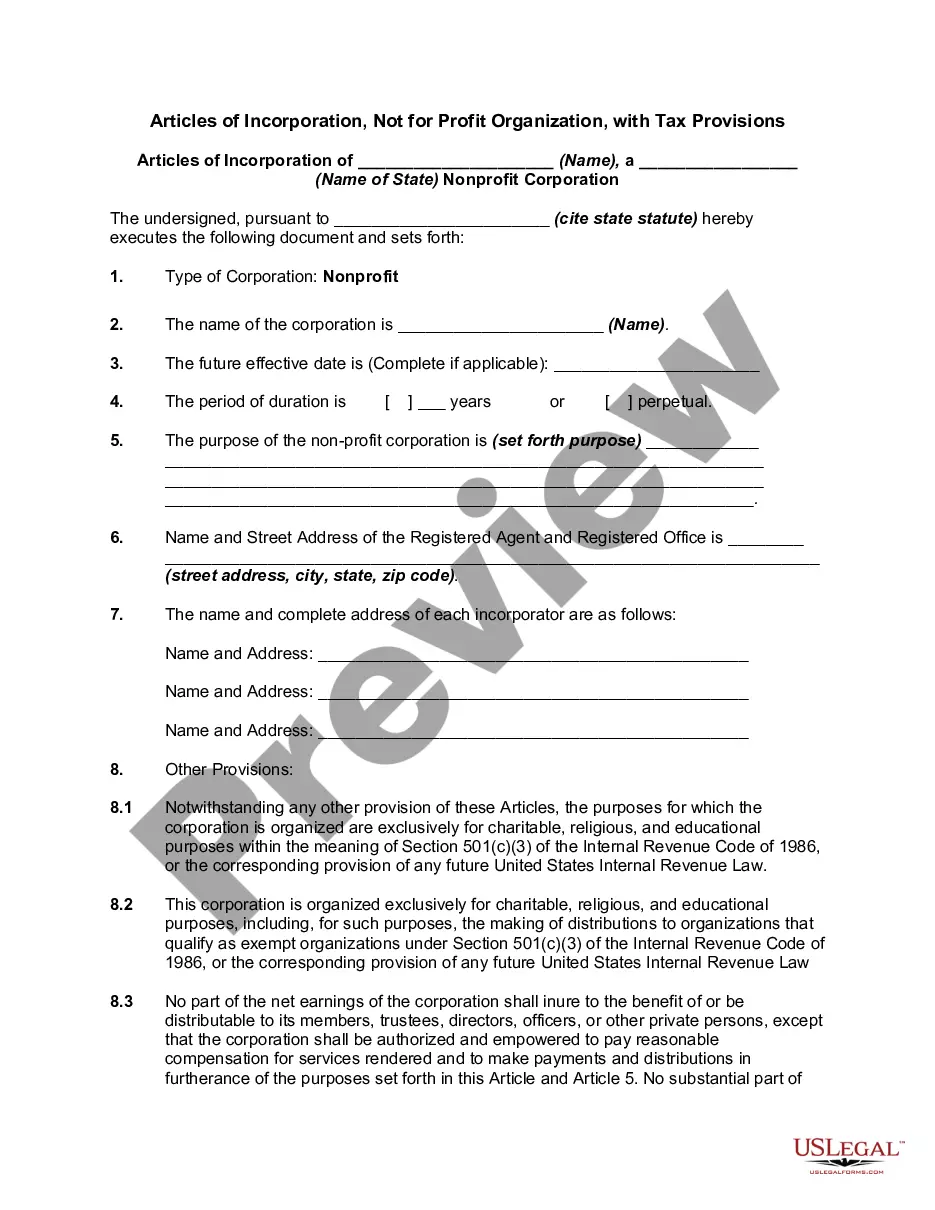

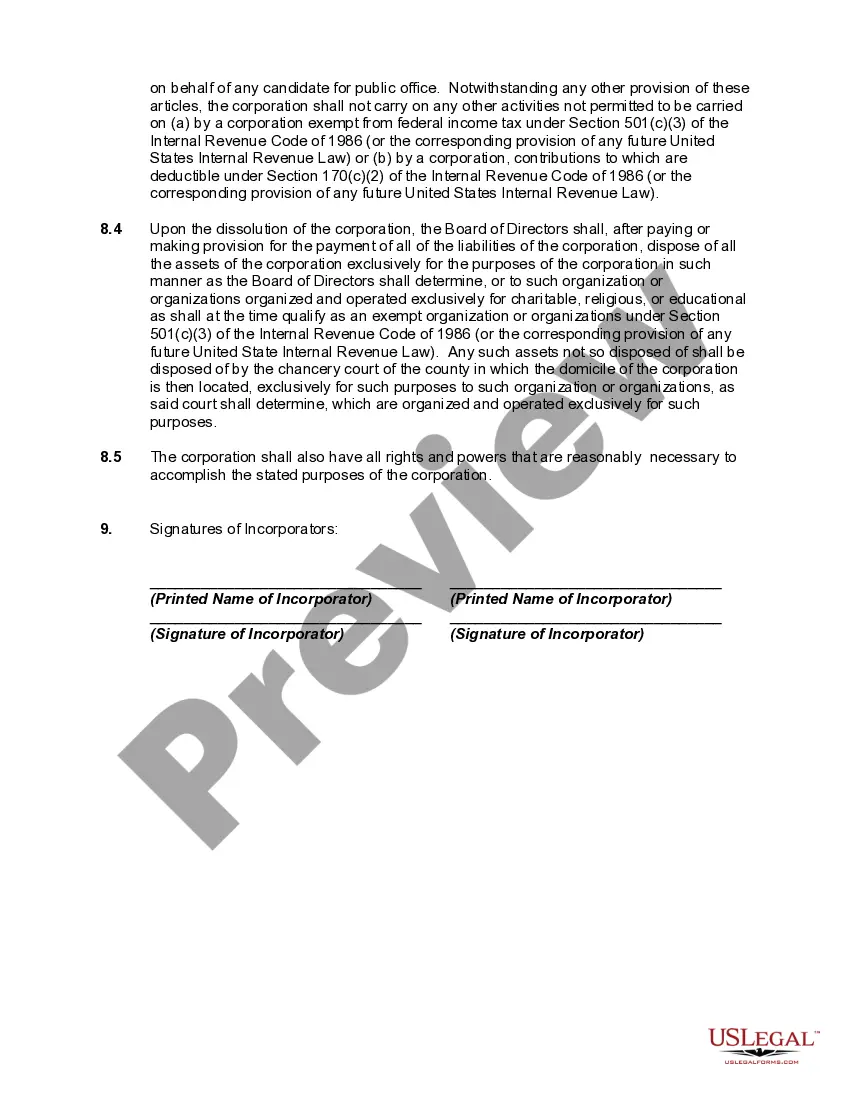

The Washington Articles of Incorporation are legal documents that must be filed with the Washington Secretary of State in order to establish a not-for-profit organization operating within the state. These articles outline the basic information about the organization, its purpose, and its structure. When establishing a not-for-profit organization through the Washington Articles of Incorporation, there are specific tax provisions that must be considered. These provisions ensure that the organization adheres to the necessary regulations in order to maintain its tax-exempt status. Some relevant keywords related to this topic could include: 1. Washington Secretary of State: The government department responsible for overseeing the registration and regulation of businesses and nonprofit organizations in the state of Washington. 2. Articles of Incorporation: The legal document that establishes a not-for-profit organization as a separate legal entity. It contains information such as the name of the organization, its purpose, and its registered agent. 3. Not-for-profit organization: An organization that operates for purposes other than generating profit, such as charitable, educational, or religious activities. These organizations are exempt from paying certain taxes. 4. Tax provisions: Specific regulations and requirements that not-for-profit organizations must comply with to maintain their tax-exempt status. These provisions include rules related to fundraising, reporting, and financial transparency. 5. Tax-exempt status: The status granted to organizations by the Internal Revenue Service (IRS) that exempts them from paying federal income tax. To maintain this status, organizations must meet certain criteria and adhere to specific regulations. Different types of Washington Articles of Incorporation for not-for-profit organizations with tax provisions can include: 1. General not-for-profit organization: This is the most common type of not-for-profit organization, which includes a broad range of charitable, educational, and religious organizations. 2. Religious or faith-based organization: These organizations have a primary religious or faith-based purpose and may have specific tax provisions and regulations unique to their religious activities. 3. Educational institution: Institutions such as schools, colleges, or universities may have specific articles of incorporation tailored to their educational mission, including provisions related to tuition, scholarships, and grants. 4. Charitable foundation: Organizations focused on charitable activities, such as providing assistance to the less fortunate, may have specific articles of incorporation designed to reflect their charitable purpose and tax-exempt status. 