Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

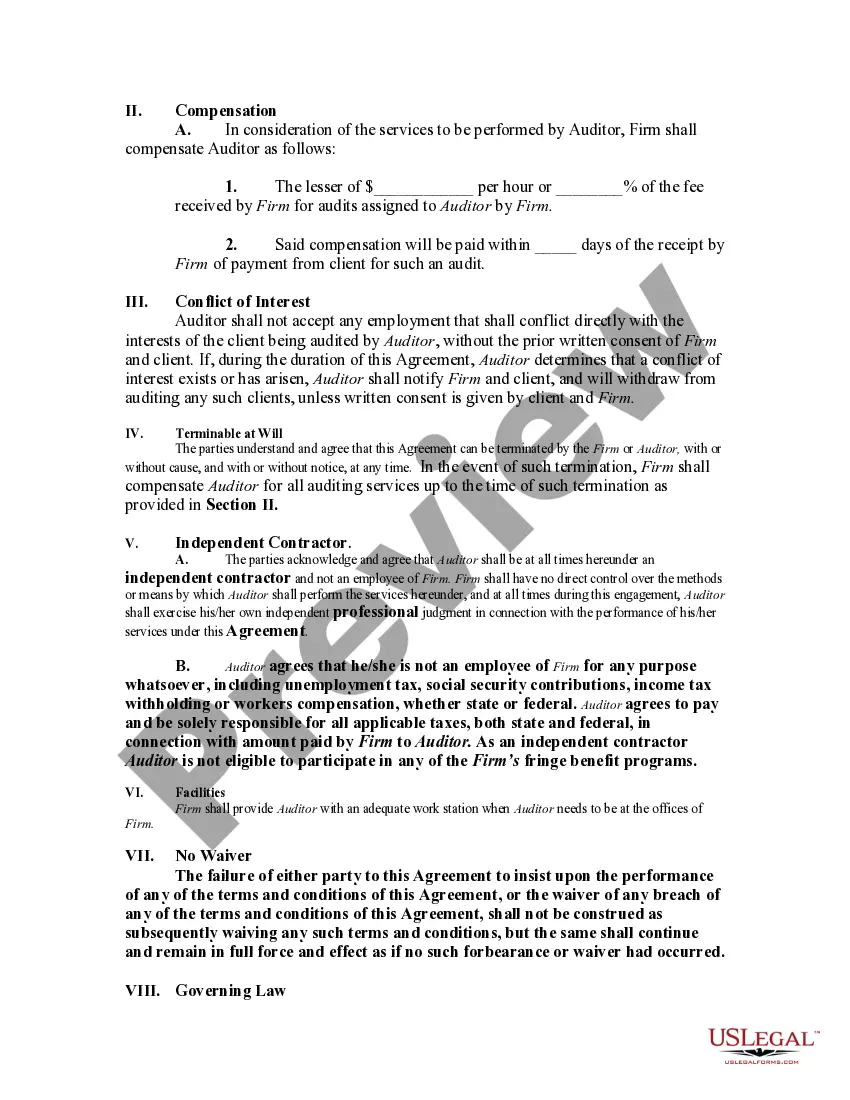

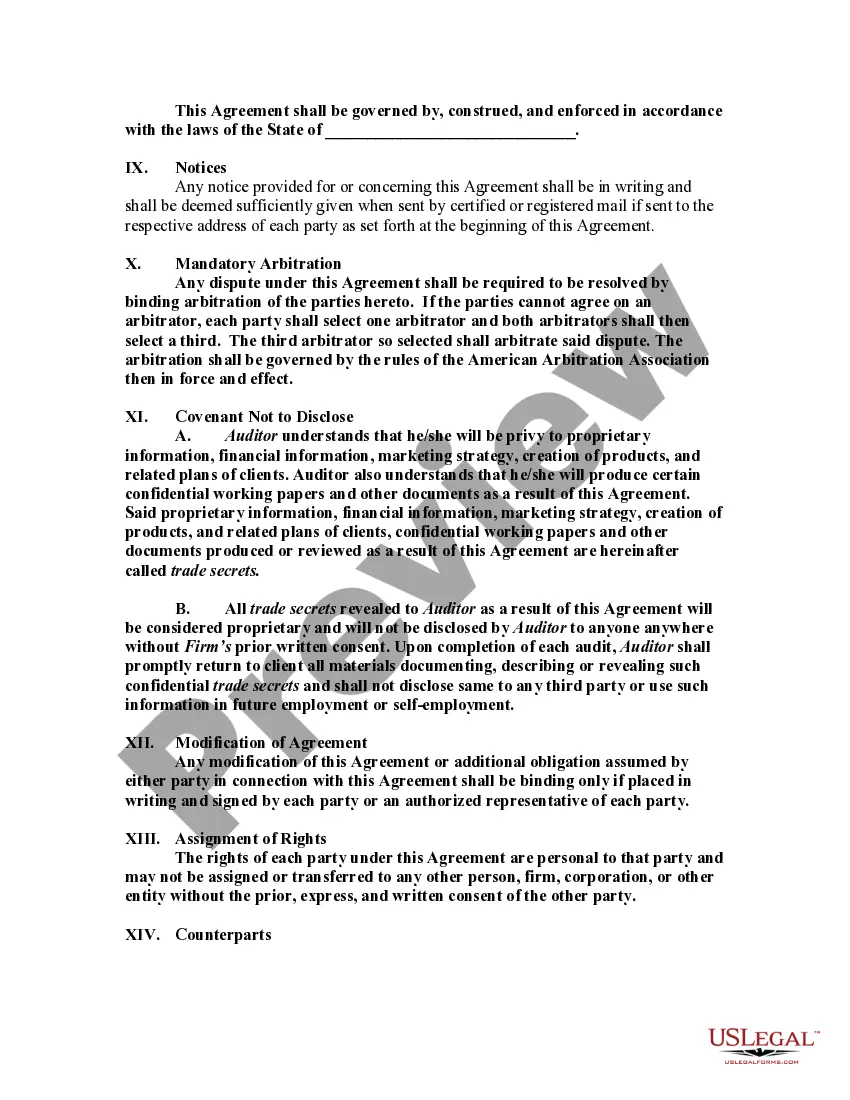

Description: A Washington Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that outlines the terms and conditions between an accounting firm and an auditor who is hired as a self-employed independent contractor in the state of Washington, USA. This agreement ensures that both parties understand their rights, responsibilities, and obligations during their professional engagement. In this agreement, the accounting firm acknowledges that the auditor is functioning as a self-employed independent contractor and not as an employee. The agreement highlights the nature of the working relationship, defined by the Washington state laws governing such arrangements. This distinction is crucial as it establishes the auditor's status as an independent contractor, emphasizing that no employer-employee relationship exists. The Washington Agreement specifies various components, which may include: 1. Scope of Work: It clearly defines the services the auditor will perform. This might encompass audits, financial reviews, or any other agreed-upon assignments. 2. Compensation: The agreement outlines the payment structure and method, such as a fixed fee or hourly rate, along with any additional incentives or bonuses. 3. Duration: The agreement states the start and end dates or duration of the engagement, ensuring that both parties understand the timeline for the services to be rendered. 4. Responsibility for Expenses: It clarifies which party shall bear the expenses related to the auditor's work, such as travel costs, office supplies, or equipment. Typically, the independent contractor carries these expenses. 5. Compliance with Laws: This clause highlights that both parties must adhere to all applicable laws and regulations, including those regarding taxation, licensing, and professional ethics. 6. Confidentiality: The agreement may include provisions to protect confidential information the auditor may come across during their work, ensuring compliance with privacy laws and ethical guidelines. 7. Termination: Terms for terminating the agreement, such as a notice period or conditions for termination, are outlined. This protects the interests of both the accounting firm and the auditor. Furthermore, there might be different types of Washington Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor, depending on various factors such as the size of the accounting firm, specific industry requirements, or the complexity of services required. However, regardless of the variations, the core elements mentioned above usually remain consistent. It is essential for both the accounting firm and the auditor to carefully review these terms before signing the agreement, ensuring a