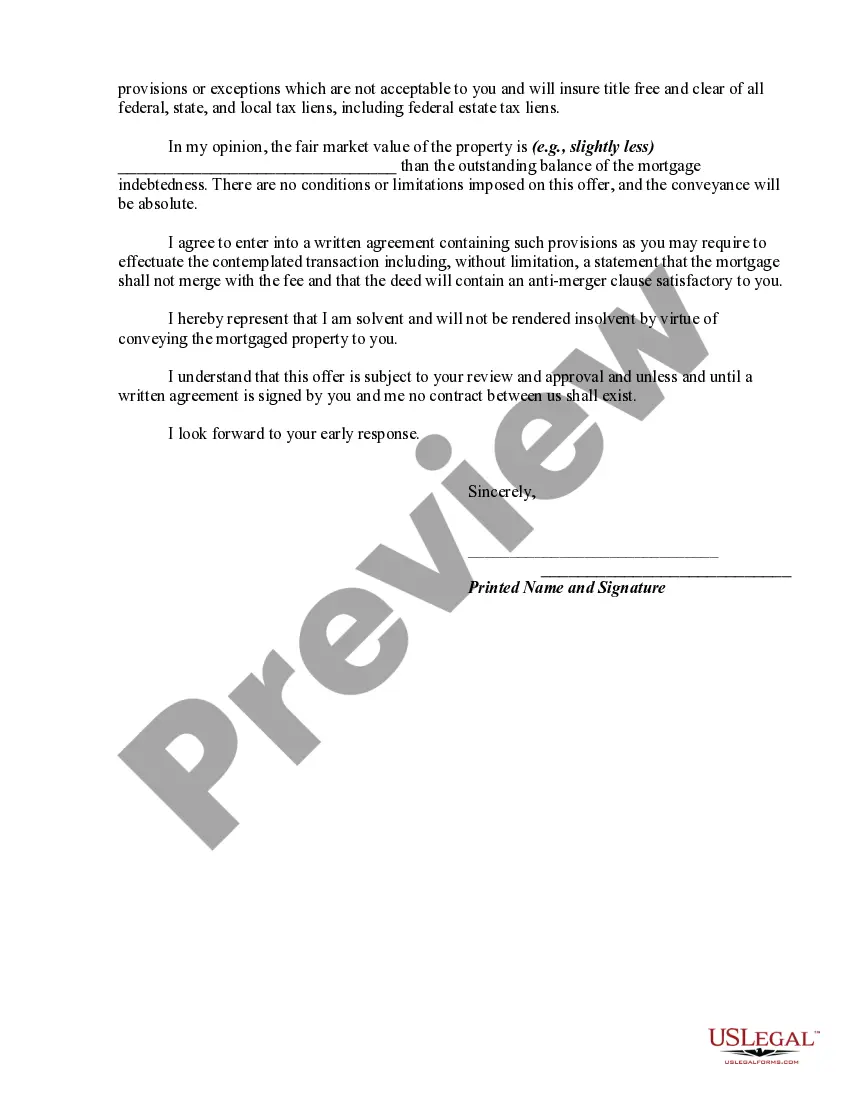

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

1. Introduction to Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure: In Wisconsin, when a borrower is facing financial hardship and cannot afford to make mortgage payments, they have the option to offer a Deed in Lieu of Foreclosure to the lender. This alternative solution allows the borrower to transfer ownership of the property back to the lender voluntarily. In return, the lender agrees to release the borrower from their mortgage obligation, avoiding the often-damaging effects of foreclosure. Let's explore the specifics and different types of Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure. 2. Benefits and Process: a. Wisconsin Deed in Lieu of Foreclosure is an attractive option for borrowers as it enables them to avoid the negative consequences usually associated with foreclosure, such as damaged credit scores and the lengthy legal process. b. The process starts with the borrower submitting a written offer to their lender, expressing their intention to transfer the property to the lender in exchange for satisfaction of the mortgage. The offer should include a detailed description of the property, reasons for financial hardship, and a proposed surrender date. c. The lender will then evaluate the offer and determine whether to accept it. If accepted, the lender will provide further instructions, such as signing the Deed in Lieu of Foreclosure agreement. d. Once the Deed in Lieu of Foreclosure agreement is signed, the borrower typically has to vacate the property by a specific date. 3. Different Types of Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure: There are several variations of the Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure, including: a. Standard Deed in Lieu of Foreclosure: This is the most common type, where the borrower voluntarily transfers ownership of the property to the lender. The lender agrees to release the borrower from any further mortgage obligations, preventing foreclosure. b. Cash for Keys Agreement: In some cases, the lender may offer a cash incentive to the borrower to encourage them to vacate the property swiftly and leave it in good condition. This arrangement benefits both parties, as the lender avoids the costs and delays associated with eviction, and the borrower receives financial assistance to facilitate relocation. c. Deed in Lieu with Deficiency Waiver: In this type of agreement, the lender agrees not to pursue the borrower for any remaining debt after the property is transferred back to them. This provides the borrower with additional peace of mind, knowing they won't face further financial consequences of the Deed in Lieu of Foreclosure is completed. d. Cooperative Short Sale: Although not strictly a Deed in Lieu of Foreclosure, in a cooperative short sale, the borrower offers to sell the property for less than what is owed on the mortgage. The lender agrees to accept the sale proceeds as full satisfaction of the mortgage, avoiding foreclosure and allowing the borrower to move on from their financial difficulties. In conclusion, Wisconsin offers various options for borrowers to propose a Deed in Lieu of Foreclosure as an alternative to traditional foreclosure proceedings. These alternatives aim to provide financial relief to distressed borrowers while minimizing the negative