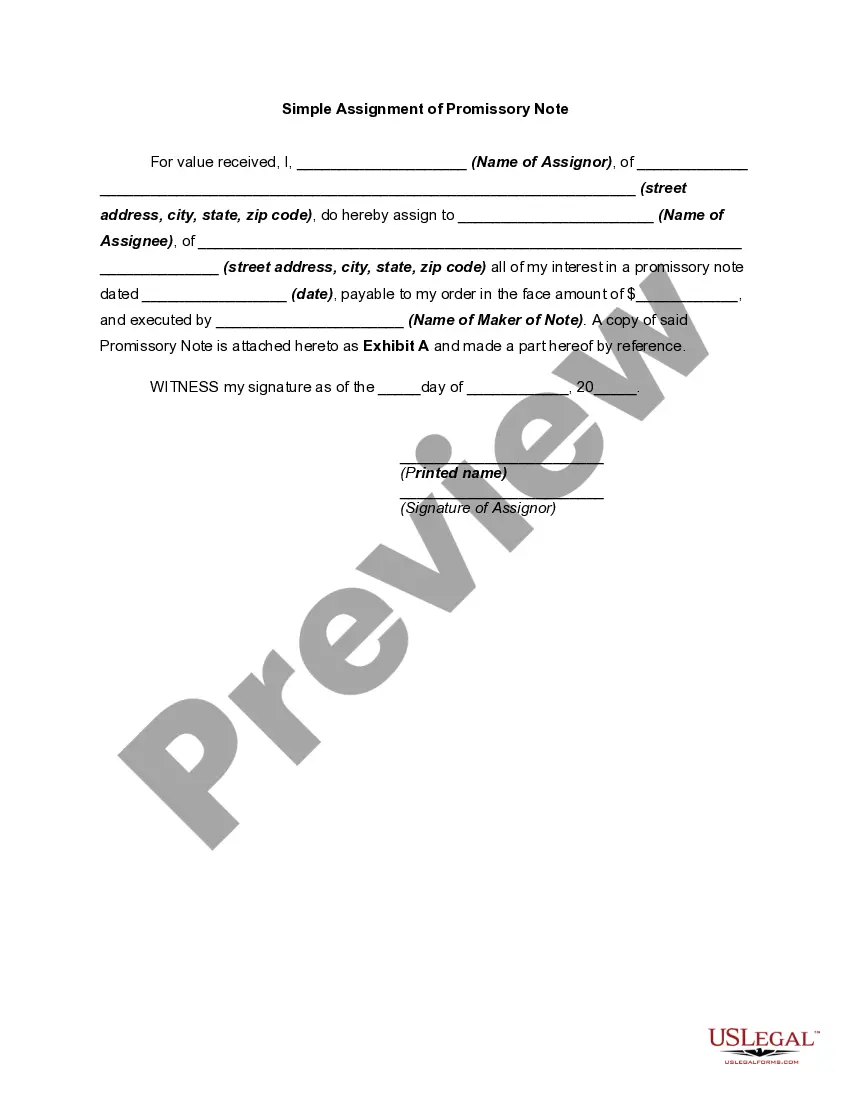

A Washington Simple Promissory Note for Family Loan is a legally binding document that outlines the details of a loan agreement between family members in the state of Washington. This promissory note establishes the terms and conditions under which a borrower promises to repay the lender the borrowed amount, along with any accrued interest, in a specified time frame. The Washington Simple Promissory Note for Family Loan serves as a written record of the loan agreement, protecting both the borrower and lender by ensuring clarity and preventing any misunderstandings or disputes in the future. This document is essential for maintaining good relationships within a family while formalizing the loan transaction. Key elements included in a typical Washington Simple Promissory Note for Family Loan are: 1. Loan Amount: This specifies the total amount of money borrowed by the borrower from the lender. 2. Interest Rate: The interest rate, if applicable, is agreed upon and stated in the note. Typically, loans within families have lower or no interest rates compared to traditional loans. 3. Repayment Terms: The note defines the repayment schedule, including the dates and amounts of periodic payments the borrower must make towards the loan. 4. Late Payment Penalties: If the borrower fails to make timely payments, there may be penalties or fees outlined in the note. 5. Events of Default: This section mentions actions or situations that could lead to loan default, such as bankruptcy or breach of terms. 6. Collateral: If the loan is secured by collateral, such as property or assets, the details of the collateral will be specified in the note. It is important to note that the Washington Simple Promissory Note for Family Loan can be customized to fit the specific needs of the parties involved. The Washington State laws govern these promissory notes, and it is crucial to ensure the document complies with these regulations. Different types of Washington Simple Promissory Notes for Family Loan may vary based on factors such as loan amount, interest rate, repayment terms, and whether the loan is secured or unsecured. These variations allow for flexibility in tailoring the promissory note to suit the unique circumstances of the family loan transaction. It is advisable to consult with a legal professional to ensure compliance with the appropriate laws and to properly document the loan agreement.

Washington Simple Promissory Note for Family Loan

Description

How to fill out Washington Simple Promissory Note For Family Loan?

If you wish to comprehensive, obtain, or print out legal document themes, use US Legal Forms, the greatest collection of legal varieties, which can be found on the Internet. Make use of the site`s simple and practical lookup to obtain the paperwork you require. Various themes for business and person purposes are categorized by types and states, or search phrases. Use US Legal Forms to obtain the Washington Simple Promissory Note for Family Loan with a handful of click throughs.

