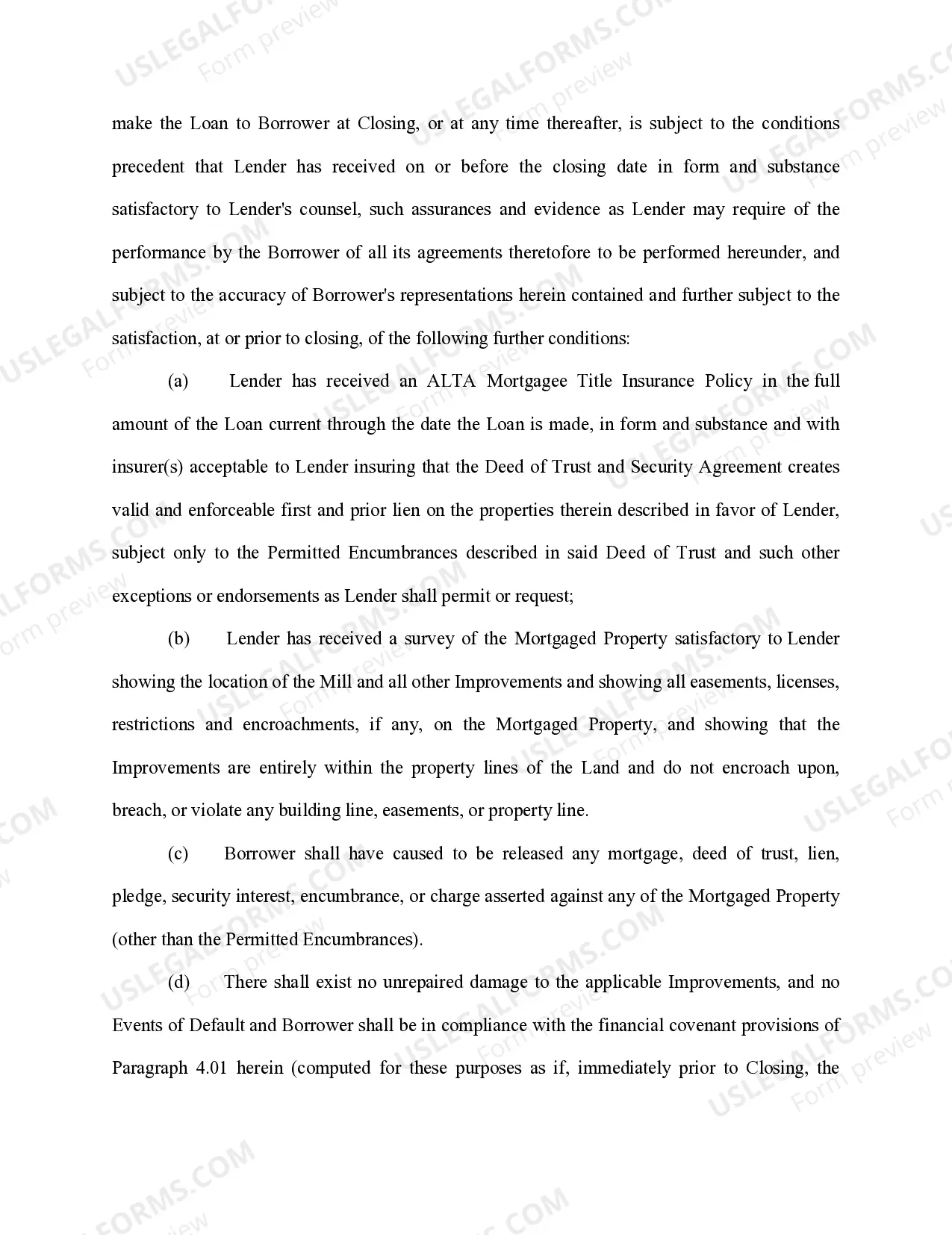

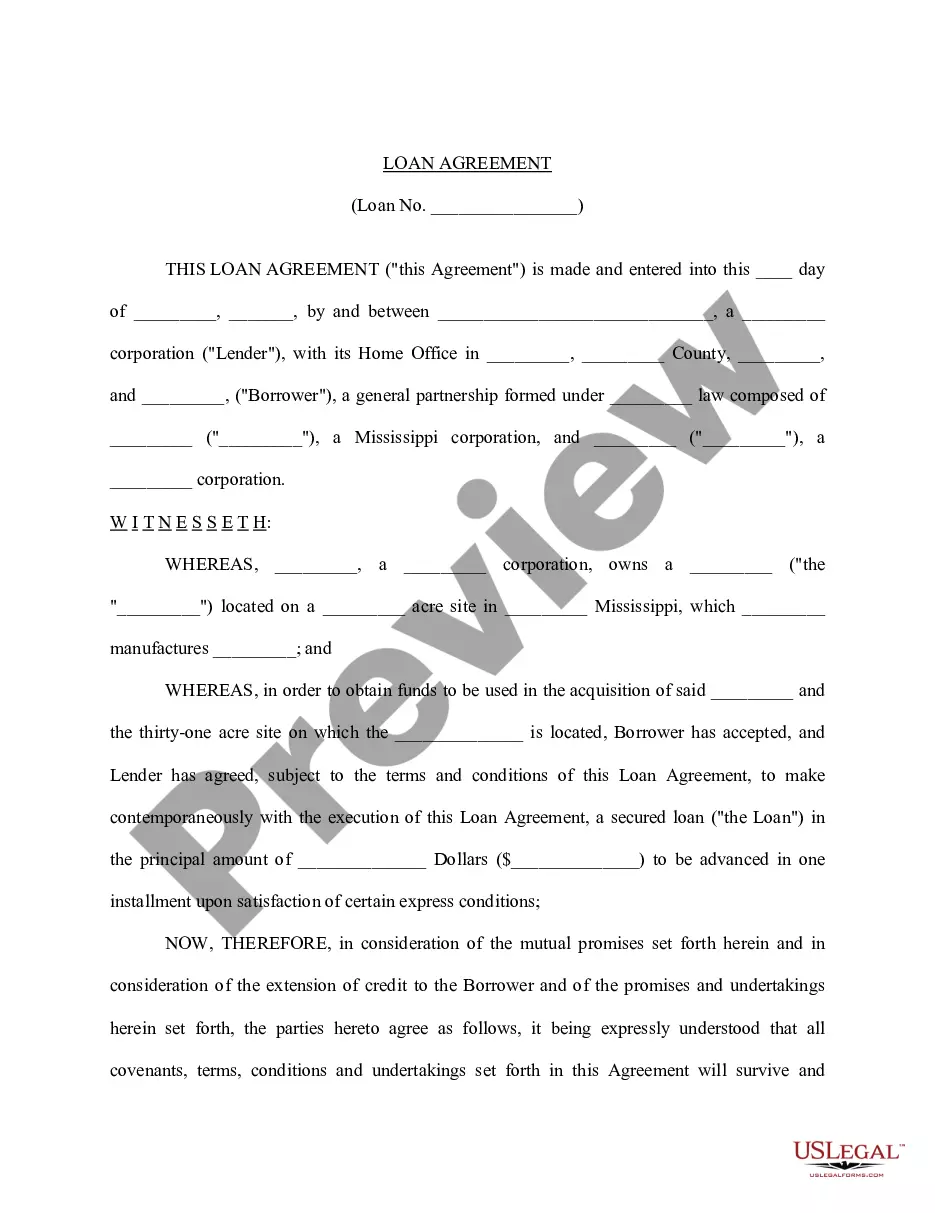

The Washington Loan Agreement for Personal Loan is a legally binding document that outlines the terms and conditions of a loan between a lender and a borrower in the state of Washington. This agreement serves as a crucial tool to establish clear financial expectations and protect the rights of both parties involved. The agreement typically includes several key elements such as: 1. Loan amount: Specifies the total amount of money being borrowed by the borrower from the lender. 2. Interest rate: States the percentage rate at which interest will be applied to the loan amount, determining the cost of borrowing. 3. Repayment terms: Outlines the schedule and method of repayment, including the installment amounts, frequency, and duration of the loan. 4. Late payment penalties: Details the consequences and additional charges if the borrower fails to make timely payments or defaults on the loan. 5. Collateral: Discusses whether collateral is required to secure the loan and, if so, describes the assets that may be used as security. 6. Loan purpose: Indicates the reason for borrowing the funds, such as debt consolidation, medical expenses, education, or any other personal need. 7. Signatures: Requires the signatures of both the lender and borrower, confirming their agreement to the terms and conditions mentioned in the document. In Washington state, there are different types of loan agreements for personal loans, including: 1. Fixed-term personal loan agreement: This type of agreement specifies a predetermined loan term with fixed interest rates and installment amounts. It provides both parties with a clear understanding of the repayment period. 2. Revolving credit loan agreement: In this agreement, the lender establishes a credit limit for the borrower, allowing them to access funds as needed, up to the set limit. Interest is usually charged only on the amount borrowed and repayments can be made flexibly. 3. Secured personal loan agreement: This type of agreement requires the borrower to provide collateral, such as a house or a car, which can be seized by the lender in case of default. The presence of collateral often allows for lower interest rates. 4. Unsecured personal loan agreement: Unlike secured agreements, this type of loan does not require collateral. In such cases, the lender relies mainly on the borrower's creditworthiness, resulting in higher interest rates due to the increased risk. It is essential for both the lender and borrower to carefully review and understand the terms and conditions set forth in the Washington Loan Agreement for Personal Loan before signing. Seeking legal advice or financial counseling may be beneficial to ensure that the terms are fair, transparent, and suitable for both parties' needs.

