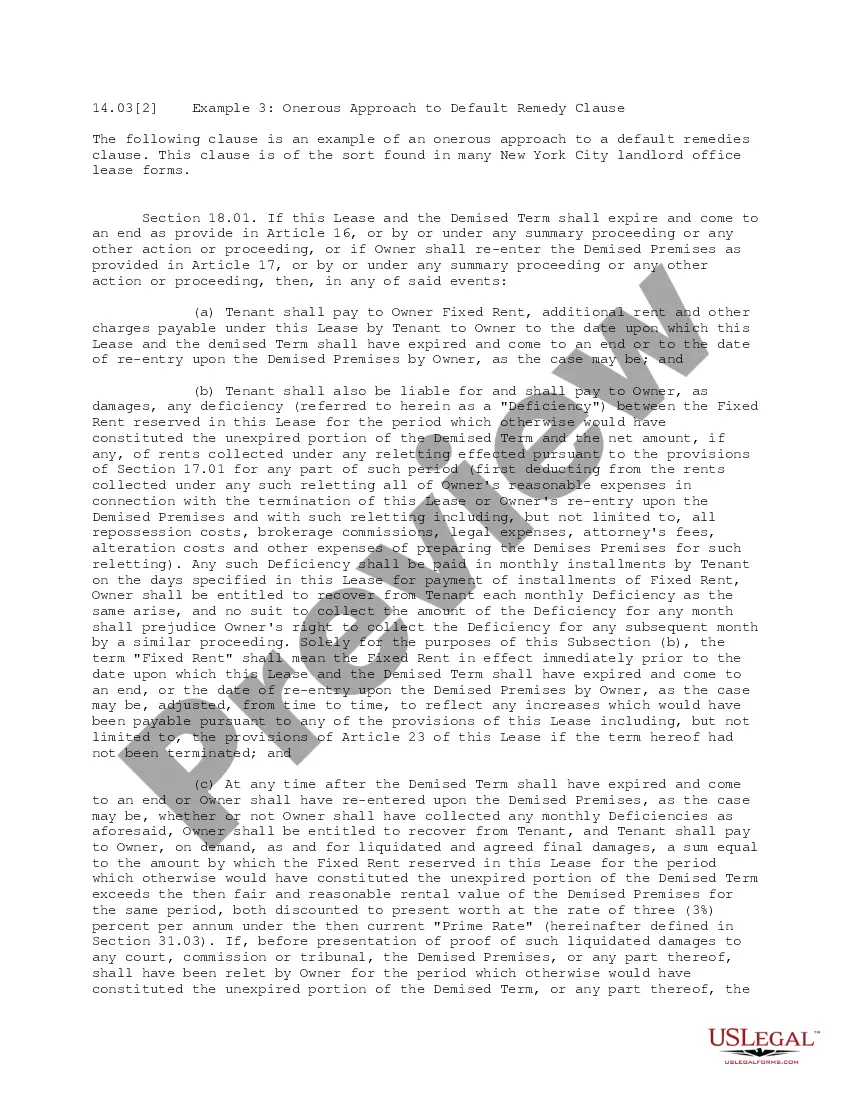

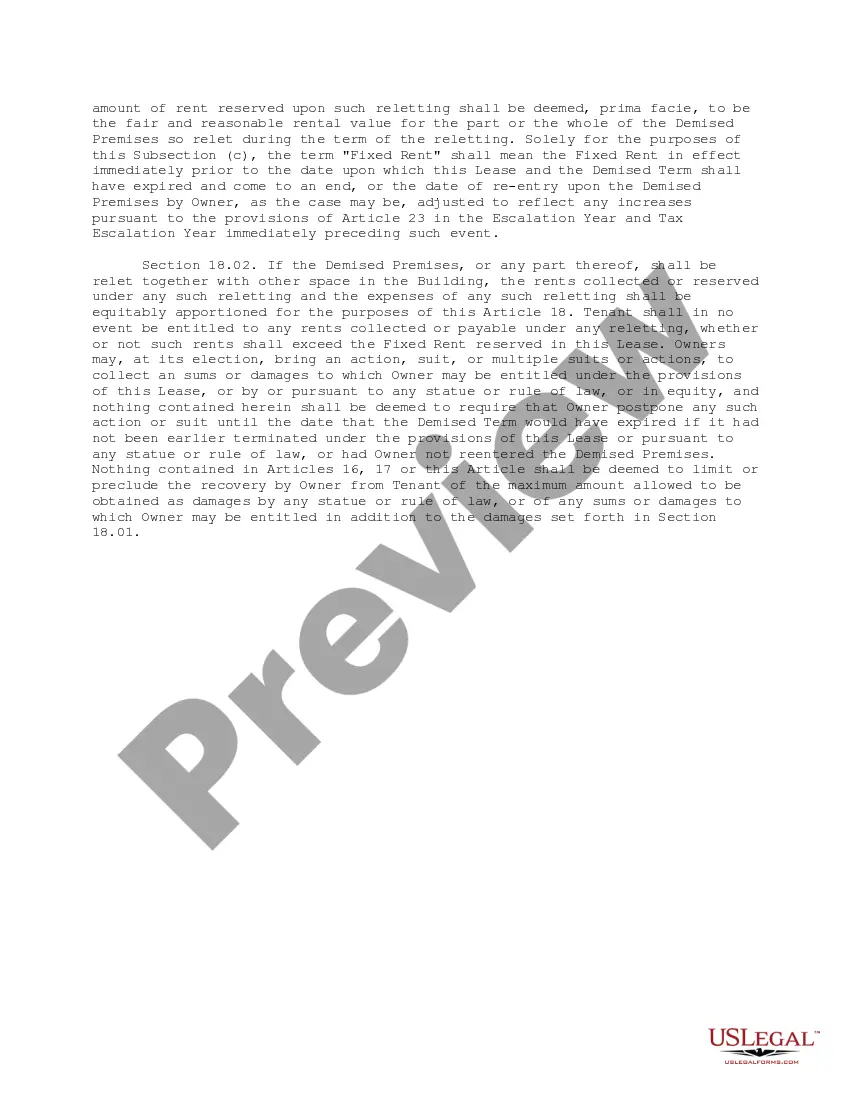

This office lease clause is an onerous approach to a default remedies clause. This clause is similar to those found in many New York City landlord office lease forms.

