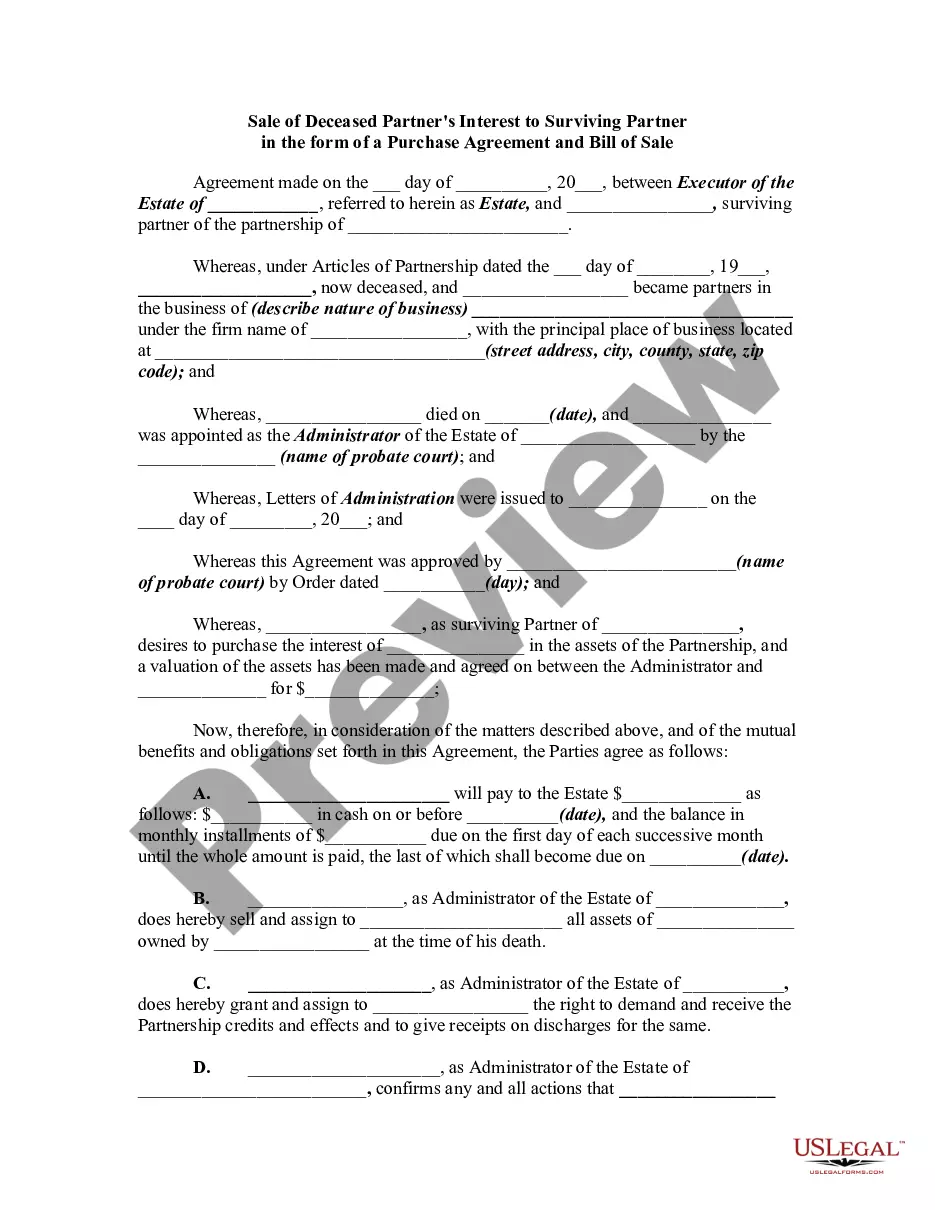

Keywords: Washington, Sale of Deceased Partner's Interest, Surviving Partner, Purchase Agreement, Bill of Sale. Title: Washington Sale of Deceased Partner's Interest to Surviving Partner: Understanding the Purchase Agreement and Bill of Sale Introduction: In the state of Washington, when a partner in a business entity passes away, their interest in the partnership must be transferred to the surviving partner. This is typically done through a Sale of Deceased Partner's Interest to the Surviving Partner, facilitated by a Purchase Agreement and Bill of Sale. In this article, we will explore the details of this process, including its types and key considerations. I. Types of Washington Sale of Deceased Partner's Interest to Surviving Partner: 1. Voluntary Agreement: In some cases, surviving partners may reach a voluntary agreement amongst themselves to allocate and purchase the deceased partner's interest. This type of arrangement allows for flexibility and can be customized to the specific needs and conditions of the partners involved. 2. Partnership Agreement Provisions: Partnerships often have detailed provisions outlined in their partnership agreements regarding the sale of a deceased partner's interest. These provisions may dictate specific procedures, valuation methods, and terms for the sale. It's crucial to review the partnership agreement to determine the applicable rules and processes. II. Purchase Agreement: The Purchase Agreement is a legally binding document that establishes the terms and conditions of the sale between the surviving partner(s) and the deceased partner's estate or representative. Key elements of the Purchase Agreement include: 1. Purchase Price and Payment Terms: The agreement should outline the agreed-upon purchase price for the deceased partner's interest. Payment terms, such as lump sum payment or installment plans, must be clearly specified. 2. Valuation Method: The Purchase Agreement should determine the valuation method for the deceased partner's interest. Common methods include book value, fair market value, or a pre-determined formula outlined in the partnership agreement. 3. Representation and Warranties: Both parties must disclose any material information relevant to the sale. Representations and warranties protect the buyer from potential undisclosed liabilities or encumbrances associated with the deceased partner's interest. III. Bill of Sale: The Bill of Sale is a legal document that confirms the transfer of the deceased partner's interest to the surviving partner(s). It serves as proof of ownership and protects the buyer's rights. Key details included in the Bill of Sale are: 1. Identification of Parties: The Bill of Sale should clearly identify the seller (deceased partner's estate or representative) and the buyer (surviving partner(s)). 