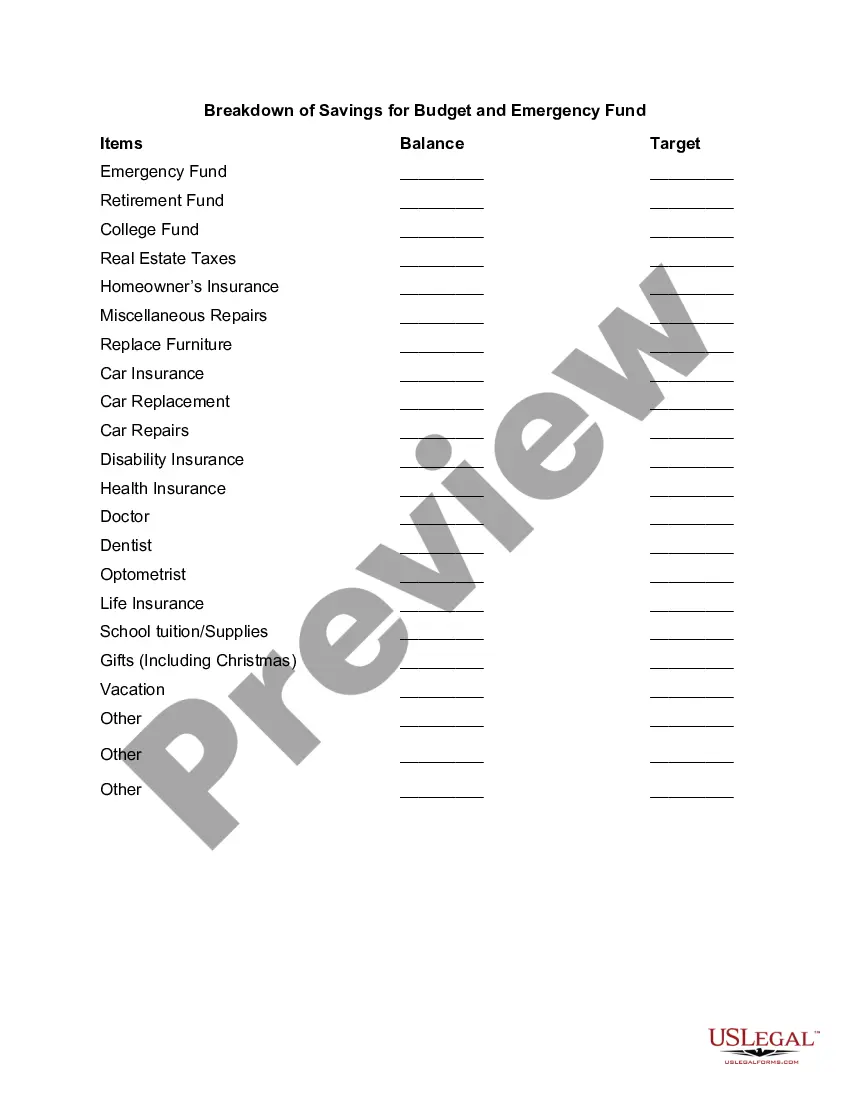

A Washington Breakdown of Savings for Budget and Emergency Fund is a comprehensive method for managing finances effectively, ensuring both short-term stability and long-term security. It involves analyzing individual income and expenses, allocating funds towards budgetary requirements, and setting aside emergency savings to address unexpected financial setbacks. By utilizing this approach, individuals can attain financial stability and prepare for unforeseen circumstances in Washington. Here is a breakdown of various types of savings commonly found within a Washington budget and emergency fund: 1. Budgeted Savings: This category involves planning and allocating money towards specific financial goals, such as saving for a down payment on a house, a vacation, or higher education expenses. By setting realistic saving targets and regularly contributing to them, individuals can work towards achieving these milestones. 2. Emergency Fund: Building an emergency fund is imperative in Washington to cope with unexpected expenses like medical emergencies, home or car repairs, or sudden job loss. By setting aside a portion of income specifically for emergencies, individuals can ensure financial stability during turbulent times without relying on expensive loans or credit cards. 3. Rainy Day Fund: Similar to an emergency fund, a rainy day fund is designed to handle unforeseen situations that may not be as immediate or severe. It can be used to cover minor medical expenses, home appliance repairs, or temporary reduction in income. This fund acts as a buffer to avoid compromising regular budgeting for small unexpected expenses. 4. Retirement Savings: Planning for retirement is vital, and a portion of income should be dedicated to building a retirement fund. Washington offers various retirement saving plans, such as 401(k), Individual Retirement Accounts (IRAs), or pension schemes. This allows individuals to save systematically for their post-retirement years and enjoy financial security during that phase of life. 5. Debt Repayment Fund: Individuals burdened with loans or credit card debt can allocate a portion of their savings to gradually pay off outstanding balances. By consistently contributing to a debt repayment fund, individuals in Washington can reduce their liabilities and rebuild their financial health. 6. Tax Savings: Washington residents can optimize their tax savings by utilizing tax-efficient investment options, such as Individual Retirement Accounts (IRAs), Health Savings Accounts (Has), or 529 college savings plans. This category focuses on reducing tax obligations while simultaneously growing savings for specific purposes. To summarize, a Washington Breakdown of Savings for Budget and Emergency Fund encompasses budgeted savings, emergency fund, rainy day fund, retirement savings, debt repayment fund, and tax savings. By carefully managing and allocating funds to each category, individuals in Washington can achieve financial stability, prepare for emergencies, and work towards long-term financial goals.

Washington Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Washington Breakdown Of Savings For Budget And Emergency Fund?

Are you in the situation the place you will need documents for sometimes enterprise or person functions just about every day time? There are plenty of legal file themes accessible on the Internet, but finding ones you can trust isn`t effortless. US Legal Forms provides a large number of develop themes, just like the Washington Breakdown of Savings for Budget and Emergency Fund, that happen to be written to meet federal and state requirements.