impact on their credit and overall well-being.1. Introduction to Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure: In Wisconsin, when a borrower is facing financial hardship and cannot afford to make mortgage payments, they have the option to offer a Deed in Lieu of Foreclosure to the lender. This alternative solution allows the borrower to transfer ownership of the property back to the lender voluntarily. In return, the lender agrees to release the borrower from their mortgage obligation, avoiding the often-damaging effects of foreclosure. Let's explore the specifics and different types of Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure. 2. Benefits and Process: a. Wisconsin Deed in Lieu of Foreclosure is an attractive option for borrowers as it enables them to avoid the negative consequences usually associated with foreclosure, such as damaged credit scores and the lengthy legal process. b. The process starts with the borrower submitting a written offer to their lender, expressing their intention to transfer the property to the lender in exchange for satisfaction of the mortgage. The offer should include a detailed description of the property, reasons for financial hardship, and a proposed surrender date. c. The lender will then evaluate the offer and determine whether to accept it. If accepted, the lender will provide further instructions, such as signing the Deed in Lieu of Foreclosure agreement. d. Once the Deed in Lieu of Foreclosure agreement is signed, the borrower typically has to vacate the property by a specific date. 3. Different Types of Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure: There are several variations of the Wisconsin Offer by Borrower of Deed in Lieu of Foreclosure, including: a. Standard Deed in Lieu of Foreclosure: This is the most common type, where the borrower voluntarily transfers ownership of the property to the lender. The lender agrees to release the borrower from any further mortgage obligations, preventing foreclosure. b. Cash for Keys Agreement: In some cases, the lender may offer a cash incentive to the borrower to encourage them to vacate the property swiftly and leave it in good condition. This arrangement benefits both parties, as the lender avoids the costs and delays associated with eviction, and the borrower receives financial assistance to facilitate relocation. c. Deed in Lieu with Deficiency Waiver: In this type of agreement, the lender agrees not to pursue the borrower for any remaining debt after the property is transferred back to them. This provides the borrower with additional peace of mind, knowing they won't face further financial consequences of the Deed in Lieu of Foreclosure is completed. d. Cooperative Short Sale: Although not strictly a Deed in Lieu of Foreclosure, in a cooperative short sale, the borrower offers to sell the property for less than what is owed on the mortgage. The lender agrees to accept the sale proceeds as full satisfaction of the mortgage, avoiding foreclosure and allowing the borrower to move on from their financial difficulties. In conclusion, Wisconsin offers various options for borrowers to propose a Deed in Lieu of Foreclosure as an alternative to traditional foreclosure proceedings. These alternatives aim to provide financial relief to distressed borrowers while minimizing the negative impact on their credit and overall well-being.