Title: Understanding Vermont's Onerous Approach to Default Remedy Clause Introduction: Vermont's legal landscape features a unique approach to default remedy clauses, providing crucial safeguards for both borrowers and lenders. In this comprehensive guide, we will delve into the intricacies of Vermont's onerous approach to default remedy clauses, exploring its significance and examining potential variations within this framework. Key Keywords: Vermont, onerous approach, default remedy clause, borrowers, lenders, legal landscape, safeguards, variations. 1. Definition of Vermont's Onerous Approach to Default Remedy Clause: Vermont's onerous approach to default remedy clause refers to specific legal provisions designed to protect borrowers from harsh consequences of loan defaults, while ensuring lenders have appropriate remedies for non-payment or breach of contract. 2. Importance of Default Remedy Clauses: Default remedy clauses play a pivotal role in loan agreements, outlining the rights and remedies available to lenders when a borrower fails to fulfill the contractual obligations. Vermont's onerous approach aims to strike a fair balance between protecting borrowers and maintaining lenders' rights. 3. Safeguards for Borrowers: Vermont's onerous approach offers several safeguards for borrowers, ensuring they are not unduly burdened by default consequences. These safeguards may include limitations on late fees, restrictions on interest rate adjustments, and provisions for meaningful negotiations before initiating foreclosure proceedings. 4. Protection for Lenders: While prioritizing borrower protection, Vermont's onerous approach also recognizes the importance of protecting lenders' interests. The default remedy clause may enable lenders to pursue legal actions, such as foreclosure or repossessing collateral, to recover their investments and mitigate potential losses. 5. Variations within Vermont's Onerous Approach: Although Vermont tends to follow a consistent onerous approach to default remedy clauses, there may be variations depending on the type of loan agreement. Some common variations include: a. Residential Mortgages: In residential mortgage agreements, Vermont may impose additional protections for homeowners, such as mandatory mediation or foreclosure moratoriums. b. Commercial Loans: Commercial loan agreements may have different default remedies compared to residential mortgages, considering the distinct nature and risks associated with commercial borrowing. c. Consumer Protection Laws: Vermont's onerous approach to default remedy clauses may intersect with consumer protection laws, offering enhanced safeguards for vulnerable borrowers. Conclusion: Vermont's onerous approach to default remedy clauses demonstrates a commitment to ensure fairness and protection for both borrowers and lenders. By closely examining the variations within this framework, borrowers and lenders can better navigate loan agreements and understand their rights and obligations, fostering a healthy lending environment in Vermont.Title: Understanding Vermont's Onerous Approach to Default Remedy Clause Introduction: Vermont's legal landscape features a unique approach to default remedy clauses, providing crucial safeguards for both borrowers and lenders. In this comprehensive guide, we will delve into the intricacies of Vermont's onerous approach to default remedy clauses, exploring its significance and examining potential variations within this framework. Key Keywords: Vermont, onerous approach, default remedy clause, borrowers, lenders, legal landscape, safeguards, variations. 1. Definition of Vermont's Onerous Approach to Default Remedy Clause: Vermont's onerous approach to default remedy clause refers to specific legal provisions designed to protect borrowers from harsh consequences of loan defaults, while ensuring lenders have appropriate remedies for non-payment or breach of contract. 2. Importance of Default Remedy Clauses: Default remedy clauses play a pivotal role in loan agreements, outlining the rights and remedies available to lenders when a borrower fails to fulfill the contractual obligations. Vermont's onerous approach aims to strike a fair balance between protecting borrowers and maintaining lenders' rights. 3. Safeguards for Borrowers: Vermont's onerous approach offers several safeguards for borrowers, ensuring they are not unduly burdened by default consequences. These safeguards may include limitations on late fees, restrictions on interest rate adjustments, and provisions for meaningful negotiations before initiating foreclosure proceedings. 4. Protection for Lenders: While prioritizing borrower protection, Vermont's onerous approach also recognizes the importance of protecting lenders' interests. The default remedy clause may enable lenders to pursue legal actions, such as foreclosure or repossessing collateral, to recover their investments and mitigate potential losses. 5. Variations within Vermont's Onerous Approach: Although Vermont tends to follow a consistent onerous approach to default remedy clauses, there may be variations depending on the type of loan agreement. Some common variations include: a. Residential Mortgages: In residential mortgage agreements, Vermont may impose additional protections for homeowners, such as mandatory mediation or foreclosure moratoriums. b. Commercial Loans: Commercial loan agreements may have different default remedies compared to residential mortgages, considering the distinct nature and risks associated with commercial borrowing. c. Consumer Protection Laws: Vermont's onerous approach to default remedy clauses may intersect with consumer protection laws, offering enhanced safeguards for vulnerable borrowers. Conclusion: Vermont's onerous approach to default remedy clauses demonstrates a commitment to ensure fairness and protection for both borrowers and lenders. By closely examining the variations within this framework, borrowers and lenders can better navigate loan agreements and understand their rights and obligations, fostering a healthy lending environment in Vermont.