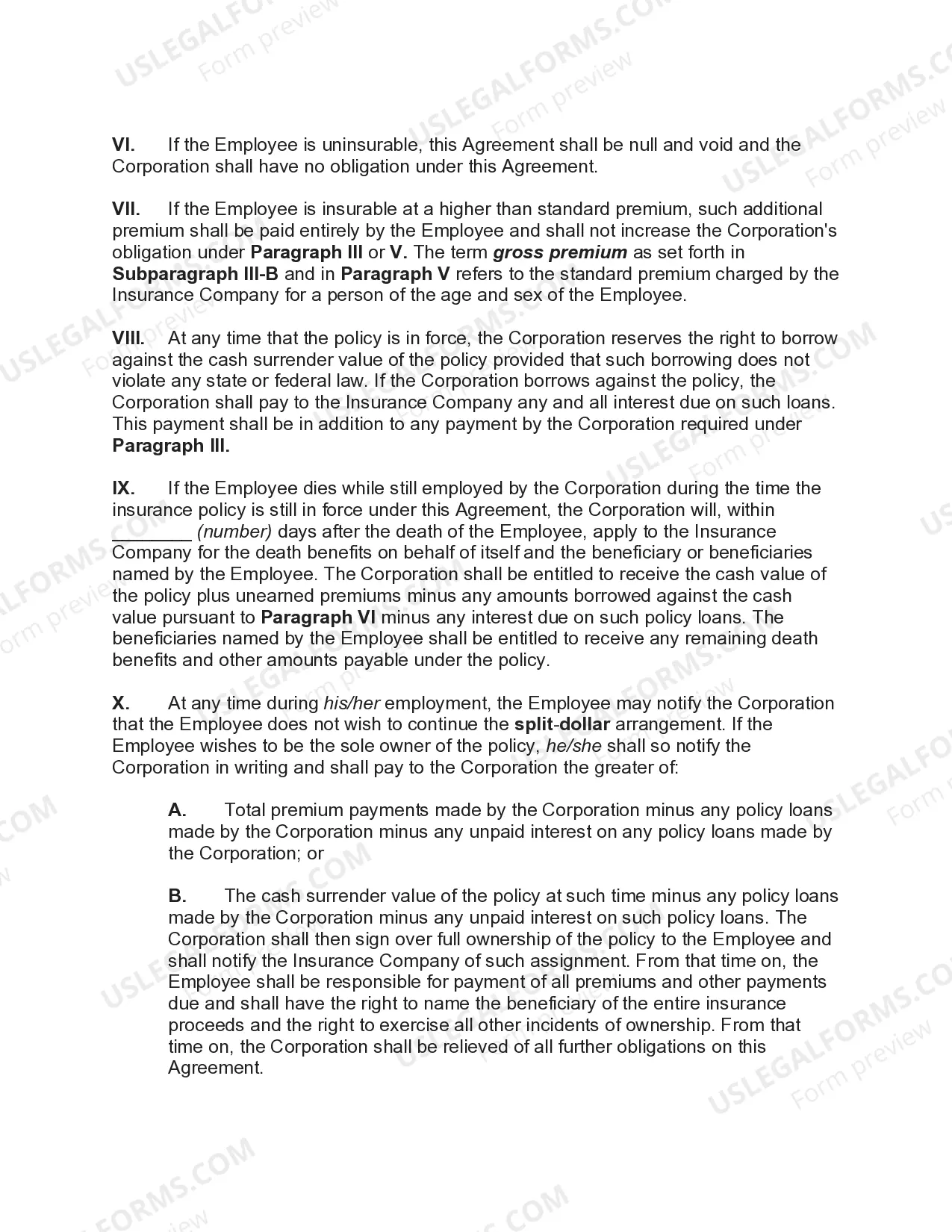

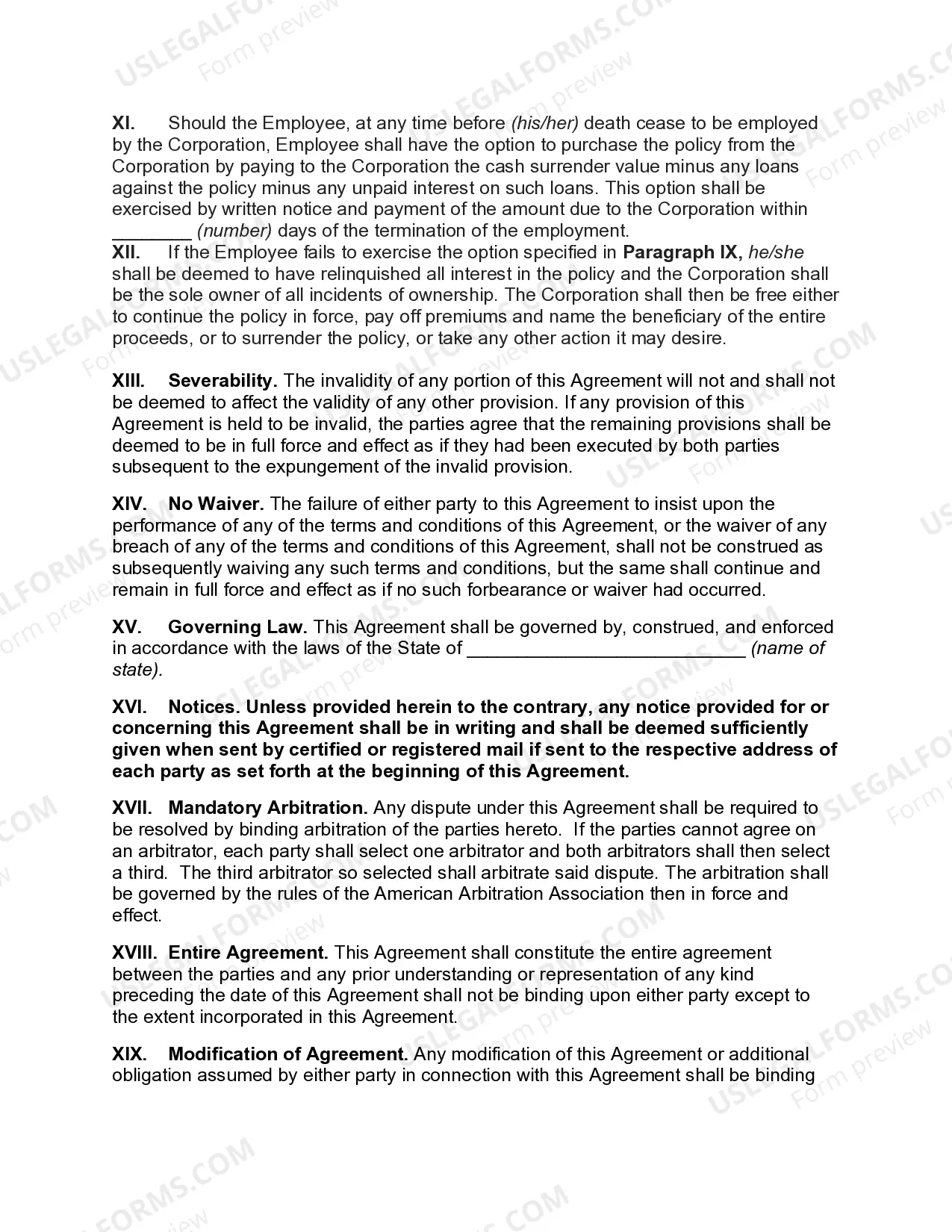

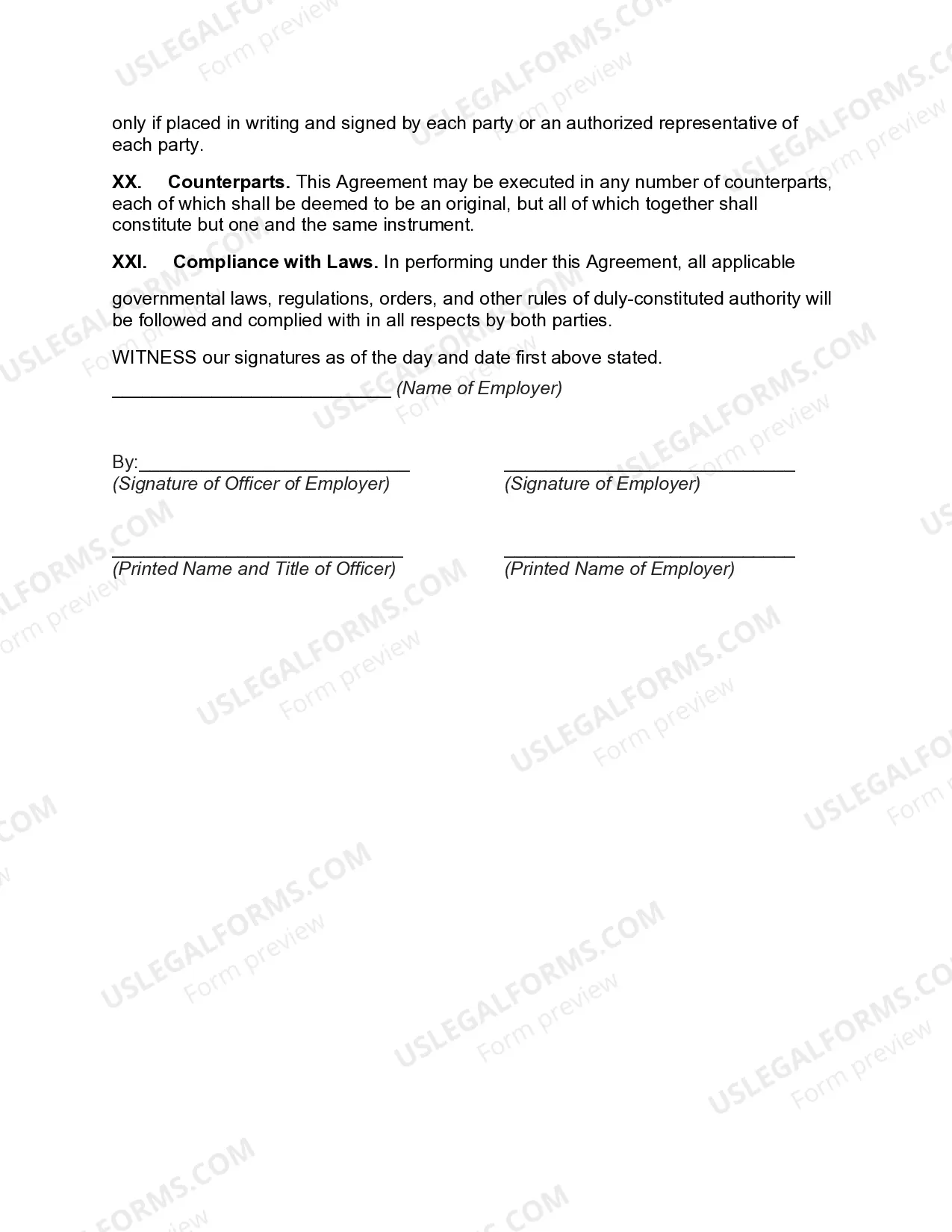

Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee: A Comprehensive Overview In the realm of employee benefits and insurance arrangements, Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee stands out as an attractive option. This agreement is designed to provide mutual benefits to both the employer and employee, offering financial security and potential tax advantages. In this article, we will delve into the intricacies of this agreement, its features, and the potential types associated with it. A Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee is a contractual arrangement between an employer and an employee, wherein both parties jointly own a life insurance policy on the employee's life. The policy is typically a permanent life insurance policy, such as whole life or universal life. This arrangement allows the employer and employee to share the benefits and costs associated with the policy, creating a collaborative approach to insurance planning. Key Features: 1. Joint Ownership: The employer and employee both hold an ownership interest in the policy. This means that both parties have the right to access policy values, receive policy dividends, and participate in the policy's cash accumulation. 2. Premium Payments: Under this agreement, the employer pays a portion or all of the premiums required to maintain the policy. The employee may also contribute towards the premium payments, depending on the agreement's terms. 3. Death Benefit Distribution: In the event of the employee's death, the death benefit is paid out to the employer to recover the premium amounts they contributed. The remaining death benefit is then directed to the employee's designated beneficiaries. 