Wisconsin Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement

Description

How to fill out Balloon Secured Note Addendum And Rider To Mortgage, Deed Of Trust Or Security Agreement?

If you wish to obtain, acquire, or print official document templates, utilize US Legal Forms, the largest collection of legal forms available online. Take advantage of the site's straightforward and user-friendly search to locate the documents you require.

Various templates for business and personal use are organized by categories and states, or keywords. Use US Legal Forms to find the Wisconsin Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement in just a few clicks.

If you are currently a US Legal Forms customer, Log In to your account and click the Acquire button to locate the Wisconsin Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement. You can also access forms you previously obtained within the My documents section of your account.

Every legal document template you purchase is yours indefinitely. You have access to each form you acquired with your account. Click the My documents section and select a form to print or download again.

Compete and purchase, and print the Wisconsin Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement with US Legal Forms. There are millions of professional and state-specific forms you can use for your business or personal needs.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to review the form's contents. Be sure to read the description.

- Step 3. If you are not satisfied with the type, utilize the Search area at the top of the screen to find other forms in the legal form template.

- Step 4. Once you have found the form you need, click the Get now button. Choose the pricing plan you prefer and enter your details to register for the account.

- Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Step 6. Locate the form in the legal type and download it to your device.

- Step 7. Fill out, modify, and print or sign the Wisconsin Balloon Secured Note Addendum and Rider to Mortgage, Deed of Trust or Security Agreement.

Form popularity

FAQ

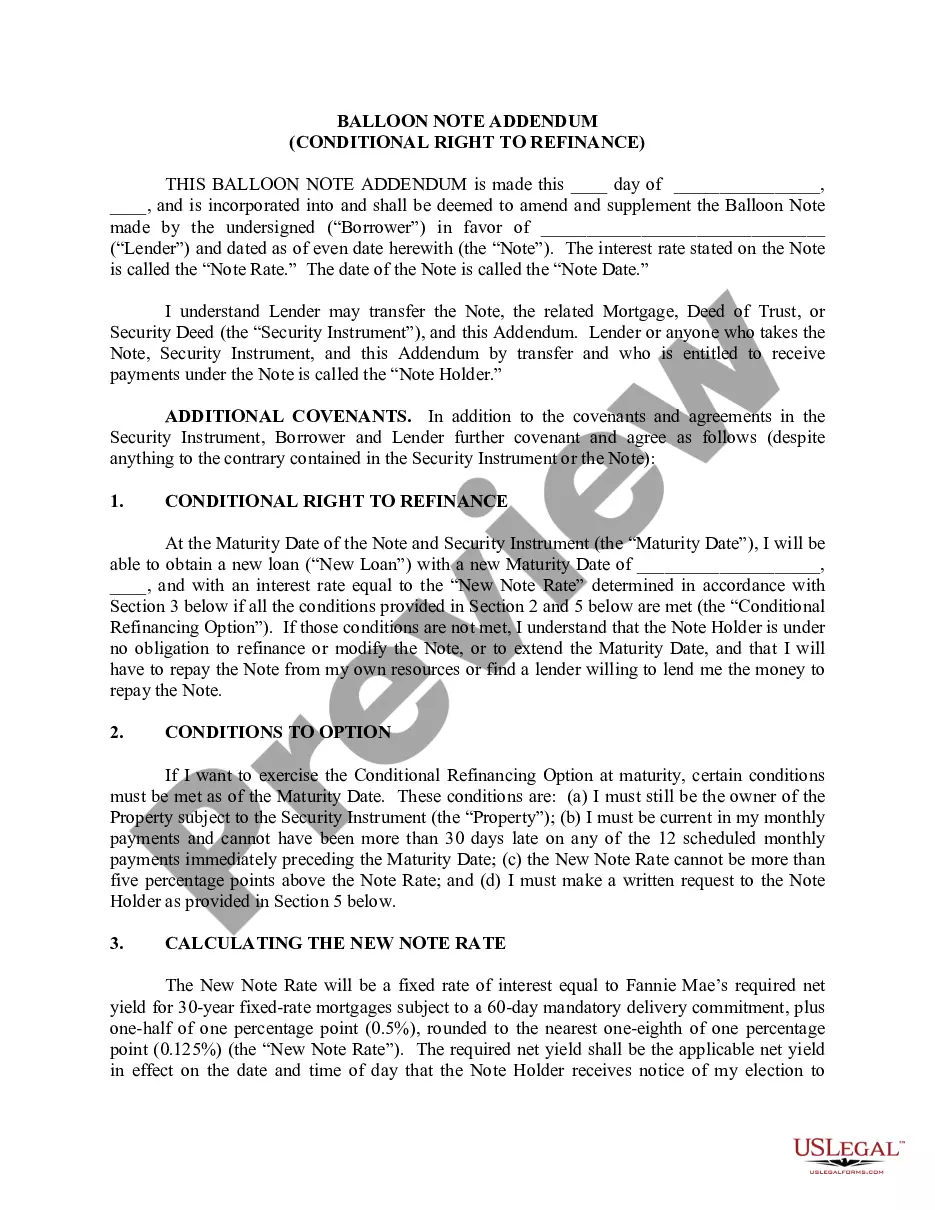

A balloon mortgage is a type of home loan in which you make low or no monthly payments for a short term, usually five or seven years. After this low- or no-payment period ends, you pay a lump sum, which settles the remaining balance in full.