Washington Loan Agreement for Personal Loan

Description

How to fill out Washington Loan Agreement For Personal Loan?

If you need to full, download, or print legal file web templates, use US Legal Forms, the largest selection of legal types, that can be found online. Utilize the site`s simple and easy practical research to obtain the papers you will need. A variety of web templates for enterprise and person functions are categorized by classes and claims, or search phrases. Use US Legal Forms to obtain the Washington Loan Agreement for Personal Loan in a number of mouse clicks.

If you are already a US Legal Forms customer, log in to the bank account and then click the Acquire button to have the Washington Loan Agreement for Personal Loan. You can also gain access to types you formerly acquired within the My Forms tab of your respective bank account.

Should you use US Legal Forms the very first time, follow the instructions under:

- Step 1. Be sure you have chosen the shape for that appropriate metropolis/country.

- Step 2. Make use of the Review method to examine the form`s content material. Never forget about to learn the information.

- Step 3. If you are unsatisfied together with the kind, utilize the Lookup field towards the top of the display screen to locate other models of your legal kind template.

- Step 4. After you have found the shape you will need, go through the Get now button. Opt for the prices program you prefer and add your references to sign up for an bank account.

- Step 5. Method the deal. You can use your Мisa or Ьastercard or PayPal bank account to accomplish the deal.

- Step 6. Choose the formatting of your legal kind and download it on the product.

- Step 7. Full, modify and print or signal the Washington Loan Agreement for Personal Loan.

Each legal file template you get is yours for a long time. You possess acces to each kind you acquired within your acccount. Select the My Forms portion and decide on a kind to print or download once more.

Remain competitive and download, and print the Washington Loan Agreement for Personal Loan with US Legal Forms. There are many expert and condition-distinct types you may use for your personal enterprise or person demands.