4. Cash Value Accumulation: As the policy accumulates cash value over time, both the employer and employee may access a portion of the policy's cash value, with certain restrictions and tax implications. Types of Washington Split-Dollar Insurance Agreements: 1. Endorsement Split-Dollar Agreement: In this type of agreement, the employer endorses the employee's individual life insurance policy, designating the employee as the policy's owner. The employer pays the premiums on the policy as a form of compensation or benefit. 2. Collateral Assignment Split-Dollar Agreement: In this arrangement, the employer purchases a life insurance policy and designates the employee as the policy's owner. The employer pays the premiums, but unlike endorsement split-dollar, they also receive a collateral assignment interest in the policy's cash value. Benefits and Considerations: — Employee Benefits: The employee gains access to life insurance protection, potential tax-free death benefits for beneficiaries, and the ability to accumulate cash value within the policy. — Employer Benefits: The employer can use the policy's cash value as a source of funds for business needs, cover premiums paid, and potentially recover premium payments upon the employee's death. It is crucial to consult with a knowledgeable insurance professional or financial advisor to determine the specific terms and conditions applicable to a Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee. This ensures that the agreement aligns with both the employer's and employee's objectives while adhering to the relevant Washington state laws and regulations. In conclusion, the Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee provides a unique and collaborative approach to life insurance planning. By leveraging this arrangement, employers can offer valuable benefits and employees can secure financial protection and potential tax advantages.

Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee

Description

How to fill out Washington Split-Dollar Insurance Agreement With Policy Owned Jointly By Employer And Employee?