A balloon payment is a lump sum principal balance that is due at the end of a loan term. The borrower pays much smaller monthly payments until the balloon payment is due. These payments may be entirely or almost entirely interest on the loan rather than principal.

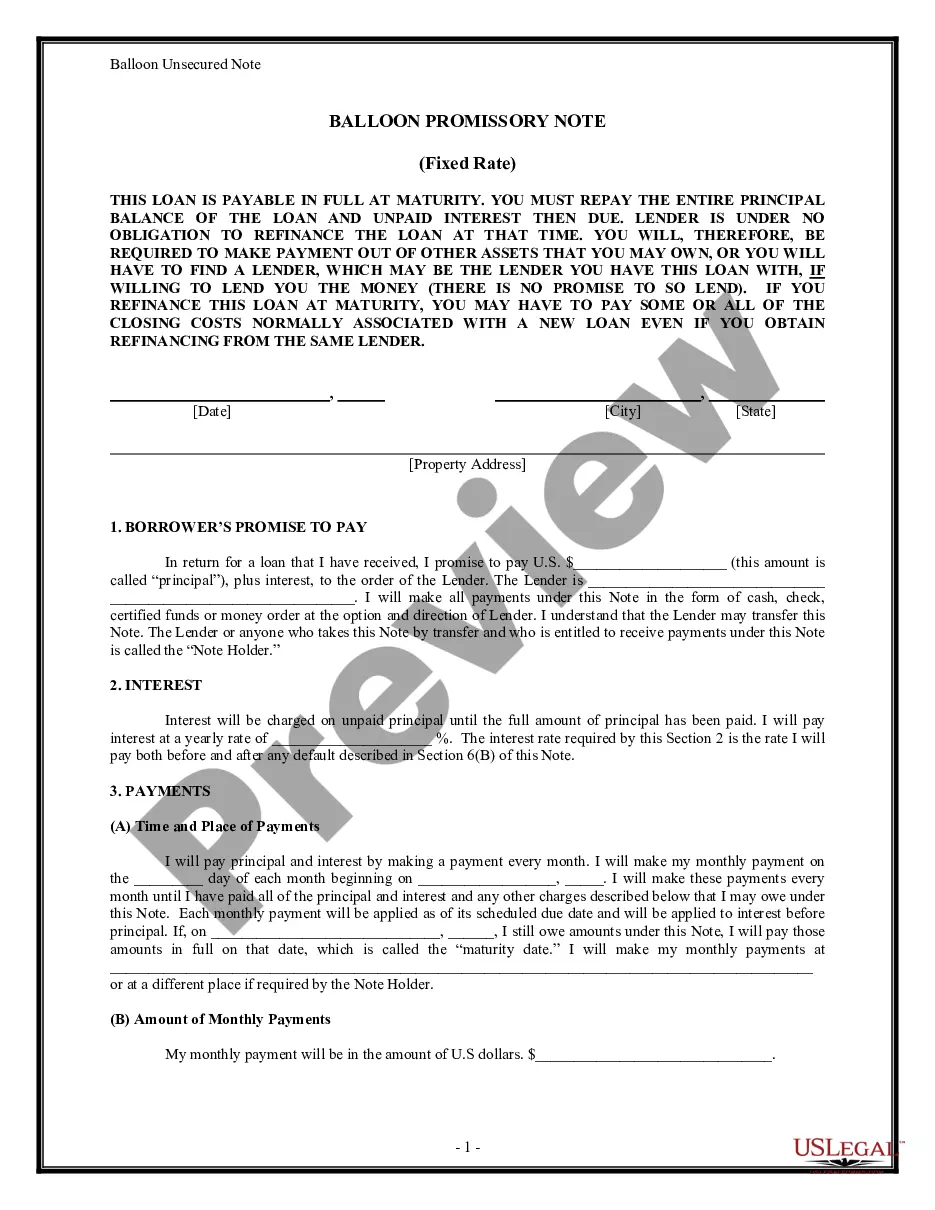

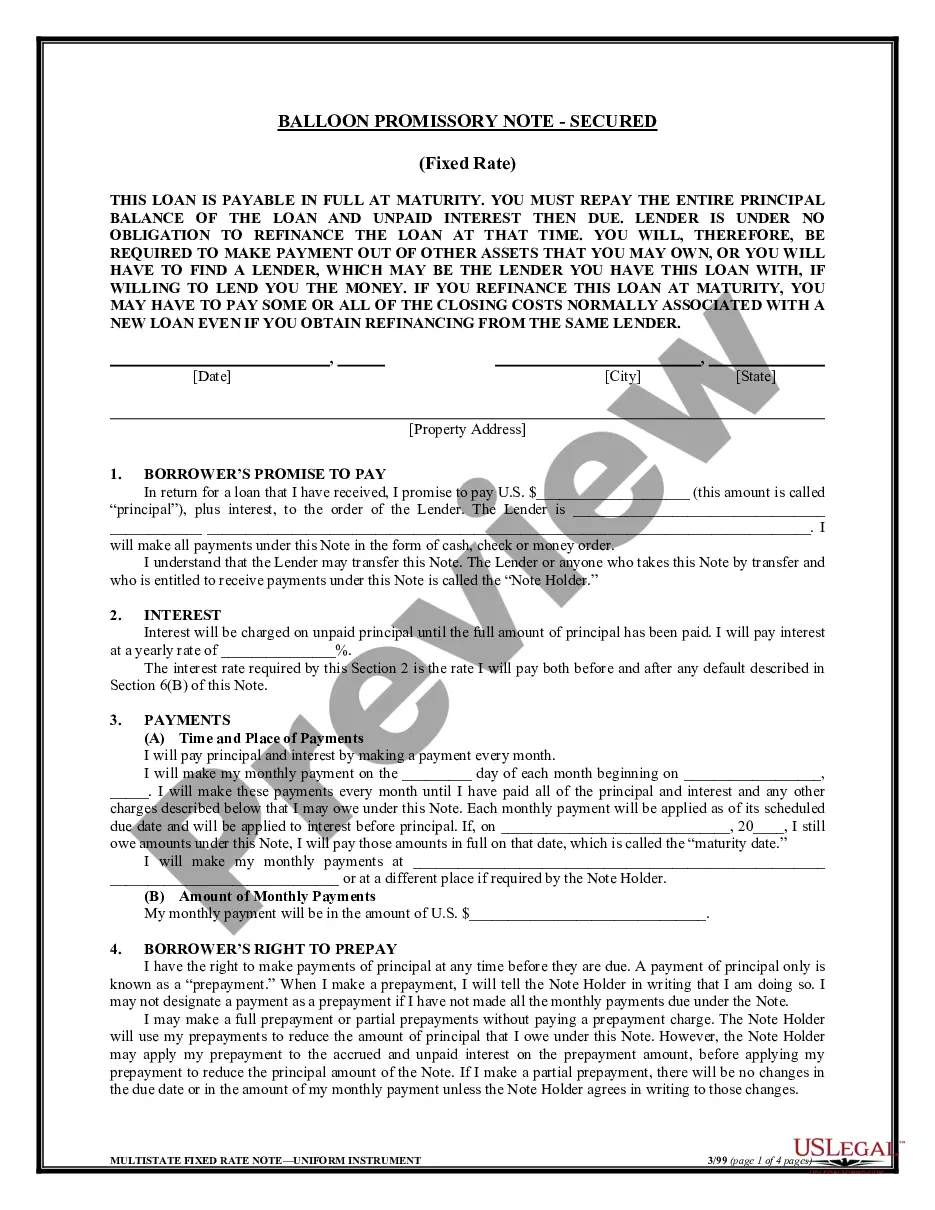

A Promissory Note with Balloon Payments is a loan contract that enables a lender set loan terms with one or more larger payments at the end. This lending document helps you to clarify the terms of a loan, define the payment schedule, and provide an amortization table, if the loan includes interest.

Balloon loans can offer flexibility in the initial loan period by providing a low payment. Still, borrowers should have a plan to pay the remaining balance or refinance before the payment comes due. These loans do have their place?for those who only need to borrow for a short time, they can offer significant savings.

Cons of balloon payments Unsecured loans with balloon payments usually have a higher interest rate than conventional loans. Paying that large balloon payment at the end of the loan may be financially difficult for your business.

A balloon payment is a lump sum payment that is significantly larger than the monthly payments and paid at the end of a loan's term. Unlike loans that have a series of fixed payments to pay off the balance of the loan, a loan that includes a balloon payment is made up of lower fixed payments and a final larger payment.

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

A secured promissory note is an agreement where the borrower puts something of value up as collateral to safeguard the value of the loan. In the event the borrower is unable to make payments and defaults on the loan, a secured promissory note empowers the lender to take possession of the collateral in lieu of payment.