2. Description of Interest: The document should provide a detailed description of the deceased partner's interest being transferred, including any specific rights or limitations associated with it. 3. Consideration Paid: The Bill of Sale must state the consideration provided by the buyer in exchange for the deceased partner's interest. Conclusion: When a partner passes away, a Sale of Deceased Partner's Interest to the Surviving Partner is crucial for the continuity of the business. In Washington, this process is typically executed through a Purchase Agreement and documented with a Bill of Sale. Understanding the types, clauses, and legal requirements involved is essential for a smooth transition and protection of the surviving partner's rights. Consulting with legal professionals experienced in partnership matters can ensure compliance with Washington state laws and the partnership agreement, if applicable.

Washington Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Description

How to fill out Washington Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

Are you presently in the situation the place you will need files for either company or individual functions just about every time? There are a lot of lawful file templates available online, but getting kinds you can rely isn`t straightforward. US Legal Forms gives 1000s of form templates, such as the Washington Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale, that are created to fulfill federal and state demands.

When you are previously informed about US Legal Forms internet site and get a merchant account, just log in. Following that, you can download the Washington Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale format.

Unless you have an bank account and need to start using US Legal Forms, follow these steps:

- Discover the form you will need and make sure it is to the proper town/region.

- Make use of the Review switch to analyze the shape.

- See the information to actually have selected the appropriate form.

- In case the form isn`t what you`re searching for, make use of the Lookup area to find the form that meets your needs and demands.

- When you find the proper form, click Acquire now.

- Choose the rates prepare you would like, complete the desired info to produce your bank account, and purchase an order with your PayPal or credit card.

- Pick a convenient paper format and download your copy.

Locate all of the file templates you may have purchased in the My Forms menu. You can aquire a more copy of Washington Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale at any time, if possible. Just click on the required form to download or print out the file format.

Use US Legal Forms, by far the most extensive collection of lawful varieties, to save lots of efforts and steer clear of mistakes. The service gives professionally made lawful file templates that can be used for an array of functions. Make a merchant account on US Legal Forms and commence creating your lifestyle easier.