5. Social welfare organization: These organizations work towards promoting the common good and addressing social issues. They may have specific articles of incorporation to address their specific focus areas and tax requirements. It is important to consult with legal professionals or experts in not-for-profit law to ensure that the articles of incorporation and tax provisions align with the organization's specific goals and comply with all applicable laws and regulations.

Washington Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Washington Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

If you need to complete, obtain, or produce authorized file templates, use US Legal Forms, the biggest selection of authorized kinds, which can be found on-line. Make use of the site`s basic and practical look for to find the files you require. A variety of templates for organization and person functions are sorted by classes and suggests, or search phrases. Use US Legal Forms to find the Washington Articles of Incorporation, Not for Profit Organization, with Tax Provisions in just a handful of clicks.

Should you be already a US Legal Forms buyer, log in for your account and then click the Down load switch to get the Washington Articles of Incorporation, Not for Profit Organization, with Tax Provisions. You may also access kinds you formerly acquired inside the My Forms tab of your own account.

Should you use US Legal Forms initially, follow the instructions under:

- Step 1. Make sure you have chosen the shape for that appropriate area/land.

- Step 2. Make use of the Review method to look through the form`s content. Never overlook to see the information.

- Step 3. Should you be unhappy using the kind, make use of the Search field near the top of the display to discover other types of the authorized kind web template.

- Step 4. Once you have discovered the shape you require, go through the Purchase now switch. Pick the prices prepare you favor and include your accreditations to sign up for an account.

- Step 5. Method the financial transaction. You may use your bank card or PayPal account to accomplish the financial transaction.

- Step 6. Pick the formatting of the authorized kind and obtain it on your product.

- Step 7. Total, edit and produce or signal the Washington Articles of Incorporation, Not for Profit Organization, with Tax Provisions.

Each and every authorized file web template you acquire is yours forever. You may have acces to every kind you acquired inside your acccount. Click the My Forms portion and decide on a kind to produce or obtain yet again.

Compete and obtain, and produce the Washington Articles of Incorporation, Not for Profit Organization, with Tax Provisions with US Legal Forms. There are millions of skilled and condition-certain kinds you can use for your personal organization or person requirements.