When you are already a US Legal Forms buyer, log in to the bank account and click on the Acquire option to find the Washington Simple Promissory Note for Family Loan. You can also accessibility varieties you formerly saved inside the My Forms tab of your bank account.

If you work with US Legal Forms initially, follow the instructions listed below:

- Step 1. Be sure you have selected the shape for your appropriate city/region.

- Step 2. Use the Review choice to check out the form`s articles. Do not neglect to read through the information.

- Step 3. When you are unsatisfied with all the form, use the Research field on top of the display to discover other variations of your legal form template.

- Step 4. When you have identified the shape you require, click the Purchase now option. Pick the prices prepare you like and include your accreditations to register on an bank account.

- Step 5. Process the purchase. You may use your bank card or PayPal bank account to perform the purchase.

- Step 6. Pick the formatting of your legal form and obtain it on the system.

- Step 7. Complete, change and print out or signal the Washington Simple Promissory Note for Family Loan.

Every legal document template you purchase is your own permanently. You may have acces to every form you saved with your acccount. Click on the My Forms area and choose a form to print out or obtain yet again.

Be competitive and obtain, and print out the Washington Simple Promissory Note for Family Loan with US Legal Forms. There are thousands of specialist and condition-specific varieties you can utilize to your business or person demands.

Form popularity

FAQ

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

Pros. Easier approval: There's typically no formal application process, credit check or verification of income when you're borrowing from family. Traditional lenders often require documents such as W-2s, pay stubs and tax forms as part of the loan application process.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

A personal loan agreement should include the following information:Names and addresses of the lender and the borrower.Information about the loan cosigner, if applicable.Amount borrowed.Date the loan was provided.Expected repayment date.Interest rate, if applicable.Annual percentage rate (APR), if applicable.More items...?

A Washington promissory note does not need to be notarized. To execute the note, the borrower should sign and date it. If there is a co-signer, the co-signer should also sign and date the document.

The name and address of the person loaning the money. The name and address of the person borrowing the money. Terms of repayment: schedule of repayment, amount of each payment and manner of payments (in-person, cash, check, etc.) Interest to be charged related to the loan, if any.

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

To draft a Loan Agreement, you should include the following:The addresses and contact information of all parties involved.The conditions of use of the loan (what the money can be used for)Any repayment options.The payment schedule.The interest rates.The length of the term.Any collateral.The cancellation policy.More items...

More info

Miles is used in business or family business loans.