A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

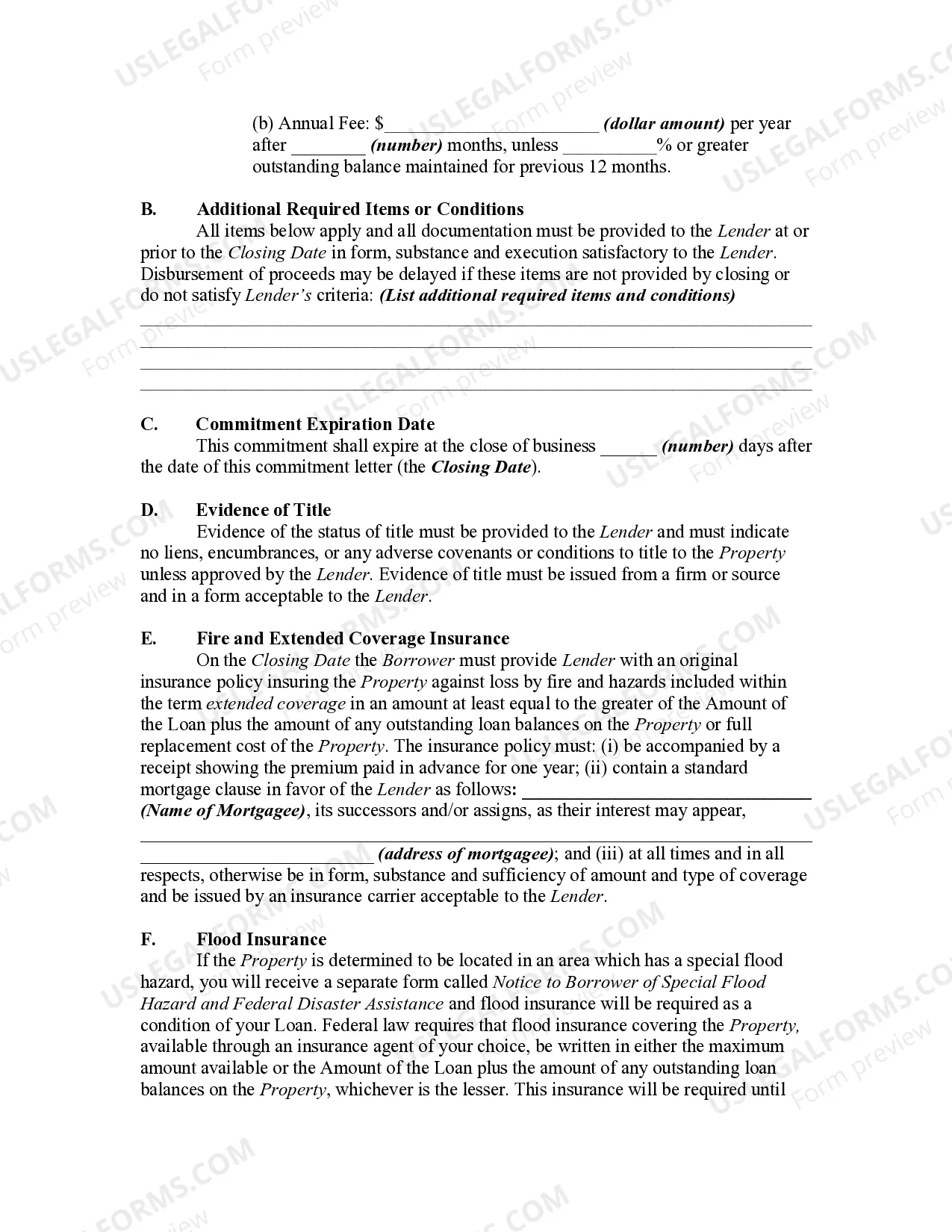

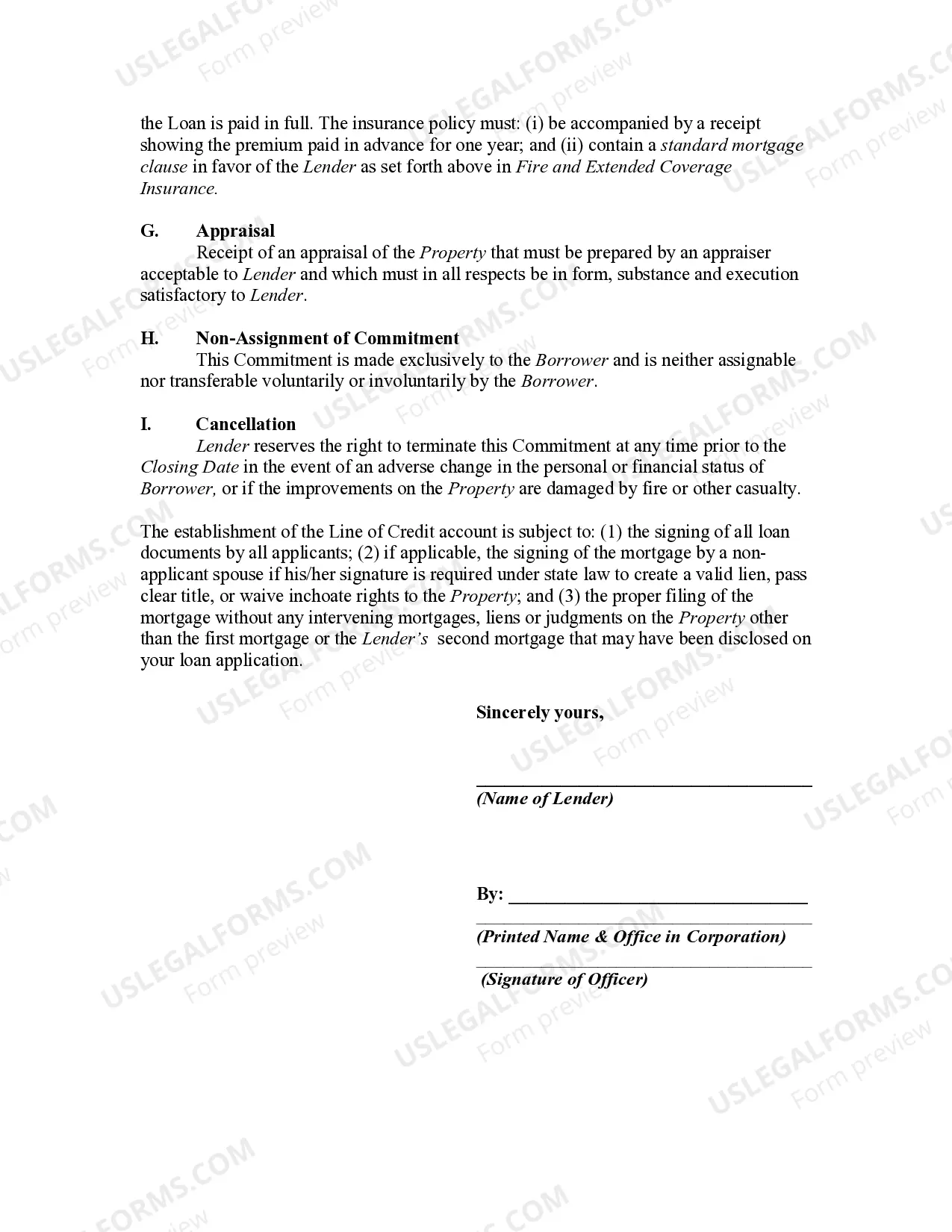

A Wisconsin Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a legal document that outlines the terms and conditions of a mortgage loan specifically used for accessing a home's equity. This commitment signifies the lender's agreement to provide a line of credit to the borrower, based on the value of the home and the borrower's creditworthiness. In Wisconsin, there are different types of Mortgage Loan Commitments available for a Home Equity Line of Credit. These include: 1. Fixed-Rate HELOT Commitment: This commitment offers a fixed interest rate for the duration of the loan term. Borrowers have the advantage of consistent monthly payments, allowing them to plan their finances more effectively. 2. Variable-Rate HELOT Commitment: This commitment involves an adjustable interest rate, which changes periodically based on market conditions. Borrowers may experience fluctuating monthly payments, depending on the current interest rate environment. 3. Interest-Only HELOT Commitment: With this commitment, borrowers are only required to make interest payments for a specified period, typically the first few years of the loan term. After the interest-only period, borrowers will need to start paying principal in addition to interest. 4. Conversion HELOT Commitment: This commitment provides borrowers with the option to convert their HELOT into a fixed-rate mortgage loan at a later time. This conversion can be beneficial if they wish to secure a fixed interest rate, especially if rates are expected to rise. 5. Subordinate HELOT Commitment: This commitment applies when a borrower already has an existing first mortgage on their property. The lender offers an additional loan that is subordinate, or secondary, to the first mortgage. The subordinate HELOT commitment allows borrowers to tap into their home equity without refinancing their primary mortgage. Regardless of the specific type of Wisconsin Mortgage Loan Commitment for Home Equity Line of Credit, it is essential for borrowers to thoroughly review the terms and conditions, including interest rates, repayment terms, and any associated fees or penalties. It is highly recommended consulting with a mortgage professional or financial advisor to understand the implications and choose the most suitable commitment for individual needs.