When you are already familiar with US Legal Forms site and have a merchant account, just log in. Following that, you can down load the Washington Breakdown of Savings for Budget and Emergency Fund format.

Unless you have an account and would like to start using US Legal Forms, adopt these measures:

- Get the develop you need and make sure it is for your right town/county.

- Make use of the Review key to examine the shape.

- See the outline to ensure that you have chosen the right develop.

- In the event the develop isn`t what you`re searching for, use the Lookup discipline to obtain the develop that meets your requirements and requirements.

- When you get the right develop, click Buy now.

- Opt for the pricing program you desire, fill out the specified details to make your bank account, and pay money for your order utilizing your PayPal or charge card.

- Select a handy document file format and down load your duplicate.

Discover each of the file themes you have bought in the My Forms menu. You can obtain a more duplicate of Washington Breakdown of Savings for Budget and Emergency Fund whenever, if necessary. Just go through the needed develop to down load or print the file format.

Use US Legal Forms, probably the most considerable collection of legal types, to save lots of efforts and stay away from faults. The services provides expertly made legal file themes which can be used for an array of functions. Make a merchant account on US Legal Forms and initiate making your lifestyle a little easier.

Form popularity

FAQ

Financial experts agree that a fully-funded emergency fund should be between three and six months of living expenses.

The 70/30 rule in finance allows us to spend, save, and invest. It's simple. Divide the monthly take-home pay by 70% for monthly expenses, and 30% is subdivided into 20% savings (including debt), 10% to tithing, donation, investment, or retirement.

The 70/30 method is a budgeting technique to help you allocate your money, Kia says. Put simply, each month, 70% of the money that you earn will be your spending money, including essentials like bills and rent as well as luxuries, and 30% of the money you earn will go towards your savings.

The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

70% is for monthly expenses (anything you spend money on). 20% goes into savings, unless you have pressing debt (see below for my definition), in which case it goes toward debt first. 10% goes to donation/tithing, or investments, retirement, saving for college, etc.

If you have consumer debt, I recommend saving a starter emergency fund of $1,000 first. Then, once you're out of debt, it's time to beef up that amount and save three to six months of expenses in a fully funded emergency fund.

It's all about your personal expenses Those include things like rent or mortgage payments, utilities, healthcare expenses, and food. If your monthly essentials come to $2,500 a month, and you're comfortable with a four-month emergency fund, then you should be set with a $10,000 savings account balance.

Most experts believe you should have enough money in your emergency fund to cover at least 3 to 6 months' worth of living expenses.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.