Discovering the right legal file template can be a struggle. Naturally, there are a variety of templates accessible on the Internet, but how would you find the legal kind you require? Take advantage of the US Legal Forms web site. The support gives 1000s of templates, including the Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee, that you can use for company and private requires. All the forms are checked out by specialists and meet up with state and federal requirements.

If you are presently authorized, log in for your accounts and then click the Down load option to have the Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee. Make use of your accounts to check from the legal forms you might have bought earlier. Visit the My Forms tab of your respective accounts and get an additional backup of the file you require.

If you are a whole new consumer of US Legal Forms, listed here are easy directions that you should follow:

- Initial, make sure you have selected the correct kind to your metropolis/region. You may look through the shape using the Review option and study the shape information to ensure it is the best for you.

- When the kind will not meet up with your requirements, use the Seach field to discover the proper kind.

- When you are certain that the shape is suitable, click the Get now option to have the kind.

- Pick the costs plan you want and enter in the necessary information. Create your accounts and pay money for the order using your PayPal accounts or Visa or Mastercard.

- Select the data file structure and download the legal file template for your system.

- Total, revise and printing and indication the received Washington Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee.

US Legal Forms is definitely the largest library of legal forms where you can find different file templates. Take advantage of the service to download expertly-manufactured files that follow condition requirements.