comprehensive understanding and a mutually beneficial working relationship.Description: A Washington Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that outlines the terms and conditions between an accounting firm and an auditor who is hired as a self-employed independent contractor in the state of Washington, USA. This agreement ensures that both parties understand their rights, responsibilities, and obligations during their professional engagement. In this agreement, the accounting firm acknowledges that the auditor is functioning as a self-employed independent contractor and not as an employee. The agreement highlights the nature of the working relationship, defined by the Washington state laws governing such arrangements. This distinction is crucial as it establishes the auditor's status as an independent contractor, emphasizing that no employer-employee relationship exists. The Washington Agreement specifies various components, which may include: 1. Scope of Work: It clearly defines the services the auditor will perform. This might encompass audits, financial reviews, or any other agreed-upon assignments. 2. Compensation: The agreement outlines the payment structure and method, such as a fixed fee or hourly rate, along with any additional incentives or bonuses. 3. Duration: The agreement states the start and end dates or duration of the engagement, ensuring that both parties understand the timeline for the services to be rendered. 4. Responsibility for Expenses: It clarifies which party shall bear the expenses related to the auditor's work, such as travel costs, office supplies, or equipment. Typically, the independent contractor carries these expenses. 5. Compliance with Laws: This clause highlights that both parties must adhere to all applicable laws and regulations, including those regarding taxation, licensing, and professional ethics. 6. Confidentiality: The agreement may include provisions to protect confidential information the auditor may come across during their work, ensuring compliance with privacy laws and ethical guidelines. 7. Termination: Terms for terminating the agreement, such as a notice period or conditions for termination, are outlined. This protects the interests of both the accounting firm and the auditor. Furthermore, there might be different types of Washington Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor, depending on various factors such as the size of the accounting firm, specific industry requirements, or the complexity of services required. However, regardless of the variations, the core elements mentioned above usually remain consistent. It is essential for both the accounting firm and the auditor to carefully review these terms before signing the agreement, ensuring a comprehensive understanding and a mutually beneficial working relationship.