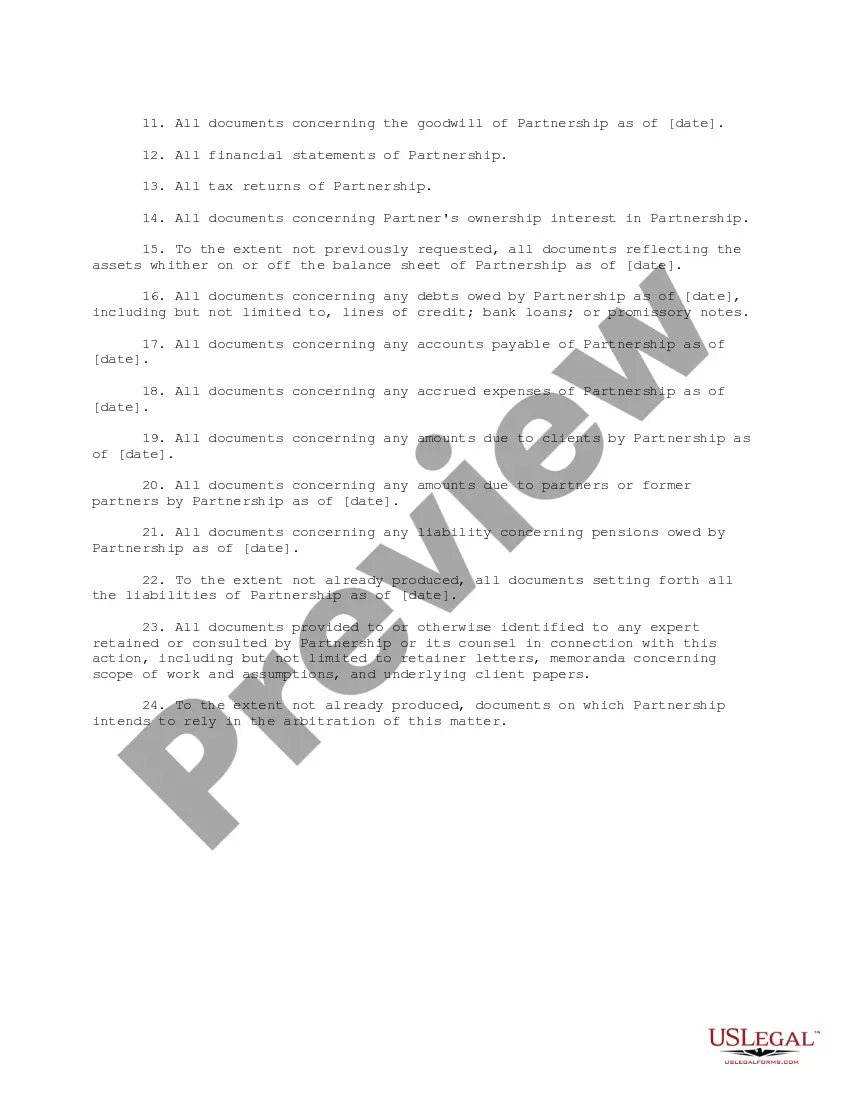

This document is the plaintiff's demand for discovery in a lawsuit filed by a former partner seeking an accounting of his former firm, when the partnership agreement did not provide for an accounting. It contains a request for production of documents.

Vermont Demand for Discovery in an Action for an Accounting is a legal procedure available in the state of Vermont that allows parties involved in an accounting action to obtain crucial information from the opposing party. This type of discovery is specifically related to actions seeking accounting or financial records. A Vermont Demand for Discovery in an Action for an Accounting serves as a means for the requesting party to gain access to relevant documents, records, and information pertaining to the financial transactions and business dealings under scrutiny. It helps parties gather evidence necessary to make informed decisions, present stronger arguments, and potentially uncover any fraudulent activities or mismanagement of funds. Key Types of Vermont Demand for Discovery in an Action for an Accounting: 1. Document Request: This type of demand focuses on obtaining specific documents relevant to the accounting action. It typically includes requests for financial statements, general ledgers, bank records, invoices, receipts, contracts, tax returns, payroll records, and any other materials related to financial transactions or reporting. 2. Interrogatories: Interrogatories are written questions posed to the opposing party that require detailed written answers under oath. In the context of a Vermont Demand for Discovery in an Action for an Accounting, interrogatories may be used to gather information regarding financial practices, business operations, financial institutions used, and any additional data essential for the accounting action. 3. Depositions: Depositions involve taking sworn oral statements from relevant individuals involved in the accounting action. Depositions can be useful in uncovering information that may be difficult to obtain through written requests alone, providing an opportunity for direct questioning and follow-up inquiries. 4. Requests for Admissions: This type of discovery is used to ask the opposing party to admit or deny specific statements of fact related to the accounting action. Requests for Admissions can be a powerful tool to streamline the litigation process by narrowing down disputed issues and potentially eliminating the need for further evidence gathering. It is important to note that the specific requirements and procedures for Vermont Demand for Discovery in an Action for an Accounting can vary depending on the court and jurisdiction. Parties involved in such actions should consult with attorneys familiar with Vermont law to ensure compliance with relevant rules and regulations. In summary, a Vermont Demand for Discovery in an Action for an Accounting is a legal mechanism aimed at acquiring financial information and records pertinent to an accounting action. By utilizing different types of discovery methods, parties can effectively gather evidence, build a strong case, and uncover any discrepancies or misconduct to support their claims.Vermont Demand for Discovery in an Action for an Accounting is a legal procedure available in the state of Vermont that allows parties involved in an accounting action to obtain crucial information from the opposing party. This type of discovery is specifically related to actions seeking accounting or financial records. A Vermont Demand for Discovery in an Action for an Accounting serves as a means for the requesting party to gain access to relevant documents, records, and information pertaining to the financial transactions and business dealings under scrutiny. It helps parties gather evidence necessary to make informed decisions, present stronger arguments, and potentially uncover any fraudulent activities or mismanagement of funds. Key Types of Vermont Demand for Discovery in an Action for an Accounting: 1. Document Request: This type of demand focuses on obtaining specific documents relevant to the accounting action. It typically includes requests for financial statements, general ledgers, bank records, invoices, receipts, contracts, tax returns, payroll records, and any other materials related to financial transactions or reporting. 2. Interrogatories: Interrogatories are written questions posed to the opposing party that require detailed written answers under oath. In the context of a Vermont Demand for Discovery in an Action for an Accounting, interrogatories may be used to gather information regarding financial practices, business operations, financial institutions used, and any additional data essential for the accounting action. 3. Depositions: Depositions involve taking sworn oral statements from relevant individuals involved in the accounting action. Depositions can be useful in uncovering information that may be difficult to obtain through written requests alone, providing an opportunity for direct questioning and follow-up inquiries. 4. Requests for Admissions: This type of discovery is used to ask the opposing party to admit or deny specific statements of fact related to the accounting action. Requests for Admissions can be a powerful tool to streamline the litigation process by narrowing down disputed issues and potentially eliminating the need for further evidence gathering. It is important to note that the specific requirements and procedures for Vermont Demand for Discovery in an Action for an Accounting can vary depending on the court and jurisdiction. Parties involved in such actions should consult with attorneys familiar with Vermont law to ensure compliance with relevant rules and regulations. In summary, a Vermont Demand for Discovery in an Action for an Accounting is a legal mechanism aimed at acquiring financial information and records pertinent to an accounting action. By utilizing different types of discovery methods, parties can effectively gather evidence, build a strong case, and uncover any discrepancies or misconduct to support their claims.